What This Calculator Does

The Monthly Payment from APR Calculator converts a loan's headline APR into the actual fixed amount you would pay each month. Enter the loan amount, the annual percentage rate (APR), and the term in months, and it returns your monthly payment along with the total of all payments and the total interest cost over the life of the loan. It works for any standard amortizing loan such as auto loans, personal loans, and fixed-rate mortgages.

How to Use It

Enter three values: the loan amount you are borrowing, the APR quoted by the lender as a percentage, and the term expressed in months (for example, a 5-year loan is 60 months). The calculator assumes monthly compounding and equal payments, which matches how most consumer loans are structured.

The Formula Explained

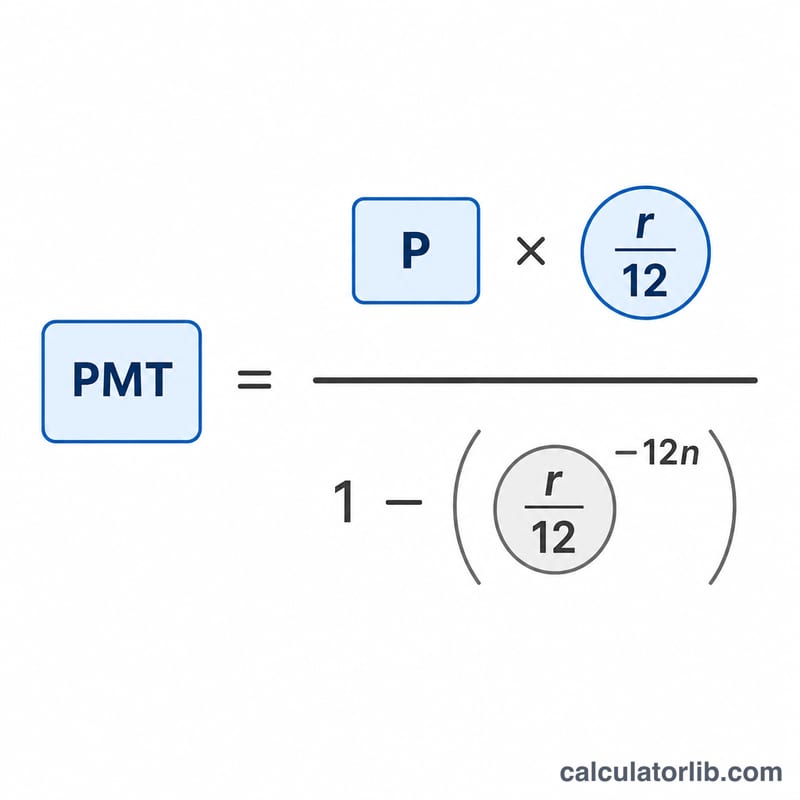

The payment is found with the standard amortization formula:

$$\text{PMT} = P \cdot \frac{r/12}{1 - (1 + r/12)^{-n}}$$

Here \(P\) is the principal, \(r\) is the APR written as a decimal (6% = 0.06), and \(n\) is the number of monthly payments. Dividing the APR by 12 gives the periodic monthly rate. If the rate is zero, the payment is simply the principal divided by the number of months.

Worked Example

Borrow $20,000 at a 6% APR over 60 months. The monthly rate is \(0.06/12 = 0.005\). The payment is $$20000 \times \frac{0.005}{1 - 1.005^{-60}} \approx \$386.66 \text{ per month.}$$ Over 60 months you pay about $23,199.36 in total, of which roughly $3,199.36 is interest.

Monthly Payment Across Loan Scenarios

The tables below apply the fixed-payment amortization formula \( M = P \cdot \dfrac{r}{1 - (1 + r)^{-n}} \) where \( r \) is the monthly rate (APR ÷ 1200) and \( n \) is the term in months. Total of payments is \( M \times n \); total interest is that total minus the principal.

$20,000 at 6% APR — varying the term

| Term | Monthly Payment | Total of Payments | Total Interest |

|---|---|---|---|

| 36 months | $608.44 | $21,903.84 | $1,903.84 |

| 60 months | $386.66 | $23,199.60 | $3,199.60 |

| 72 months | $331.46 | $23,865.12 | $3,865.12 |

$20,000 over 60 months — varying the APR

| APR | Monthly Payment | Total of Payments | Total Interest |

|---|---|---|---|

| 4% | $368.33 | $22,099.80 | $2,099.80 |

| 6% | $386.66 | $23,199.60 | $3,199.60 |

| 8% | $405.53 | $24,331.80 | $4,331.80 |

Two patterns stand out: stretching the same loan from 36 to 72 months cuts the monthly payment by nearly half but roughly doubles the interest paid, and each two-point rise in APR at a fixed term adds about $1,100 in total interest on a $20,000 balance.

Interpreting Your Result

Monthly payment (M) is the fixed amount you pay every month for the life of the loan. Because it is fixed, the same dollar figure covers both interest and principal in every installment — only the split between the two changes over time.

