What Is the Retirement Withdrawal Calculator?

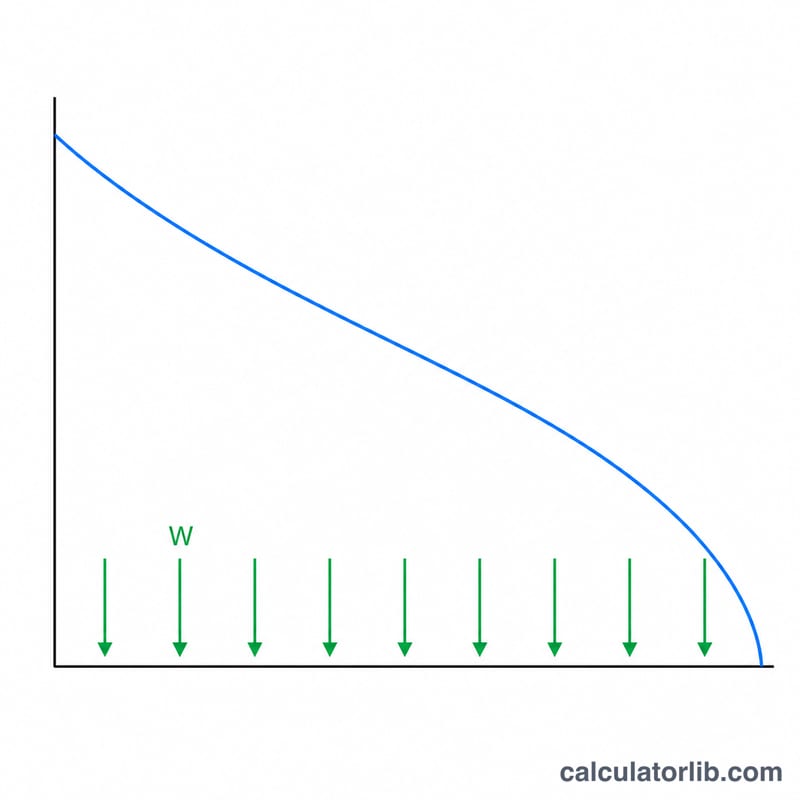

This calculator tells you how much money you can withdraw from your retirement savings each period — monthly, quarterly, or annually — so that the balance is fully drawn down over a chosen number of years while the remaining money keeps earning a steady return. It is the annuity payout (amortization) formula applied to your nest egg, and it is currency- and country-neutral: the math works regardless of where you live.

How to Use It

Enter your current savings balance, the annual rate of return you expect your investments to earn, the number of years you want the income to last, and how often you plan to withdraw. The calculator converts the annual rate into a periodic rate and computes the level payment that exhausts the account at the end of the term.

The Formula Explained

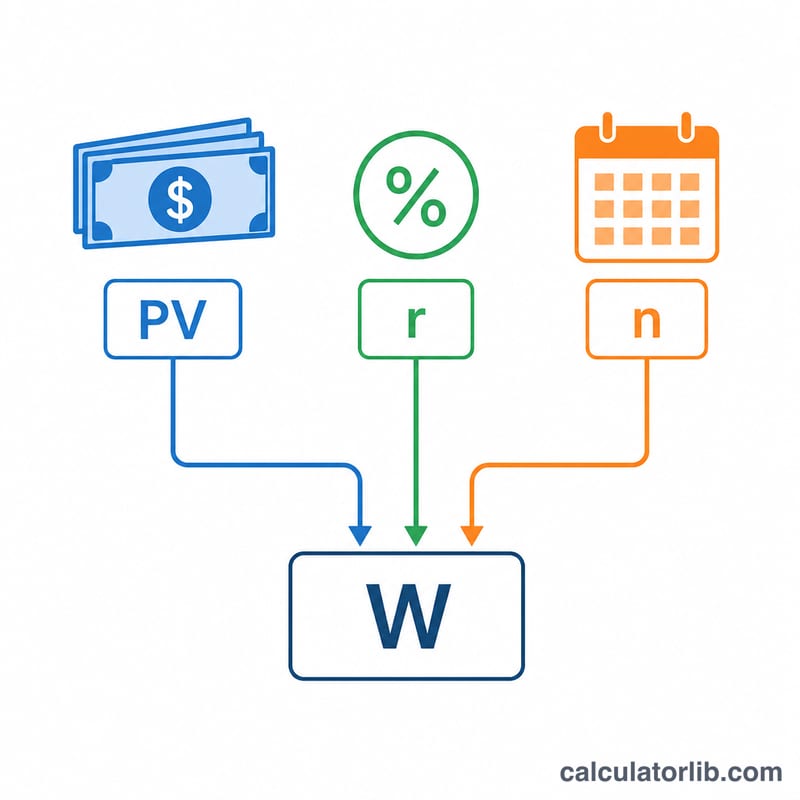

The core equation is $$W = \frac{PV \times r}{1 - (1 + r)^{-n}}$$ where PV is the present balance, r is the periodic return rate (annual rate ÷ frequency), and n is the total number of withdrawals (years × frequency). If the return rate is 0%, the formula simplifies to \(PV \div n\).

Worked Example

Suppose you have $500,000, expect a 5% annual return, want income for 25 years, and withdraw monthly. Then \(r = 0.05/12 \approx 0.0041667\) and \(n = 300\). Plugging in gives a withdrawal of about $2,922.95 per month, totaling roughly $876,886 over 25 years — the extra above your $500,000 comes from continued growth.

FAQ

Does it account for inflation? No — it assumes a constant withdrawal and a constant nominal return. To approximate real (inflation-adjusted) income, enter your return rate minus expected inflation.

What happens at the end of the term? The balance reaches exactly zero after the final withdrawal, assuming the actual return matches your input.

Can I make it last forever? Yes — if you only withdraw the periodic interest \((PV \times r)\), the principal is never touched, but that requires a longer or "perpetual" horizon rather than a fixed term.