What is an amortized loan calculator?

An amortized loan is repaid with a fixed periodic payment that covers both interest and principal. Early payments are mostly interest; later payments are mostly principal, but the payment amount stays the same. This calculator computes that fixed payment along with the total amount you will pay and the total interest cost over the life of the loan. The math is universal standard amortization, used for mortgages, car loans and personal loans worldwide, and is not specific to any country.

How to use it

Enter the Loan Amount (the principal you borrow), the Interest Rate (Annual %) as a nominal APR, and the Loan Term with its unit (years or months). Choose how many Payments per Year you make (monthly is standard). The tool returns your payment per period, the total of all payments, the total interest paid and the number of payments.

The formula explained

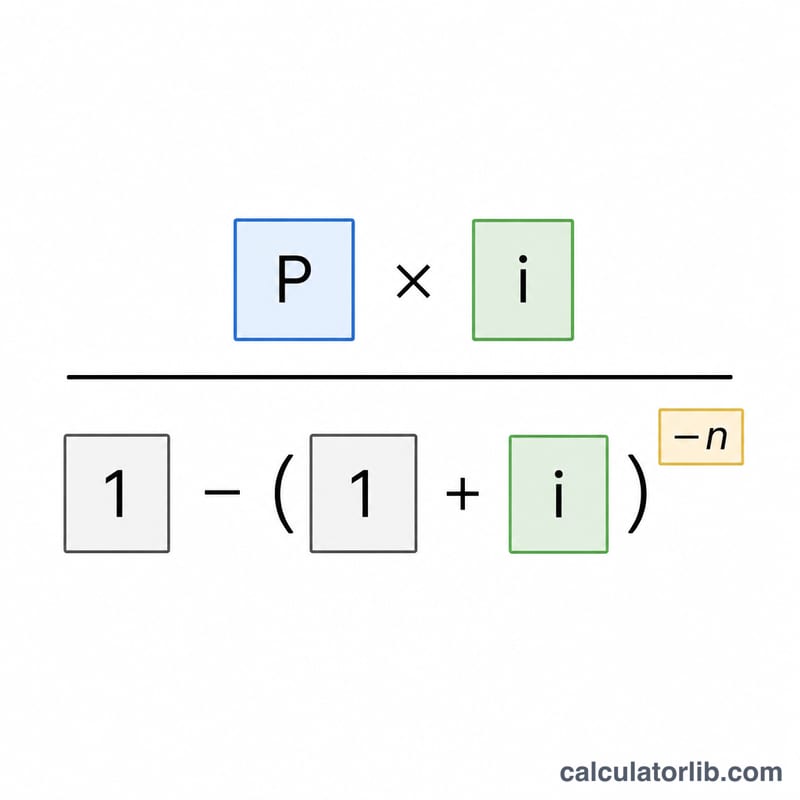

Let \(P\) be the principal, \(m\) the payments per year, \(n\) the total number of payments and \(i\) the periodic rate (annual rate as a decimal divided by \(m\)). The payment is $$\text{Payment} = \frac{P \cdot i}{1 - (1 + i)^{-n}}$$ If the rate is zero, the denominator collapses, so the payment is simply \(P / n\). Total paid is \(\text{Payment} \cdot n\), and total interest is $$\text{Interest} = \text{Payment} \cdot n - P$$

Worked example

Borrow 100,000 at 6% APR for 30 years, paid monthly. Then \(m = 12\), \(n = 360\), and \(i = 0.06 / 12 = 0.005\). $$\text{Payment} = \frac{100{,}000 \cdot 0.005}{1 - 1.005^{-360}} = \frac{500}{0.83396} = 599.55 \text{ per month}$$ Total paid \(= 599.55 \cdot 360 = 215{,}838.19\), and total interest \(= 215{,}838.19 - 100{,}000 = 115{,}838.19\).

Payment & Interest Across Loan Scenarios

The table below shows how the monthly payment, total of payments and total interest change for a fixed principal of \(P = \$100{,}000\) across three annual percentage rates and three loan terms. All figures use monthly compounding (\(m = 12\)) and the amortization formula \(\text{Payment} = \dfrac{P \cdot i}{1 - (1 + i)^{-n}}\), where \(i\) is the monthly rate and \(n\) is the total number of payments.

| APR | Term | Monthly Payment | Total Paid | Total Interest |

|---|---|---|---|---|

| 4% | 15 yr (180 pmts) | $739.69 | $133,144.20 | $33,144.20 |

| 4% | 20 yr (240 pmts) | $605.98 | $145,435.20 | $45,435.20 |

| 4% | 30 yr (360 pmts) | $477.42 | $171,871.20 | $71,871.20 |

| 6% | 15 yr (180 pmts) | $843.86 | $151,894.80 | $51,894.80 |

| 6% | 20 yr (240 pmts) | $716.43 | $171,943.20 | $71,943.20 |

| 6% | 30 yr (360 pmts) | $599.55 | $215,838.00 | $115,838.00 |

| 8% | 15 yr (180 pmts) | $955.65 | $172,017.00 | $72,017.00 |

| 8% | 20 yr (240 pmts) | $836.44 | $200,745.60 | $100,745.60 |

| 8% | 30 yr (360 pmts) | $733.76 | $264,153.60 | $164,153.60 |

Reading down each APR block shows the core trade-off: extending the term lowers the monthly payment but increases the total interest. Reading across the same term shows that each two-percentage-point rise in APR adds substantially to both the payment and the lifetime cost.