Total of payments is simply the monthly payment multiplied by the number of months (\( M \times n \)). It represents the entire amount of money that will leave your pocket if you keep the loan to maturity and make no extra payments.

Total interest is the total of payments minus the original loan amount: it is the true cost of borrowing, on top of repaying what you received.

Longer terms lower the payment but raise total interest. A longer term spreads the principal over more installments, so each payment is smaller — but you also pay interest on the outstanding balance for more months, so the cumulative interest grows. There is a direct trade-off between monthly affordability and lifetime cost.

APR is treated here as a nominal annual rate compounded monthly. The calculator converts it to a periodic monthly rate by dividing by 12 (\( r = \text{APR}/1200 \) when APR is entered as a percent). Because interest is applied monthly, the effective annual rate (APY) is slightly higher than the stated APR; if you want that figure, an APR-to-APY conversion shows the difference.

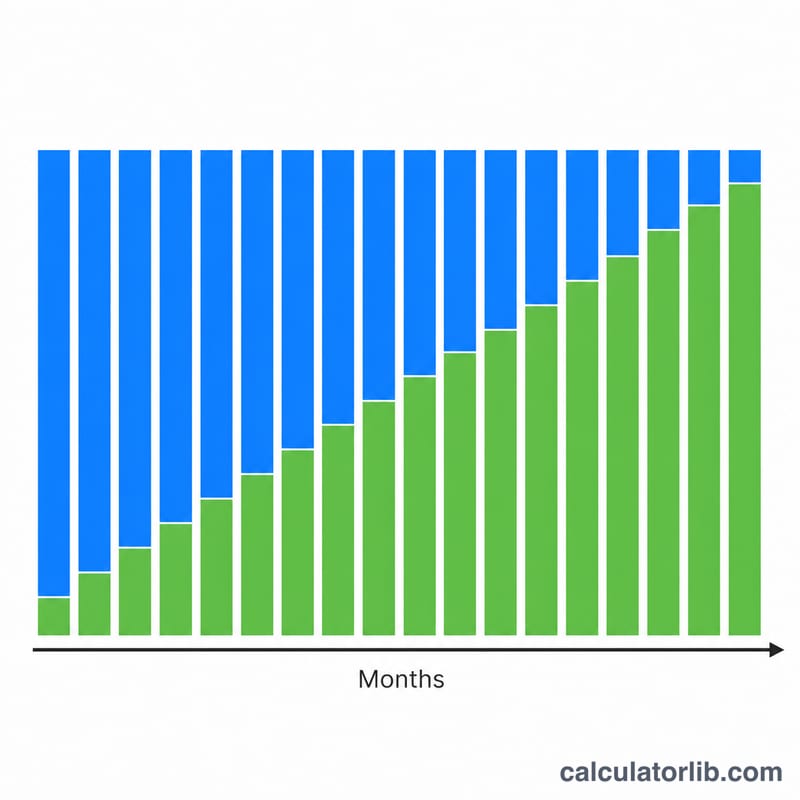

Fixed-payment amortization means early payments are mostly interest. Interest each month is charged on the remaining balance, which is highest at the start. So in the early installments a large share of the fixed payment goes to interest and only a little reduces principal; as the balance falls, the interest portion shrinks and more of each payment chips away at the principal. An amortization schedule shows this shift month by month.

Key Terms Defined

- Principal (P)

- The original amount borrowed — the loan amount before any interest is added. It is the base on which interest is calculated.

- APR (Annual Percentage Rate)

- The stated yearly interest rate on the loan, expressed as a percent. In this calculator it is the nominal rate used to derive the monthly rate.

- Nominal vs. effective rate

- The nominal rate is the quoted annual rate that ignores within-year compounding. The effective rate (APY) reflects the impact of compounding each period and is therefore slightly higher than the nominal rate when interest compounds monthly.

- Periodic monthly rate (r)

- The interest rate applied to the balance each month, found by dividing the annual rate by 12: \( r = \text{APR}/1200 \) when APR is in percent (or APR/12 in decimal form).

- Term (n)

- The total number of monthly payments over the life of the loan — for example, a 5-year loan has \( n = 60 \).

- Amortization

- The process of paying off a loan through equal periodic payments, where each payment covers the interest due plus a portion of principal, gradually reducing the balance to zero by the final payment.

- Total of payments

- The sum of every scheduled payment over the term, equal to the monthly payment times the number of months (\( M \times n \)).

- Total interest

- The total cost of borrowing: the total of payments minus the principal (\( M \times n - P \)).

FAQ

Is APR the same as interest rate? Not always. APR can include certain fees, but this tool treats APR as the nominal annual rate compounded monthly, which is standard for installment loans.

What if I enter 0% APR? The calculator simply divides the loan amount by the number of months, since there is no interest.

Does this include taxes or insurance? No. It computes principal-and-interest only. Add escrow items like property tax or insurance separately.