What Is a VA Loan Calculator?

This calculator applies to United States VA home loans backed by the U.S. Department of Veterans Affairs. It estimates your monthly mortgage payment (principal and interest) after rolling the VA funding fee into your loan balance. VA loans typically require no down payment and no private mortgage insurance, but most borrowers pay a one-time funding fee that is usually financed into the loan.

How to Use It

Enter the home price, any down payment, your VA funding fee rate (commonly 1.25%–3.3% depending on down payment and prior VA loan use), the interest rate, and the loan term. The tool computes the financed loan amount and shows your estimated monthly payment, total interest, and total of payments.

The Formula Explained

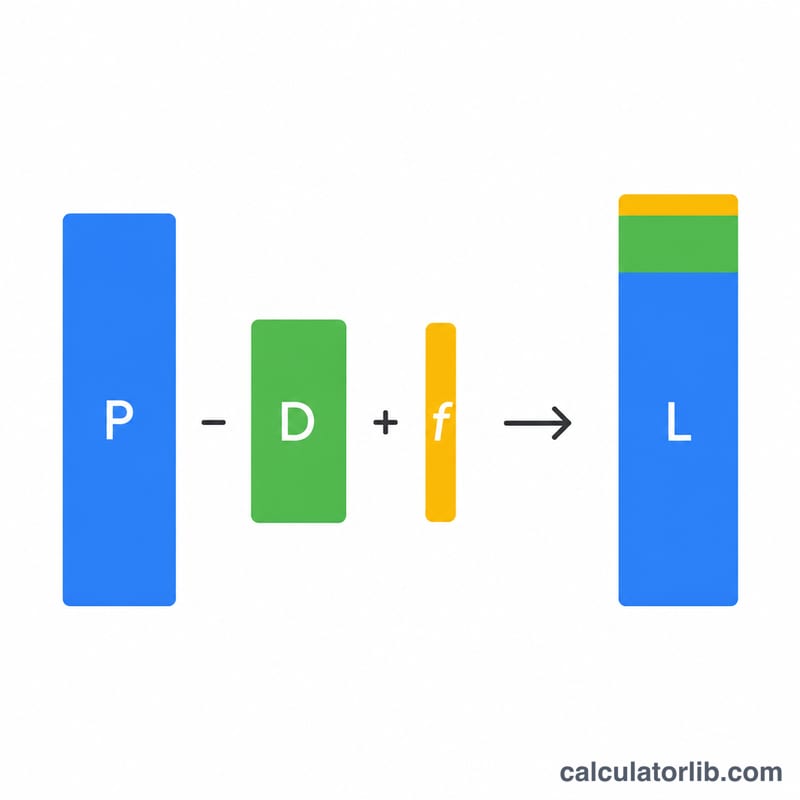

The base loan equals home price minus down payment. The funding fee equals the base loan times the fee rate, and it is added to form the total loan L. The monthly payment uses the standard amortization formula

$$M = L \cdot \frac{r\,(1+r)^{n}}{(1+r)^{n}-1}$$where \(r\) is the monthly interest rate (annual rate \(\div\) 12) and \(n\) is the number of months (years \(\times\) 12).

Worked Example

A $300,000 home with $0 down and a 2.15% funding fee gives a base loan of $300,000 and a fee of $6,450, for a total loan of $306,450. At 6.5% over 30 years (360 payments), the monthly rate is about \(0.0054167\), producing a monthly payment of roughly $1,937.

$$M = 306{,}450 \cdot \frac{0.0054167\,(1+0.0054167)^{360}}{(1+0.0054167)^{360}-1} \approx 1{,}937$$

FAQ

Is the funding fee always financed? No — you can pay it at closing instead, which lowers your loan amount and monthly payment.

Are taxes and insurance included? No. This estimate covers principal and interest only; add property taxes, homeowners insurance, and any HOA dues separately.

Who is exempt from the funding fee? Veterans receiving VA disability compensation and certain surviving spouses may be exempt — set the fee rate to 0 in that case.