What Is the After-Tax Bonus Calculator?

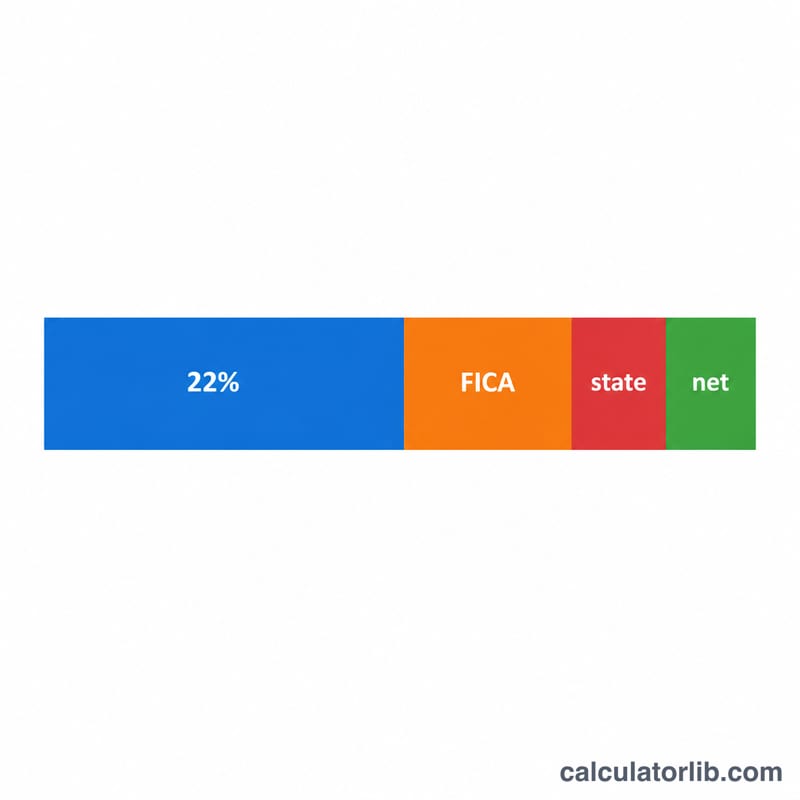

This calculator estimates the net (take-home) amount of a work bonus in the United States after federal supplemental withholding, FICA (Social Security and Medicare), and state income tax. In the US, supplemental wages such as bonuses are commonly withheld at a flat 22% federal rate (for bonuses up to $1 million in a calendar year). This tool uses that 22% flat rate, the standard 7.65% FICA rate, and a state rate you supply. It is an estimate for the 2024 rules and not tax advice — your actual refund or balance is settled when you file your annual return.

How to Use It

Enter your gross bonus amount, your FICA rate (default 7.65%, the combined employee Social Security + Medicare rate), and your state withholding rate (use 0 for no-income-tax states like Texas or Florida). The calculator shows your net bonus plus a breakdown of each tax withheld.

The Formula

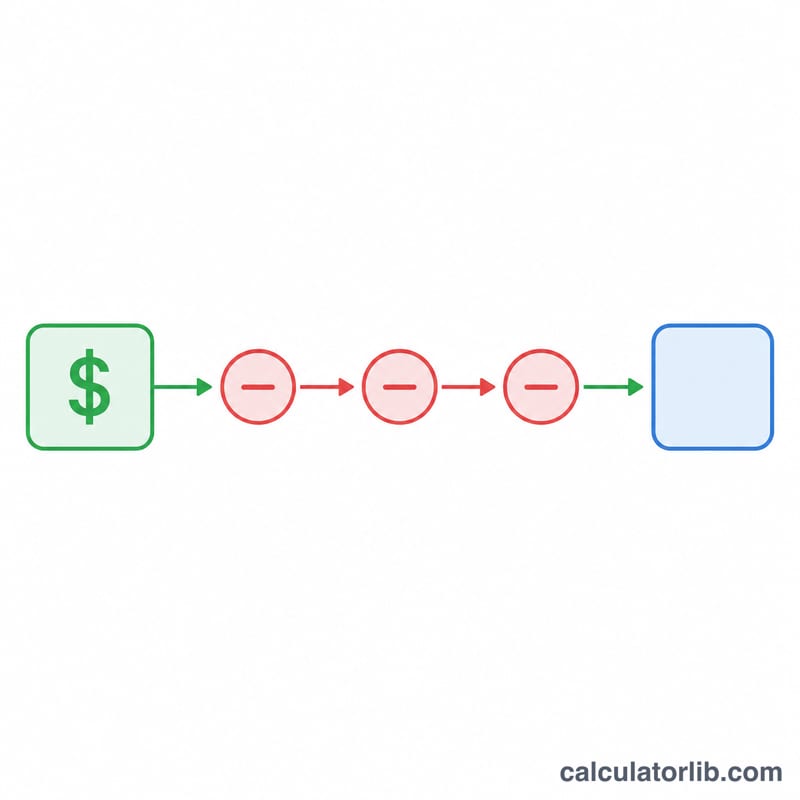

The net bonus is calculated as:

$$\text{net\_bonus} = \text{bonus} \times (1 - 0.22 - \text{fica\_rate} - \text{state\_rate})$$

