What Is a 403(b) Plan?

This calculator applies to the United States. A 403(b) is a tax-advantaged retirement savings plan offered to employees of public schools, certain nonprofits (501(c)(3) organizations), and some ministers. It works much like a 401(k): contributions are typically made pre-tax through payroll deduction and grow tax-deferred until withdrawal. This tool estimates how large your 403(b) balance could grow by retirement based on your contributions and an assumed rate of return. It is a projection, not financial advice, and does not model IRS contribution limits, employer matches, fees, or taxes.

How to Use It

Enter your current 403(b) balance, the amount you contribute each month, your expected average annual return (commonly 5%–8% for a diversified portfolio), and the number of years until you retire. The calculator compounds your contributions monthly and adds the growth of your existing balance to project a total future value.

The Formula Explained

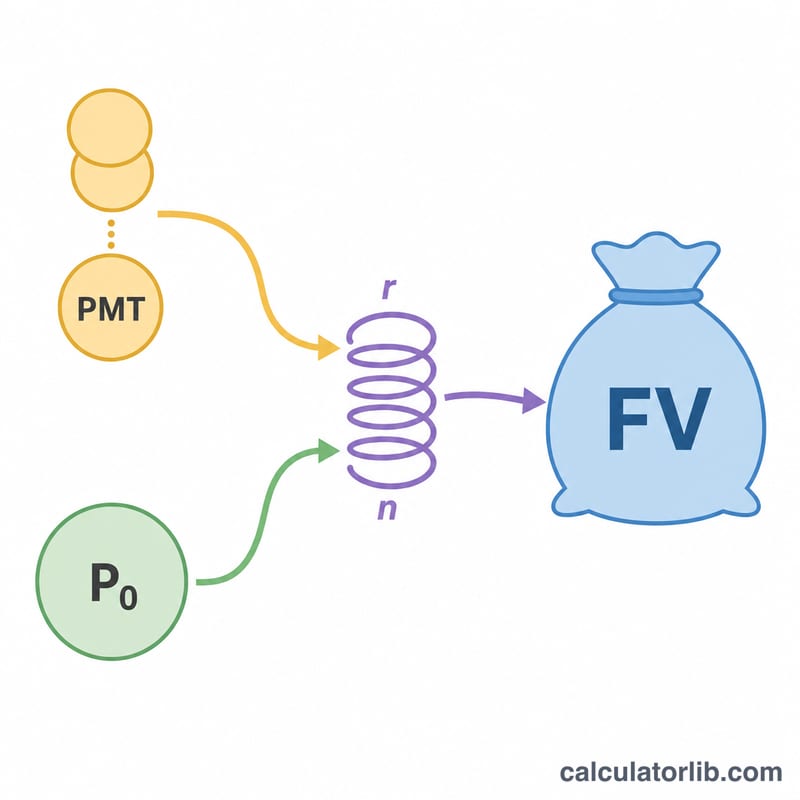

The core formula is the future value of an ordinary annuity: $$\text{FV} = \text{PMT} \times \frac{(1+r)^n - 1}{r}$$ where \(r\) is your monthly return (annual return \(\div\) 12) and \(n\) is the total number of months (years \(\times\) 12). Any existing balance grows separately as \(\text{P}_0 (1+r)^n\). The two are summed for your projected balance.

Worked Example

Suppose you start with $0, contribute $500 per month at a 6% annual return for 30 years. Then \(r = 0.06 \div 12 = 0.005\) and \(n = 360\). $$\text{FV} = 500 \times \frac{1.005^{360} - 1}{0.005} \approx 500 \times 1004.5150 \approx \$502{,}257$$ Of that, you contributed $180,000, so roughly $322,257 came from investment growth.

2024 IRS 403(b) Contribution Limits

A 403(b) plan is a tax-advantaged retirement account for employees of public schools, certain non-profits, and some ministers. The IRS sets annual limits on how much can be contributed. The figures below apply to the 2024 tax year and are indexed for inflation, so they typically rise in later years.

| Limit Type | 2024 Amount | Who It Applies To |

|---|---|---|

| Elective deferral limit | $23,000 | All participants (your own salary deferrals) |

| Age 50+ catch-up | $7,500 | Participants age 50 or older by year-end |

| 15-years-of-service catch-up | $3,000 | Eligible long-tenured employees of qualifying organizations (lifetime cap of $15,000) |

| Overall combined limit | $69,000 | Total of employee + employer contributions (excludes age-50 catch-up) |

The 15-years-of-service catch-up and the age-50 catch-up can both apply in the same year if you qualify, which can meaningfully raise the amount you funnel into the monthly contribution figure used by this calculator. Always confirm current-year limits with the IRS or your plan administrator, as these amounts are indexed annually.

Interpreting Your Projection

The projected balance is a nominal, pre-tax estimate. It does not account for inflation, so a $1,000,000 balance 30 years from now will buy considerably less than $1,000,000 buys today. To gauge purchasing power, consider adjusting the result for an assumed average inflation rate.

Several real-world factors are intentionally excluded from the basic formula:

- Fees: Investment expense ratios, administrative fees, and advisory fees reduce your effective return. A return assumption of 7% might net closer to 6% after a 1% annual fee drag.

- Employer match: Some 403(b) plans offer matching contributions. This calculator counts only your own monthly contribution, so adding a match would increase the result.

- Taxes: Traditional 403(b) contributions and growth are tax-deferred, but withdrawals in retirement are taxed as ordinary income. Your spendable amount will be lower than the projected balance. A Roth 403(b), by contrast, is funded with after-tax dollars and qualified withdrawals are tax-free.

The dominant driver of the final figure is compounding over time: returns earned each period themselves earn returns in future periods. Because of this, starting earlier — even with smaller amounts — often beats starting later with larger amounts.

This is general educational information, not personal financial or tax advice. Consult a qualified professional about your specific situation.

Key Terms Defined

- Present value / current balance (\(P_0\))

- The amount already in your 403(b) today. It grows on its own for the full projection period.

- Monthly contribution (\(PMT\))

- The fixed amount you add to the account each month. Assumed constant in this model, though many people increase it over time.

- Monthly return (\(r\))

- The expected annual return expressed per month: \(r = \frac{\text{annual rate}}{1200}\). For example, a 6% annual return gives \(r = 0.005\).

- Number of periods (\(n\))

- The total number of monthly contributions, equal to \(12 \times \text{years}\). Over 30 years, \(n = 360\).

- Future value (\(FV\))

- The projected total balance at retirement, combining the grown current balance and the accumulated value of all contributions.

- Tax-deferred growth

- Earnings inside a traditional 403(b) are not taxed each year; taxes are deferred until withdrawal, allowing the full balance to compound.

- Employer match

- Contributions your employer adds, often as a percentage of your own deferral up to a cap. Free money that accelerates growth, but not included in this calculator's core formula.

FAQ

Are 403(b) and 401(k) the same? They are very similar tax-advantaged plans; 403(b)s are for schools and nonprofits, while 401(k)s are typically offered by for-profit employers.

What return rate should I assume? Many planners use 5%–7% as a conservative long-term average, but past performance does not guarantee future results.

Does this include taxes or contribution limits? No. Withdrawals from a traditional 403(b) are taxed as income, and the IRS sets annual contribution limits that this tool does not enforce.