What Your Results Mean

The calculator returns three related figures:

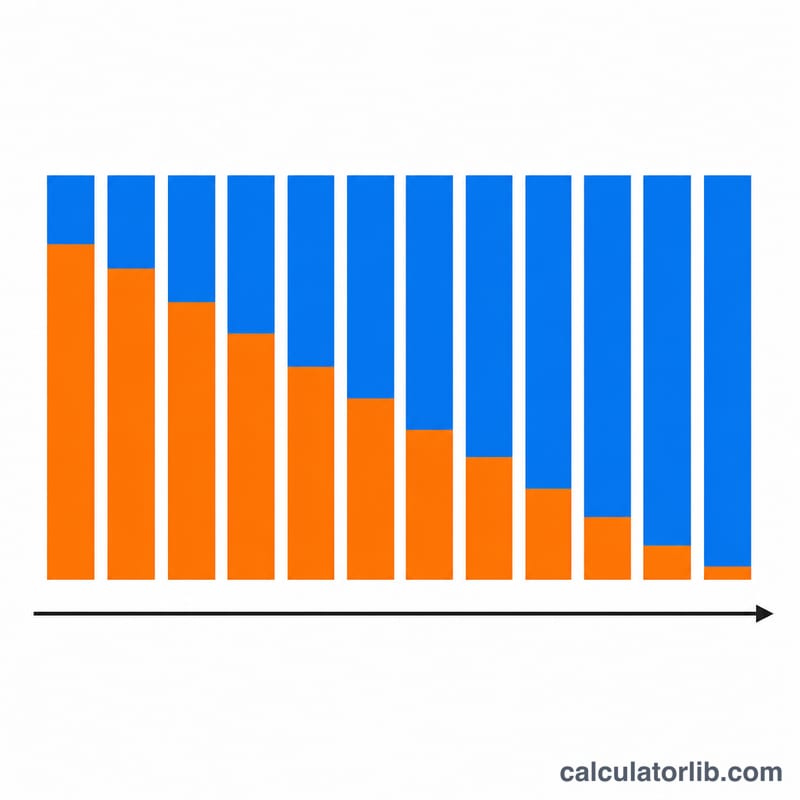

- Monthly payment — the fixed amount due each period that fully repays the loan over its term. Each payment is split between interest on the outstanding balance and a portion of principal; early payments are mostly interest, later payments mostly principal.

- Total of payments — the monthly payment multiplied by the number of payments \(n\). This is the full amount of cash that leaves your account over the life of the loan.

- Total interest — the total of payments minus the original principal \(P\). It is the cost of borrowing, i.e. everything paid beyond what was lent.

A longer term lowers the monthly payment because the same principal is spread over more periods, but it raises total interest because the balance is carried for longer and accrues interest over more periods. A shorter term does the opposite: a higher payment but less interest overall.

The APR is an annual nominal rate. The calculator converts it to a periodic rate by dividing by the number of payments per year: \(i = \dfrac{\text{APR}}{m}\). For a 6% APR paid monthly, the periodic rate is \(i = 0.06 / 12 = 0.005\) (0.5% per month). The number of payments is \(n = \text{years} \times m\). Because interest compounds on the declining balance each period, even a small change in the periodic rate changes the payment and total interest noticeably.

This is general educational information about how amortized loans work, not personal financial advice. Actual offers may include fees, insurance or compounding conventions that differ from this simplified model.

Key Terms & Variables

| Term | Symbol | Definition |

|---|---|---|

| Principal | \(P\) | The original amount borrowed, before any interest is added. |

| Nominal APR | — | The stated annual interest rate quoted on the loan, expressed as a percent per year before conversion to a periodic rate. |

| Periodic rate | \(i\) | The interest rate applied each payment period, equal to the APR divided by the number of payments per year: \(i = \text{APR}/m\). |

| Payments per year | \(m\) | How many payments are made annually (e.g. 12 for monthly, 26 for biweekly, 52 for weekly). |

| Number of payments | \(n\) | Total payments over the full term, \(n = \text{years} \times m\); it is the exponent in the amortization formula. |

| Amortization | — | The process of repaying a loan through equal periodic payments, each covering current interest plus a portion of principal until the balance reaches zero. |

| Total interest | — | The sum of all interest paid over the loan, equal to the total of payments minus the principal. |

FAQ

Is the interest rate nominal or effective? It is treated as a nominal annual rate (APR) and divided by payments per year to get the periodic rate, the standard amortization convention.

Why might my real payment differ by a few cents? Lenders round each payment to the cent, so the final scheduled payment can adjust slightly. The summary here uses the exact formula.

What if the rate is 0%? The payment is simply the principal divided evenly across all payments, and total interest is zero.