What is APY?

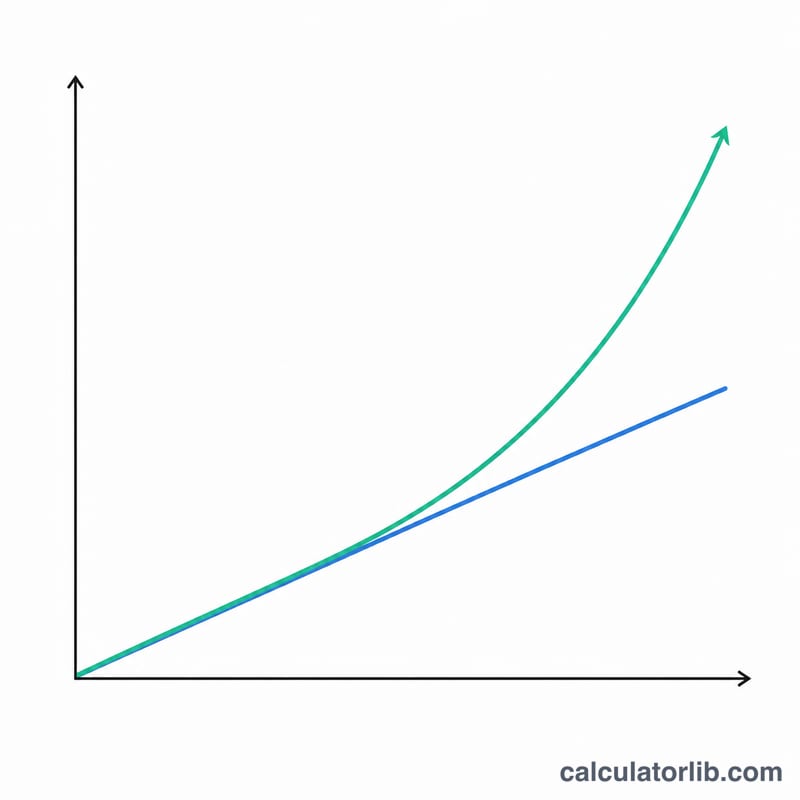

APY (Annual Percentage Yield) is a standardized way to measure the annual return on an investment that factors in the effect of compound interest. Unlike simple interest calculations, APY accounts for how often the interest is compounded during the year, giving you a more accurate picture of your actual returns.

When to Use an APY Calculator

An APY calculator helps you understand the true earning potential of your investments in the following situations:

- Comparing different savings accounts or certificates of deposit (CDs) with different compounding periods

- Planning for long-term investments and understanding how compound interest will grow your money over time

- Evaluating the real returns on fixed-income investments when interest compounds multiple times per year

How to Calculate APY

The formula to calculate APY is:

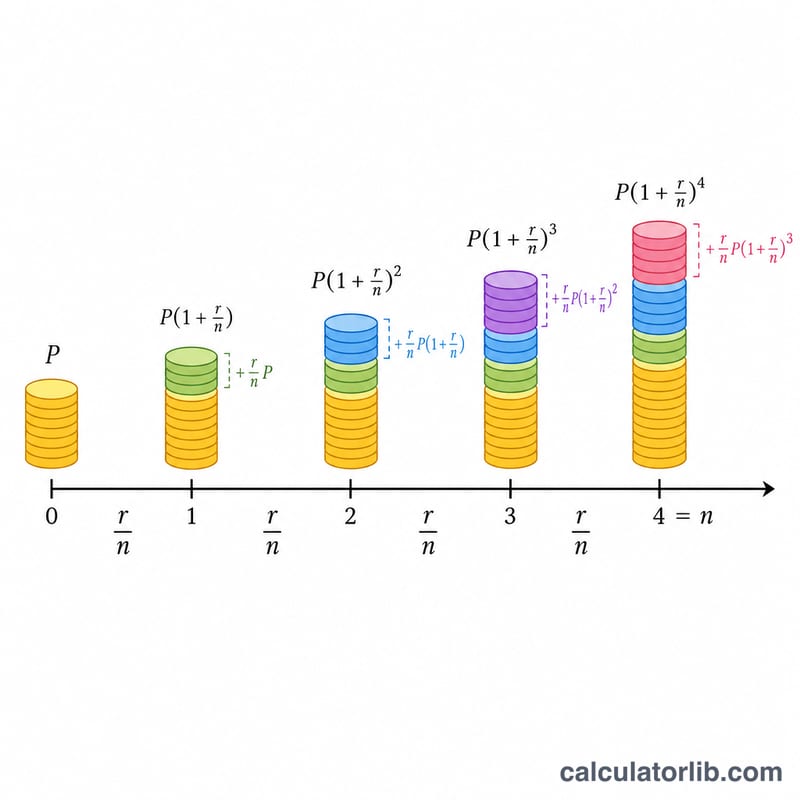

$$\text{APY} = \left(1 + \frac{r}{n}\right)^{n} - 1$$Where:

- \(r\) = Annual interest rate (decimal)

- \(n\) = Number of compounding periods per year

To calculate the final amount after a certain term:

$$\text{Final Amount} = P \times \left(1 + \frac{r}{n}\right)^{n \times t}$$Where:

- \(P\) = Principal (initial investment)

- \(r\) = Annual interest rate (decimal)

- \(n\) = Number of compounding periods per year

- \(t\) = Term in years

The total interest earned is:

$$\text{Total Interest} = \text{Final Amount} - \text{Principal}$$Common Compounding Frequencies

| Compounding Frequency | Number of Times Per Year (n) |

|---|---|

| Daily | 365 |

| Weekly | 52 |

| Monthly | 12 |

| Quarterly | 4 |

| Semi-annually | 2 |

| Annually | 1 |

Examples

Example 1: Calculating APY for a Savings Account

What is the APY for a savings account that offers 2% annual interest rate, compounded monthly?

$$\text{APY} = \left(1 + \frac{0.02}{12}\right)^{12} - 1 = 2.02\%$$| Annual Interest Rate | 2% |

| Compounding Frequency | Monthly (12 times per year) |

| APY | 2.02% |

Example 2: Calculating Final Amount and Total Interest

If you invest $10,000 at 5% annual interest compounded quarterly for 3 years, what will be the final amount and total interest earned?

$$\text{Final Amount} = 10{,}000 \times \left(1 + \frac{0.05}{4}\right)^{4 \times 3} = \$11{,}616.17$$| Principal | $10,000 |

| Annual Interest Rate | 5% |

| Compounding Frequency | Quarterly (4 times per year) |

| Term | 3 years |

| APY | 5.09% |

| Final Amount | $11,616.17 |

| Total Interest | $1,616.17 |

Example 3: Comparing Different Compounding Frequencies

How does the APY differ for a $5,000 investment at 3% annual interest rate with different compounding frequencies over 5 years?

| Compounding Frequency | APY | Final Amount |

|---|---|---|

| Annually (1 time) | 3.00% | $5,796.37 |

| Semi-annually (2 times) | 3.02% | $5,803.89 |

| Quarterly (4 times) | 3.03% | $5,807.77 |

| Monthly (12 times) | 3.04% | $5,810.58 |

| Daily (365 times) | 3.05% | $5,812.82 |

Definitions & Glossary

The terms below appear throughout APY calculations. Understanding each one helps you read the result correctly and compare it with figures advertised by banks and credit unions.

- APY (Annual Percentage Yield) — the effective annual rate of return once compounding is taken into account. It expresses how much your balance actually grows in one year, stated as a single percentage. \(\text{APY} = \left(1 + \frac{r/100}{n}\right)^{n} - 1\).

- APR / Nominal rate (r) — the stated annual interest rate before compounding is applied within the year. It is the rate you typically see quoted on an account, but it understates actual growth whenever interest compounds more than once a year.

- Principal (P) — your initial deposit or investment amount, the starting balance on which interest is first calculated.

- Annual interest rate (r) — the nominal yearly rate, entered as a percentage (e.g. 5 for 5%). In the formula it is divided by 100 to become a decimal.

- Compounding frequency (n) — how many times per year interest is added to the balance: 1 (annual), 2 (semi-annual), 4 (quarterly), 12 (monthly), or 365 (daily).

- Term (t) — the length of time the money stays invested, in years. APY itself is a one-year figure, but the term determines the final balance and total interest.

- Final amount — the balance at the end of the term: \(A = P\left(1 + \frac{r/100}{n}\right)^{n t}\).

- Total interest — the earnings produced over the term, equal to the final amount minus the principal: \(A - P\).

APY vs APR/nominal rate: APR (the nominal rate) tells you the quoted rate; APY tells you the real yearly yield after compounding. When interest compounds only once a year (\(n = 1\)) the two are equal. With more frequent compounding, APY is higher than the nominal rate because you earn interest on previously credited interest.