What This Calculator Does

This tool applies to US traditional (pre-tax) 401(k) plans. Money you contribute to a traditional 401(k) is deducted from your taxable income, so it lowers the federal income tax you owe this year. This calculator shows two numbers: how much tax you save, and how much your take-home pay actually drops once that saving is factored in. It uses a simplified flat marginal-rate model and does not include state taxes, FICA, or employer matching.

How to Use It

Enter your planned annual 401(k) contribution and your marginal tax rate — the percentage applied to your top dollar of income (for 2024 US brackets this is commonly 12%, 22%, 24%, 32%, 35% or 37%). The calculator instantly returns your estimated tax savings and the net reduction in your take-home pay.

The Formula Explained

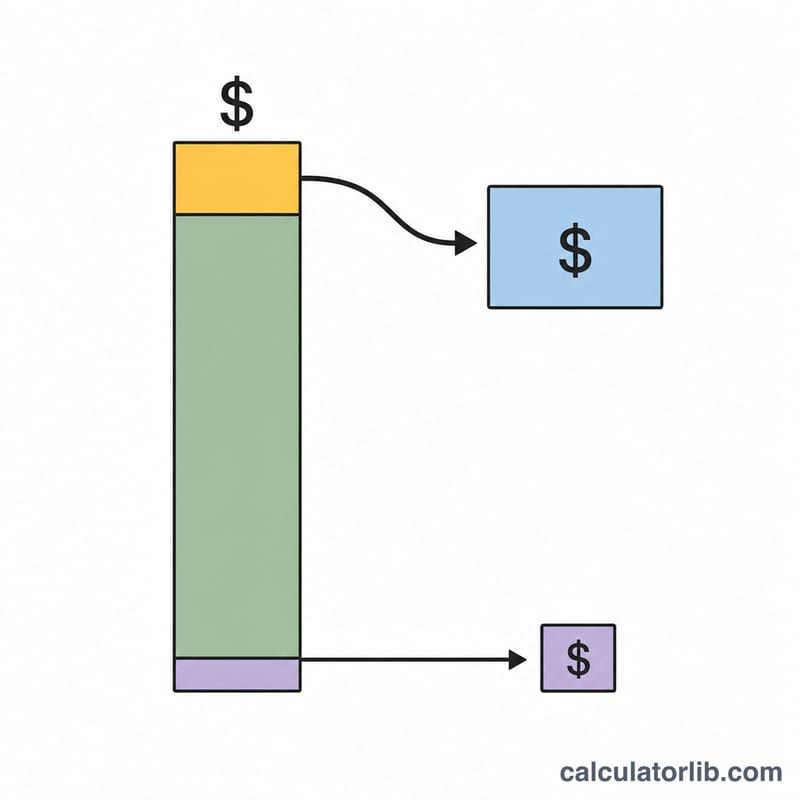

Because a pre-tax contribution reduces taxable income, the tax you avoid equals the contribution multiplied by your marginal rate: $$\text{Tax Savings} = \text{Contribution} \times \text{Marginal Tax Rate}$$. The amount your paycheck actually shrinks is the contribution minus that saving: $$\text{Net Pay Reduction} = \text{Contribution} \times (1 - \text{Marginal Tax Rate})$$. In other words, the government effectively subsidizes part of your retirement saving.

Worked Example

Suppose you contribute $10,000 per year and your marginal tax rate is 22%. Tax savings = $$10{,}000 \times 0.22 = 2{,}200$$ $2,200. Net pay reduction = $$10{,}000 \times (1 - 0.22) = 7{,}800$$ $7,800. So you set aside $10,000 for retirement while your take-home pay only falls by $7,800.

2024 Federal Tax Brackets & Marginal Rates

Your marginal tax rate is the rate applied to your last (highest) dollar of taxable income — and the rate that a pre-tax 401(k) contribution effectively offsets. The table below shows the seven federal ordinary-income brackets for tax year 2024 for single filers and for married couples filing jointly. Use the rate that applies to the top of your taxable income as the Tax Rate (%) input in the calculator.

| Marginal Rate | Single — Taxable Income | Married Filing Jointly — Taxable Income |

|---|---|---|

| 10% | $0 – $11,600 | $0 – $23,200 |

| 12% | $11,601 – $47,150 | $23,201 – $94,300 |

| 22% | $47,151 – $100,525 | $94,301 – $201,050 |

| 24% | $100,526 – $191,950 | $201,051 – $383,900 |

| 32% | $191,951 – $243,725 | $383,901 – $487,450 |

| 35% | $243,726 – $609,350 | $487,451 – $731,200 |

| 37% | $609,351 and up | $731,201 and up |

Because the U.S. system is progressive, only income within each band is taxed at that band's rate. A pre-tax 401(k) contribution reduces taxable income from the top down, so it saves tax at your marginal rate first. Note these are federal brackets only — state income tax (where it applies) can increase your total savings further.

