What This Calculator Does

Most loan tools start with a loan amount and tell you the monthly payment. This calculator works in reverse: you tell it the monthly payment you can comfortably afford, the interest rate, and the loan term, and it tells you the maximum loan amount (principal) that fits that budget. It's ideal for shopping for a car, mortgage, or personal loan when you know exactly how much you can pay each month.

How to Use It

Enter the monthly payment you want to make, the annual percentage rate (APR) offered by the lender, and the loan term in months (for example, 60 months for a 5-year loan). The calculator returns the loan amount you can finance, the total of all payments over the life of the loan, and the total interest you will pay.

The Formula Explained

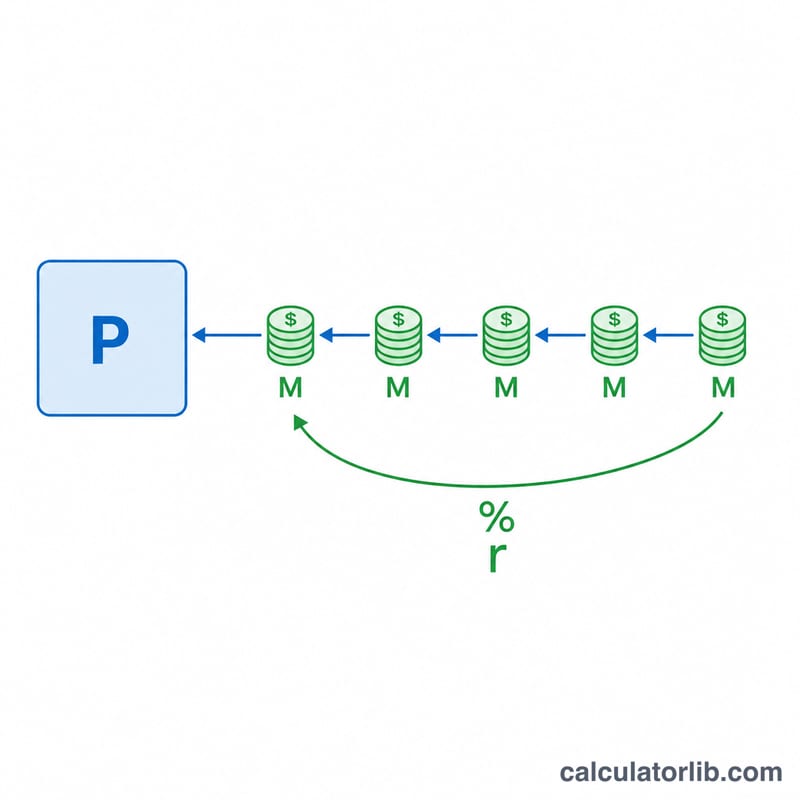

The loan amount is the present value of an annuity: $$P = M \times \frac{1 - (1+r)^{-n}}{r}$$ Here \(M\) is the monthly payment, \(r\) is the monthly interest rate (APR \(\div\) 12 \(\div\) 100), and \(n\) is the number of months. When the interest rate is zero, the formula simplifies to \(P = M \times n\), because there is no interest cost.

Worked Example

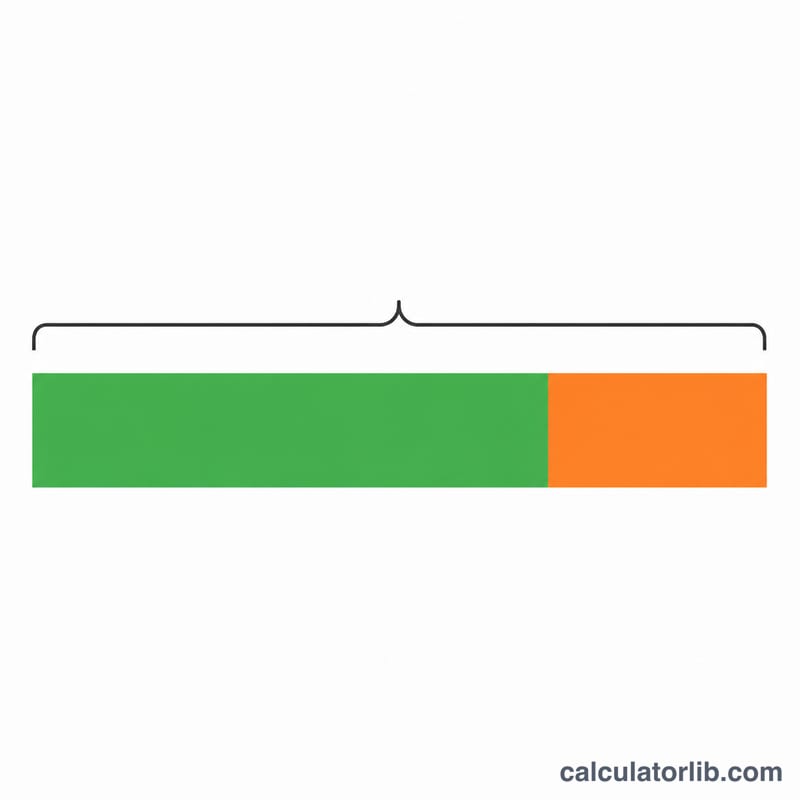

Suppose you can pay $500 per month at 6% APR for 60 months. The monthly rate is \(r = 6 \div 12 \div 100 = 0.005\). Then $$P = 500 \times \frac{1 - 1.005^{-60}}{0.005} \approx \$25{,}862.78$$ You will pay \(500 \times 60 = \$30{,}000\) in total, of which about $4,137.22 is interest.

FAQ

Does a higher APR let me borrow more? No. For the same payment, a higher rate means more of each payment goes to interest, so the principal you can afford goes down.

What if the rate is 0%? The loan amount is simply your payment multiplied by the number of months.

Is this an estimate? Yes. It assumes fixed payments and a constant rate, and excludes fees, taxes, or insurance that may be bundled into your actual payment.