What This Calculator Does

The Simple Loan Calculator works out the fixed monthly payment on an amortizing loan, plus the total interest you will pay and the total cost over the life of the loan. It works for personal loans, car loans, mortgages, and any installment loan with a constant payment. The math is universal — the dollar sign is cosmetic and the same formula applies in any currency.

How to Use It

Enter three things: the Loan Amount (the principal you borrow), the annual Interest Rate as a percentage, and the Loan Term with its time unit (years or months). The calculator converts the annual rate to a monthly rate, converts the term to a number of monthly payments, and returns your payment instantly.

The Formula Explained

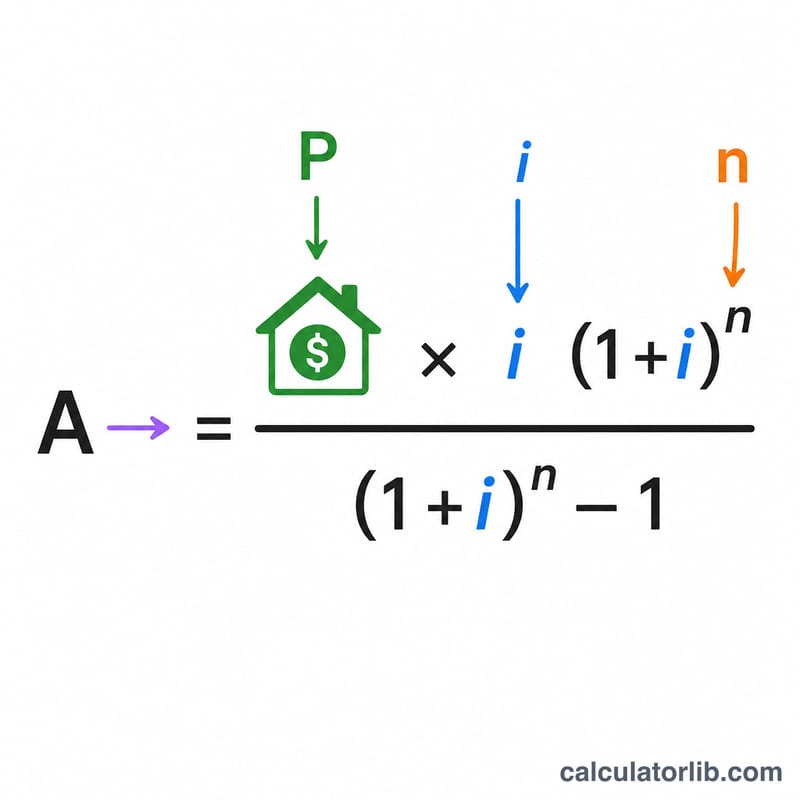

An amortizing loan is paid off with equal monthly payments. Each payment covers that month's interest first, and the rest reduces the balance. The standard annuity payment formula is:

$$A = P \cdot \dfrac{i\,(1+i)^n}{(1+i)^n - 1}$$

where P is the principal, i is the monthly interest rate (annual rate divided by 100, then by 12), and n is the total number of monthly payments. If the interest rate is 0%, the formula simplifies to \(A = P / n\).

Worked Example

Borrow $20,000 at 5% annual interest for 5 years. The monthly rate is \(i = 0.05 / 12 = 0.0041667\), and \(n = 5 \times 12 = 60\) payments. Then \((1+i)^{60} = 1.28336\), so $$A = 20000 \times \frac{0.0041667 \times 1.28336}{1.28336 - 1} = \$377.42$$ per month. Total paid \(= 377.42 \times 60 = \$22{,}645.48\), so total interest = $2,645.48.

FAQ

Is interest compounded monthly? Yes. This calculator uses standard monthly compounding, the convention for most consumer loans.

What if my rate is 0%? The payment is simply the principal divided by the number of months, with no interest charged.

Does this include fees or insurance? No. It computes pure principal-and-interest payments. Add any origination fees, taxes, or insurance separately.