Here \(0.22\) is the IRS flat supplemental federal withholding rate. Each rate is expressed as a decimal (\(7.65\% = 0.0765\)). Total withholding equals the bonus times the sum of all three rates.

Worked Example

Suppose you receive a $10,000 bonus, FICA is 7.65%, and your state rate is 5%. Total tax rate \(= 0.22 + 0.0765 + 0.05 = 0.3465\). Net bonus $$= 10{,}000 \times (1 - 0.3465) = 10{,}000 \times 0.6535 = \textbf{\$6{,}535}.$$ Federal \(= \$2{,}200\), FICA \(= \$765\), state \(= \$500\), leaving $6,535 in your pocket.

Net Bonus Across Different Scenarios

The scenarios below assume the 22% federal flat supplemental rate and a 7.65% FICA rate (6.2% Social Security + 1.45% Medicare), with the bonus falling below the Social Security wage base. The net bonus is the gross amount minus federal, FICA, and state withholding.

| Gross Bonus | State Rate | Federal (22%) | FICA (7.65%) | State | Net Bonus |

|---|---|---|---|---|---|

| $1,000 | 0% | $220.00 | $76.50 | $0.00 | $703.50 |

| $5,000 | 0% | $1,100.00 | $382.50 | $0.00 | $3,517.50 |

| $5,000 | 5% | $1,100.00 | $382.50 | $250.00 | $3,267.50 |

| $10,000 | 0% | $2,200.00 | $765.00 | $0.00 | $7,035.00 |

| $10,000 | 5% | $2,200.00 | $765.00 | $500.00 | $6,535.00 |

| $10,000 | 9% | $2,200.00 | $765.00 | $900.00 | $6,135.00 |

| $25,000 | 0% | $5,500.00 | $1,912.50 | $0.00 | $17,587.50 |

| $25,000 | 9% | $5,500.00 | $1,912.50 | $2,250.00 | $15,337.50 |

For a $10,000 bonus in a 9% state, total withholding is $3,865 (38.65%), leaving $6,135. Lower-rate or no-tax states keep noticeably more of each bonus dollar.

Understanding Your Net Bonus Result

The net figure this calculator produces is an estimate of take-home after withholding — not your final tax liability. Several important points explain the difference between what is withheld and what you ultimately owe:

- 22% is a withholding rate, not your tax rate. Under the IRS percentage method, employers withhold a flat 22% from supplemental wages such as bonuses. Your actual federal tax on that income depends on your total annual income and marginal bracket. If your effective rate is below 22%, you may have been over-withheld; if above, under-withheld.

- Everything reconciles at filing. When you file your annual tax return, all withholding (regular wages plus bonuses) is totaled and compared to your true tax owed. Over-withholding comes back as a refund; under-withholding means a balance due. The bonus is not taxed at a special permanent rate — it simply has its own withholding rule.

- The $1 million threshold. If your total supplemental wages for the year exceed $1,000,000, the portion above $1,000,000 must be withheld at the highest federal rate — currently 37% — rather than 22%. The first $1,000,000 may still use the 22% flat rate.

- FICA and the Social Security wage base. FICA is 7.65% (6.2% Social Security + 1.45% Medicare). Social Security tax only applies up to an annual wage base limit ($168,600 for 2024); once your year-to-date earnings exceed it, the 6.2% portion stops, so a large bonus paid late in the year may effectively be subject to only the 1.45% Medicare portion. High earners may also owe an Additional Medicare Tax of 0.9% above certain thresholds.

Because state rules, total income, and wage-base timing all affect the outcome, treat this result as a planning estimate. This is general information, not professional tax advice — consult a tax professional for guidance on your specific situation.

FAQ

Why is 22% used for federal tax? The IRS allows employers to withhold supplemental wages like bonuses at a flat 22% rate (for amounts under $1M per year), which is simpler than the aggregate method.

Will I get some of it back? Possibly. Withholding is not your final tax. If 22% is more than your actual marginal rate, you may recover the difference at tax time.

What FICA rate should I use? 7.65% (6.2% Social Security + 1.45% Medicare) is standard, though Social Security stops after the annual wage base is reached.