What Is the Bonus Tax Calculator?

This calculator estimates the take-home (net) amount of a bonus paid in the United States. Bonuses are treated as "supplemental wages" by the IRS. Under the most common method, employers withhold federal income tax at a flat 22% supplemental rate (37% on amounts over $1 million in a year) rather than at your regular paycheck rate. State income tax and FICA (Social Security 6.2% + Medicare 1.45% = 7.65%) are also withheld. This tool reflects the 2024 flat-rate (percentage) method and uses the rates you enter.

How to Use It

Enter your gross bonus amount, then the three withholding rates as percentages. Defaults are the federal supplemental rate of 22%, an example 5% state rate, and the standard 7.65% FICA rate. Adjust the state rate to match your state (some states have no income tax — enter 0). The calculator shows each tax component, the total withheld, your effective withholding rate, and the net bonus you actually receive.

The Formula

The net bonus is computed as Net = Bonus × (1 − r_fed − r_state − r_fica), where each rate is expressed as a decimal. Each individual tax equals the bonus multiplied by that single rate.

Worked Example

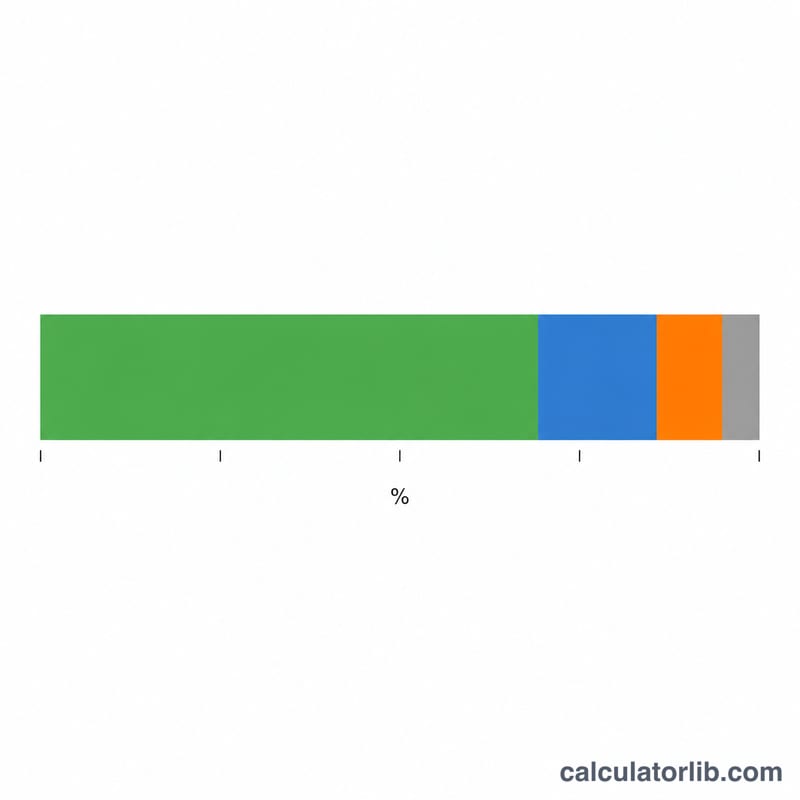

A $10,000 bonus with 22% federal, 5% state, and 7.65% FICA: federal = $2,200, state = $500, FICA = $765. Total withheld = $3,465, so the net bonus is $10,000 − $3,465 = $6,535, an effective rate of 34.65%.

State Supplemental Withholding Rates

When an employer pays a bonus separately from regular wages, many states require a flat supplemental withholding rate rather than running the bonus through normal wage-bracket tables. The figures below reflect commonly cited 2024 state supplemental rates. Several states have no broad personal income tax and therefore withhold nothing on bonuses, while others apply a flat percentage.

