What Is the Rule of 25?

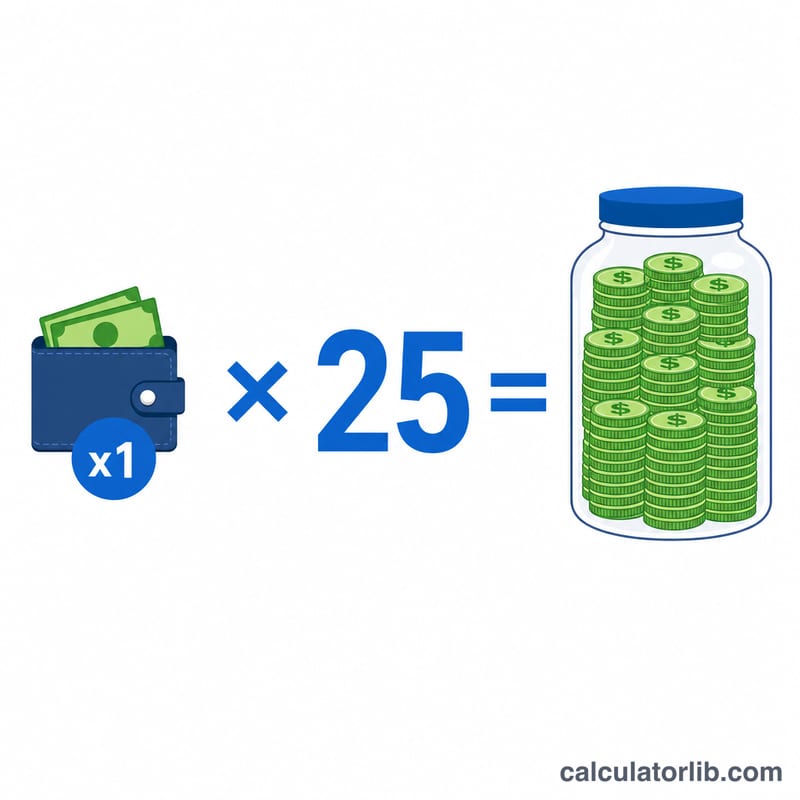

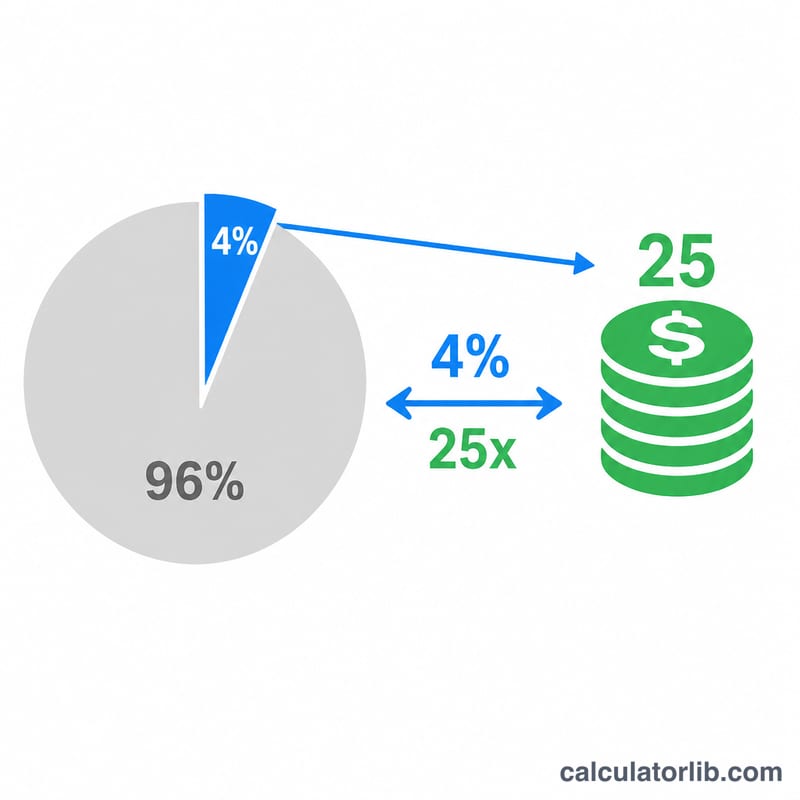

The Rule of 25 is a quick way to estimate how much money you need to retire. It says your target nest egg should equal 25 times your annual living expenses. The rule is the mirror image of the well-known 4% safe withdrawal rule: if you can safely withdraw about 4% of your portfolio each year, then you need \(100 \div 4 = 25\) years of expenses saved. It's a popular benchmark in the FIRE (Financial Independence, Retire Early) community.

How to Use This Calculator

Enter the amount you expect to spend each year in retirement, then keep the multiplier at 25 (or adjust it if you prefer a more conservative 30× or a more aggressive 20×). The calculator multiplies the two to give your retirement number, and also shows the implied withdrawal rate and your equivalent monthly spending.

The Formula Explained

The core math is simply: $$\text{Nest Egg} = \text{Annual Expenses} \times \text{Multiplier}$$. The default multiplier of 25 corresponds to a 4% withdrawal rate (\(100 \div 25 = 4\%\)). Choosing 30 instead implies a more cautious 3.33% withdrawal, requiring a larger portfolio; choosing 20 implies 5%, requiring less but carrying more risk of running out of money.

Worked Example

Suppose you expect to spend $40,000 per year in retirement. Using the Rule of 25: $$\$40{,}000 \times 25 = \$1{,}000{,}000$$ So you'd aim for a $1 million portfolio, from which a 4% withdrawal of $40,000 covers your first-year expenses.

FAQ

Is the Rule of 25 guaranteed? No. It's based on historical market data (notably the Trinity Study) and assumes a diversified portfolio over roughly a 30-year retirement. Markets and longevity vary.

Should I adjust for inflation? Use your expected retirement-year expenses in today's dollars; the 4% rule assumes withdrawals rise with inflation each year.

Does this include taxes? No. Estimate your annual expenses to include taxes, healthcare, and other costs so the result is realistic.