401(k) Contribution Limits

The IRS caps how much you can defer into a workplace 401(k) each year. For tax year 2024, the limits are:

| Contribution Type | 2024 Limit | Who It Applies To |

|---|---|---|

| Elective deferral (employee) | $23,000 | All eligible employees |

| Catch-up contribution | $7,500 | Employees age 50 or older |

| Total for age 50+ | $30,500 | Age 50 or older (base + catch-up) |

These limits apply to your own pre-tax (and Roth) salary deferrals; employer matching contributions are separate and do not count against the $23,000/$30,500 employee limit. Maxing out the $23,000 employee deferral at a 24% marginal rate would cut your federal tax bill by $5,520 while reducing take-home pay by only $17,480 for the year.

Tax Savings Across Contributions & Rates

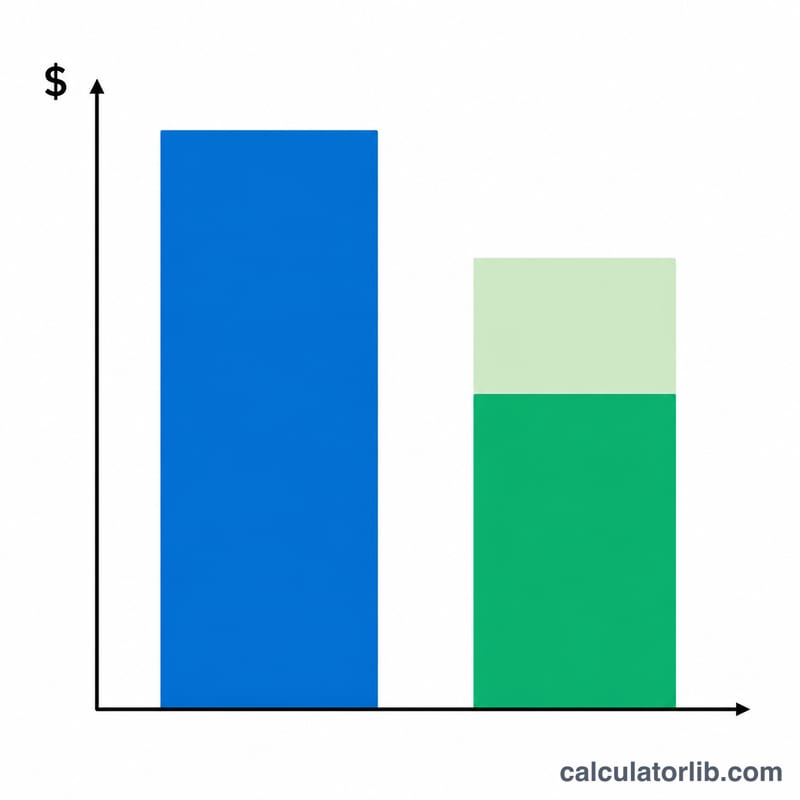

The two takeaways from a pre-tax contribution: the tax savings (contribution × marginal rate) is the cash you keep that would otherwise go to the IRS, and the net pay reduction (contribution × (1 − rate)) is how much your take-home actually drops. The higher your bracket, the more the government effectively subsidizes your saving.

| Contribution | Marginal Rate | Tax Savings | Net Pay Reduction |

|---|---|---|---|

| $5,000 | 12% | $600 | $4,400 |

| $5,000 | 22% | $1,100 | $3,900 |

| $5,000 | 24% | $1,200 | $3,800 |

| $5,000 | 32% | $1,600 | $3,400 |

| $10,000 | 12% | $1,200 | $8,800 |

| $10,000 | 22% | $2,200 | $7,800 |

| $10,000 | 24% | $2,400 | $7,600 |

| $10,000 | 32% | $3,200 | $6,800 |

| $15,000 | 12% | $1,800 | $13,200 |

| $15,000 | 22% | $3,300 | $11,700 |

| $15,000 | 24% | $3,600 | $11,400 |

| $15,000 | 32% | $4,800 | $10,200 |

| $23,000 | 12% | $2,760 | $20,240 |

| $23,000 | 22% | $5,060 | $17,940 |

| $23,000 | 24% | $5,520 | $17,480 |

| $23,000 | 32% | $7,360 | $15,640 |

For example, a worker in the 22% bracket who contributes $15,000 saves $3,300 in federal tax, so the contribution costs only $11,700 in reduced take-home pay. If that same $15,000 is invested each year and grows, see the 401(k) Retirement Calculator to project the long-term balance.

FAQ

Does this include state income tax? No. Add your state's marginal rate to the federal rate for a fuller picture in states that tax income.

Is this for a Roth 401(k)? No. Roth contributions are made with after-tax dollars and provide no upfront tax deduction, so there is no current-year tax savings.

What about FICA taxes? 401(k) contributions still have Social Security and Medicare (FICA) taxes withheld, so those are not reduced by your contribution.