| State | 2024 Supplemental Rate | Notes |

|---|---|---|

| Florida (FL) | 0% | No state income tax |

| Texas (TX) | 0% | No state income tax |

| Washington (WA) | 0% | No broad income tax on wages |

| Nevada (NV) | 0% | No state income tax |

| Tennessee (TN) | 0% | No state income tax |

| Wyoming (WY) | 0% | No state income tax |

| South Dakota (SD) | 0% | No state income tax |

| Alaska (AK) | 0% | No state income tax |

| Illinois (IL) | 4.95% | Flat rate |

| Indiana (IN) | 3.05% | Flat rate |

| Colorado (CO) | 4.40% | Flat rate |

| Pennsylvania (PA) | 3.07% | Flat rate |

| Michigan (MI) | 4.25% | Flat rate |

| Arizona (AZ) | 2.50% | Flat rate |

| North Carolina (NC) | 4.50% | Flat supplemental rate |

| Georgia (GA) | 5.39% | Flat supplemental rate |

| New York (NY) | 11.70% | State supplemental rate (NYC adds local) |

| California (CA) | 10.23% | Bonuses/commissions supplemental rate |

Rates change periodically and some states require a different rate for stock options or vacation payouts. Always confirm the current rate with your state revenue department or payroll provider before relying on it.

Bonus Net Pay Across Scenarios

The examples below assume the federal supplemental rate of 22% on amounts up to $1 million, FICA of 7.65% (6.2% Social Security + 1.45% Medicare), and three illustrative state rates: a no-tax state (0%), a mid-tax state (~5%), and a high-tax state (~10.23%, California). For the $1.2M bonus, the portion above $1M is withheld at the mandatory 37% federal supplemental rate.

| Gross Bonus | State Rate | Total Withholding % | Net Bonus | Effective Rate |

|---|---|---|---|---|

| $1,000 | 0% | 29.65% | $703.50 | 29.65% |

| $1,000 | 5% | 34.65% | $653.50 | 34.65% |

| $1,000 | 10.23% | 39.88% | $601.20 | 39.88% |

| $5,000 | 0% | 29.65% | $3,517.50 | 29.65% |

| $5,000 | 5% | 34.65% | $3,267.50 | 34.65% |

| $5,000 | 10.23% | 39.88% | $3,006.00 | 39.88% |

| $25,000 | 0% | 29.65% | $17,587.50 | 29.65% |

| $25,000 | 5% | 34.65% | $16,337.50 | 34.65% |

| $25,000 | 10.23% | 39.88% | $15,030.00 | 39.88% |

| $1,200,000 | 0% | see note | ~$840,200 | ~30.0% |

The $1.2M no-tax-state row reflects 22% on the first $1,000,000 ($220,000) plus 37% on the next $200,000 ($74,000) of federal withholding, with Social Security capping after the annual wage base is met and Medicare (1.45% plus the 0.9% Additional Medicare surtax over $200,000) continuing to apply. Because the Social Security cap and Medicare surtax depend on total year-to-date wages, treat the high-earner figure as an estimate.

Key Terms Explained

- Supplemental wages

- Compensation paid in addition to regular wages, such as bonuses, commissions, overtime, severance, awards, and back pay. The IRS allows employers to withhold federal tax on these using a flat percentage rather than the normal wage-bracket method.

- Federal supplemental rate

- The flat federal income-tax withholding rate applied to supplemental wages — 22% on amounts up to $1,000,000 in a calendar year, and a mandatory 37% on the portion exceeding $1,000,000.

- FICA (Social Security + Medicare)

- Federal Insurance Contributions Act taxes. The employee share is 6.2% for Social Security (up to the annual wage base) plus 1.45% for Medicare, totaling 7.65%. An Additional Medicare Tax of 0.9% applies to wages above $200,000.

- Withholding vs. final tax liability

- Withholding is an estimated prepayment of tax taken from each payment. Your actual tax owed is determined when you file your annual return. If 22% was withheld but your marginal bracket is higher or lower, you settle the difference (refund or balance due) at filing.

- Effective withholding rate

- The total tax withheld divided by the gross bonus, expressed as a percentage. It combines the federal supplemental rate, state rate, and FICA into one figure describing how much of the bonus is held back.

- The $1M threshold

- The point at which mandatory federal supplemental withholding jumps from 22% to 37%. Once an employee's total supplemental wages for the year exceed $1,000,000, every dollar above that threshold must be withheld at 37%.

FAQ

Why is so much taken out of my bonus? The 22% flat federal rate often differs from your marginal rate. If too much was withheld, you may get it back at tax time.

Does this replace my W-2 taxes? No — withholding is an estimate; your final liability is settled when you file your return.

What if my bonus exceeds $1 million? The IRS requires a 37% flat rate on the portion above $1 million; enter that higher rate manually.