What this calculator does

This loan calculator solves an amortizing loan for any one of four quantities: the monthly payment, the loan amount (principal), the annual interest rate, or the number of monthly payments. You supply the three values you know, choose which one to solve for, and the tool computes the fourth. It assumes monthly compounding equal to the payment frequency, which is the standard convention for consumer loans such as auto loans, personal loans, and fixed-rate mortgages.

How to use it

Pick a calculation from the dropdown. The quantity you choose becomes the output, so its input box is ignored. Fill in the remaining three fields, then read the highlighted result. The calculator also reports the total amount paid over the life of the loan and the total interest. Tick "Show Solution Steps" to display the underlying algebra.

The formula explained

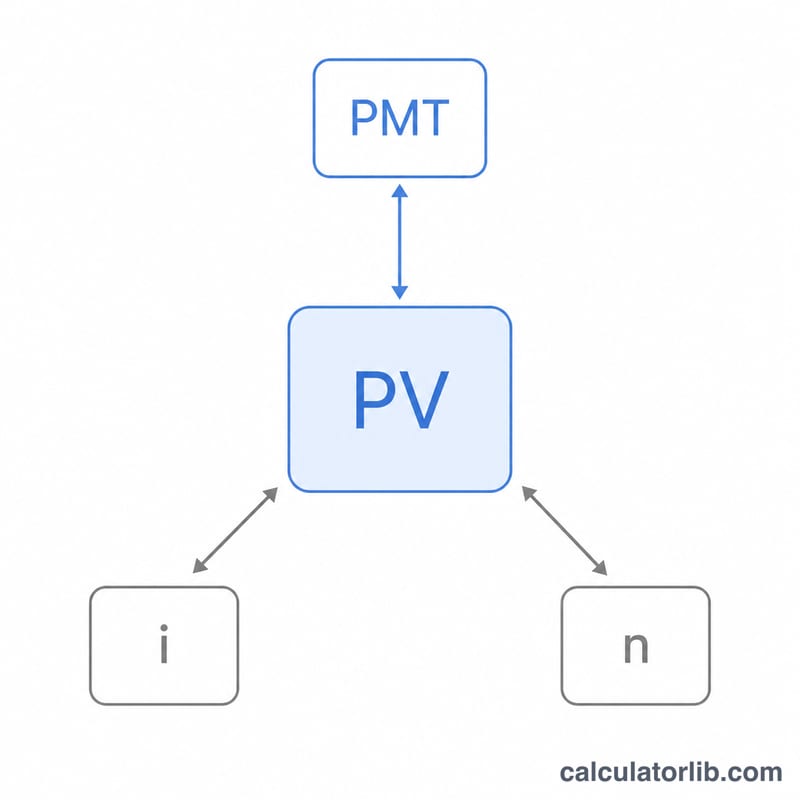

The core relationship is the present value of an ordinary annuity:

$$PV = \frac{PMT}{i}\left[1 - (1+i)^{-n}\right]$$

Here \(i\) is the per-month interest rate (annual rate divided by 100 then by 12) and \(n\) is the number of monthly payments. Solving for the payment gives $$PMT = \frac{PV \cdot i}{1 - (1+i)^{-n}}.$$ The term \(n\) is found with logarithms, and the interest rate has no closed form, so it is solved numerically by bisection. When the interest rate is zero, the linear forms \(PMT = PV/n\), \(PV = PMT \cdot n\), and \(n = PV/PMT\) are used.

Worked example

Borrow $25,000 at 6% annual interest for 60 months. The monthly rate is \(i = 6/100/12 = 0.005\). With \((1.005)^{60} \approx 1.34885\), the payment is $$\frac{25000 \times 0.005 \times 1.34885}{1.34885 - 1} \approx \mathbf{\$483.32}.$$ Total paid is \(483.32 \times 60 = \$28{,}999.20\), so total interest is about $3,999.20.

FAQ

Why does the interest rate solver use a numerical method? The annuity equation cannot be rearranged algebraically for \(i\), so the tool searches for the rate that reproduces your inputs.

What if my payment is too small to find a term? If the monthly payment does not even cover the monthly interest, the balance grows forever and no term exists; the calculator returns an error.

Does this handle different compounding frequencies? No. It assumes monthly compounding matched to monthly payments, the most common consumer-loan setup.