What the Interest Rate Calculator Does

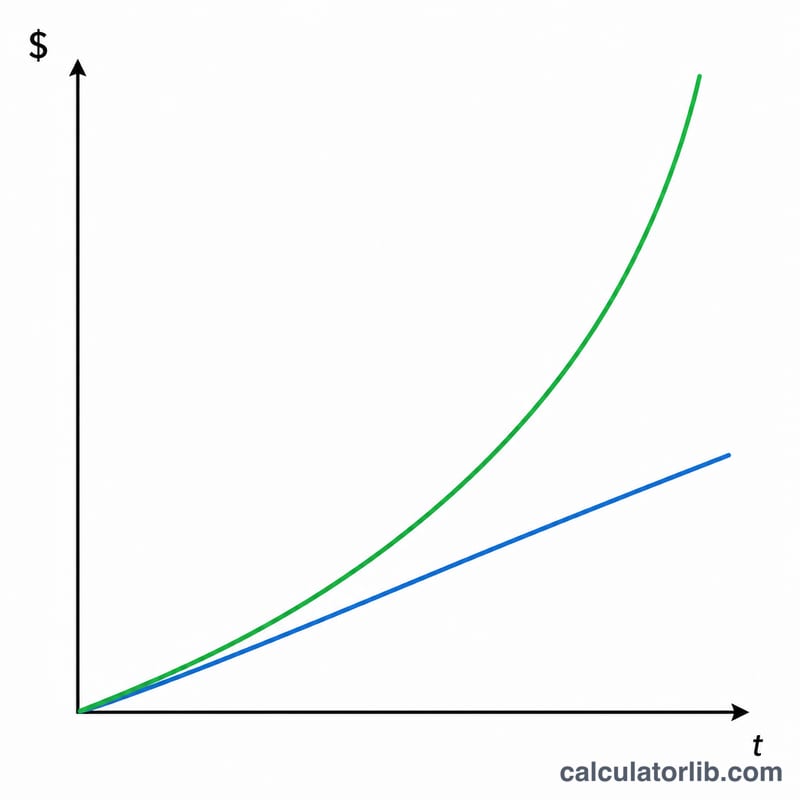

This Interest Rate Calculator works out how much interest your money earns (or costs) over time, showing you both compound interest and simple interest side by side. Enter your starting balance and a few details, and it instantly returns the interest earned and the total final balance under each method — so you can see exactly how much compounding adds compared with a flat simple-interest calculation.

The Inputs You Provide

- Principal Amount – the initial sum you invest or borrow.

- Interest Rate (%) – the annual nominal rate, entered as a percentage (e.g. 5 for 5%).

- Time (years) – how long the money stays invested or borrowed.

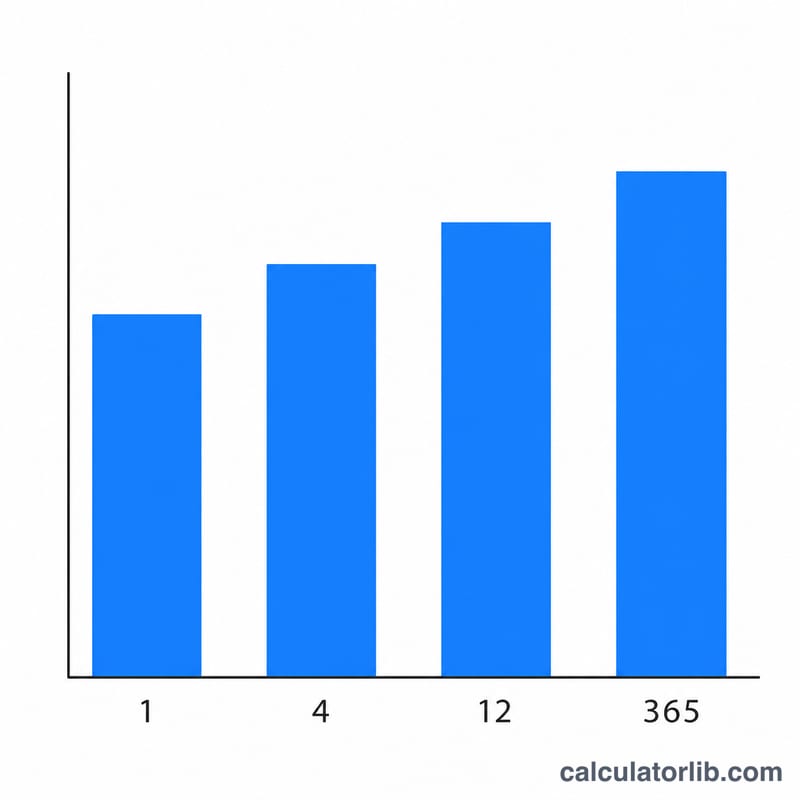

- Compound Frequency – how often interest is added: Annually (1), Semi-annually (2), Quarterly (4), Monthly (12) or Daily (365).

The Formula

For compound interest, the calculator uses:

$$\text{Total Amount} = \text{Principal} \times \left(1 + \frac{\text{Rate}}{\text{Compounds per Year}}\right)^{\text{Compounds per Year} \times \text{Years}}$$

The interest itself is simply Total Amount − Principal. For comparison, it also computes simple interest as Principal × Rate × Time, which ignores compounding entirely.

Worked Example

Suppose you invest a Principal of $10,000 at an Interest Rate of 5% for 3 years, compounded Monthly (frequency = 12).

- Monthly rate \(r = 0.05 \div 12 = 0.0041667\); periods \(n = 12 \times 3 = 36\).

- $$\text{Total Amount} = 10{,}000 \times (1.0041667)^{36} \approx \$11{,}614.72$$

- Compound interest ≈ $1,614.72.

- $$\text{Simple interest} = 10{,}000 \times 0.05 \times 3 = \$1{,}500.00$$

Compounding monthly earns about $114.72 more than the simple-interest method over the same period.

Frequently Asked Questions

Why are there two interest results? The calculator shows both compound and simple interest so you can compare. Most savings accounts, loans and investments use compounding; simple interest is a useful baseline.

Does compound frequency really matter? Yes. The more often interest compounds, the higher the total. Daily compounding earns slightly more than annual at the same nominal rate, because interest starts earning interest sooner.

What currency does it use? The calculator is currency-neutral — it works with whatever unit you enter for the principal, whether dollars, pounds, euros or any other.