What Is the Bonus Tax Calculator?

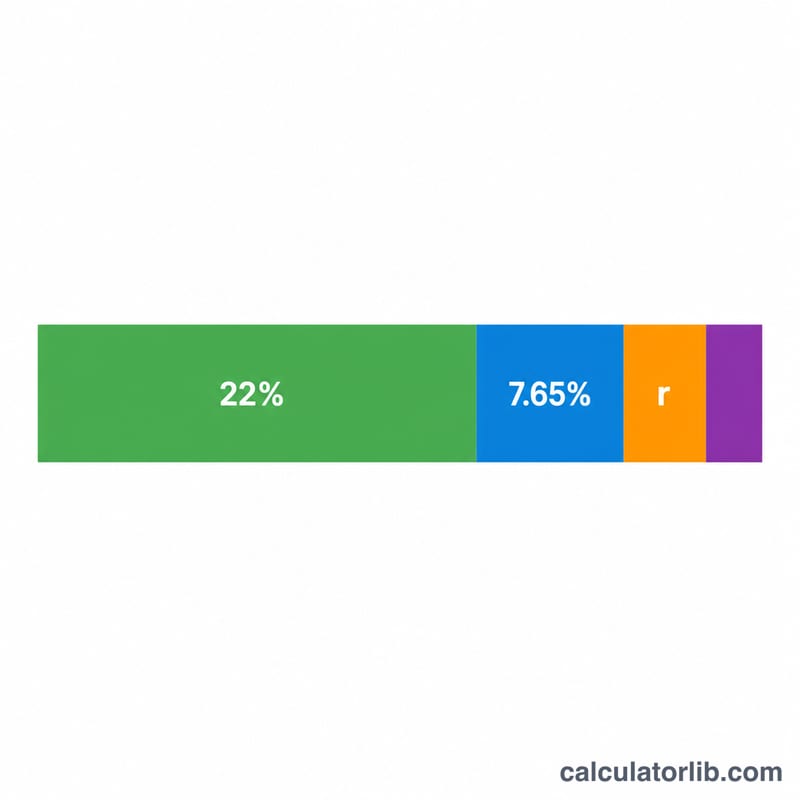

This calculator applies to the United States. It estimates how much of a bonus you actually take home after withholding. The IRS treats bonuses as supplemental wages, which employers most commonly withhold using the flat 22% federal rate (for supplemental pay under $1 million in a calendar year). On top of that, FICA taxes — 6.2% Social Security plus 1.45% Medicare, totaling 7.65% — and your state income tax are withheld. Figures are estimates for the 2024 rules and do not account for the Social Security wage cap, the 0.9% additional Medicare surtax, or local taxes.

How to Use It

Enter your gross bonus amount and your state income tax rate as a percentage (use 0 for states with no income tax, like Texas or Florida). The calculator shows your net take-home, a breakdown of each withholding category, and your effective withholding rate.

The Formula Explained

The net bonus is computed as Net = Bonus × (1 − 0.22 − 0.0765 − stateRate). The 0.22 is the flat federal supplemental withholding rate, 0.0765 is combined FICA, and stateRate is your state rate expressed as a decimal. Total tax withheld is simply the bonus minus the net amount.

Worked Example

Suppose you receive a $5,000 bonus in a state with a 5% income tax. Federal withholding is 5,000 × 0.22 = $1,100. FICA is 5,000 × 0.0765 = $382.50. State tax is 5,000 × 0.05 = $250. Total withheld = $1,732.50, leaving a net take-home of $3,267.50 — an effective rate of 34.65%.

Bonus Take-Home Across Scenarios

The federal supplemental withholding rate is a flat 22% on bonuses up to $1,000,000 in a calendar year. FICA adds 7.65% (6.2% Social Security + 1.45% Medicare). The table below combines those with three representative state rates so you can see how net pay and the effective withholding rate scale with the bonus size. Effective rate here is total withholding divided by the gross bonus.

| Bonus | State rate | Federal (22%) | FICA (7.65%) | State | Net take-home | Effective rate |

|---|---|---|---|---|---|---|

| $1,000 | 0% | $220.00 | $76.50 | $0.00 | $703.50 | 29.65% |

| $1,000 | 5% | $220.00 | $76.50 | $50.00 | $653.50 | 34.65% |

| $5,000 | 5% | $1,100.00 | $382.50 | $250.00 | $3,267.50 | 34.65% |

| $5,000 | 9% | $1,100.00 | $382.50 | $450.00 | $3,067.50 | 38.65% |

| $10,000 | 0% | $2,200.00 | $765.00 | $0.00 | $7,035.00 | 29.65% |

| $10,000 | 9% | $2,200.00 | $765.00 | $900.00 | $6,135.00 | 38.65% |

| $25,000 | 0% | $5,500.00 | $1,912.50 | $0.00 | $17,587.50 | 29.65% |

| $25,000 | 5% | $5,500.00 | $1,912.50 | $1,250.00 | $16,337.50 | 34.65% |

| $25,000 | 9% | $5,500.00 | $1,912.50 | $2,250.00 | $15,337.50 | 38.65% |

Because every component is a flat percentage, the effective rate does not change with the bonus amount — only the state rate moves it. At a 0% state rate the floor is 29.65% (22% + 7.65%); add the state rate directly on top. This is why a larger bonus does not get withheld at a proportionally higher rate under the flat-rate method.

Interpreting Your Result

The number this calculator produces is withholding, not your final tax. Withholding is a prepayment toward the income tax you ultimately owe for the year. When you file your federal and state returns, your bonus is combined with all your other income and taxed at your actual marginal rates. If too much was withheld, you receive a refund; if too little, you owe the difference.

Why the 22% may not match your bracket. The IRS percentage method for supplemental wages applies a flat 22% federal rate (38% above $1,000,000 in a year), regardless of your tax bracket. If your marginal bracket is 12%, the flat 22% over-withholds and you may get part of it back at filing. If your bracket is 24%, 32% or higher, the flat 22% under-withholds and you may owe more. The percentage method is a withholding convention, not the rate your bonus is ultimately taxed at.

Social Security wage cap. The 6.2% Social Security portion of FICA only applies up to the annual taxable maximum ($176,100 for 2025). If your year-to-date wages have already passed that cap, no additional Social Security is withheld on the bonus, so the FICA component drops from 7.65% to just the 1.45% Medicare rate. This calculator assumes the full 7.65%, so it can overstate FICA for high earners late in the year.

Additional Medicare surtax. An extra 0.9% Medicare tax applies to wages above $200,000 in a year (regardless of filing status, for withholding purposes). A bonus that pushes year-to-date wages past $200,000 can trigger this surtax on the amount above the threshold — which this simplified estimate does not include.

Also note that aggregate-method employers (who add the bonus to a regular paycheck and withhold using your W-4) may withhold a different amount than the flat 22% method shown here. This page provides general educational information, not personalized tax advice; consult a qualified tax professional for your specific situation.

FAQ

Is the 22% the actual tax I owe? No. It is the withholding rate. Your final tax liability is settled when you file your return; you may get some back or owe more depending on your total income and bracket.

What if my bonus exceeds $1 million? Amounts over $1 million in a year are withheld at 37% under the mandatory aggregate rule — this tool uses the standard 22% flat method.

Why include FICA? Social Security and Medicare taxes apply to bonus pay just like regular wages, so they reduce your take-home amount.