What Is a Savings Withdrawal Calculator?

A savings withdrawal calculator tells you the fixed amount you can take out of a savings account or investment each period — monthly, quarterly, or yearly — so that the balance is exactly depleted by the end of a chosen time horizon. Because your remaining balance keeps earning interest, you can usually withdraw more in total than you originally deposited. This is the same math used for retirement drawdown planning and annuity payouts.

How to Use It

Enter your current savings balance, the annual interest rate your account earns, the number of years you want the money to last, and how often you plan to withdraw. The calculator returns the level payment per period, the total number of withdrawals, the grand total you will receive, and how much of that came from interest.

The Formula Explained

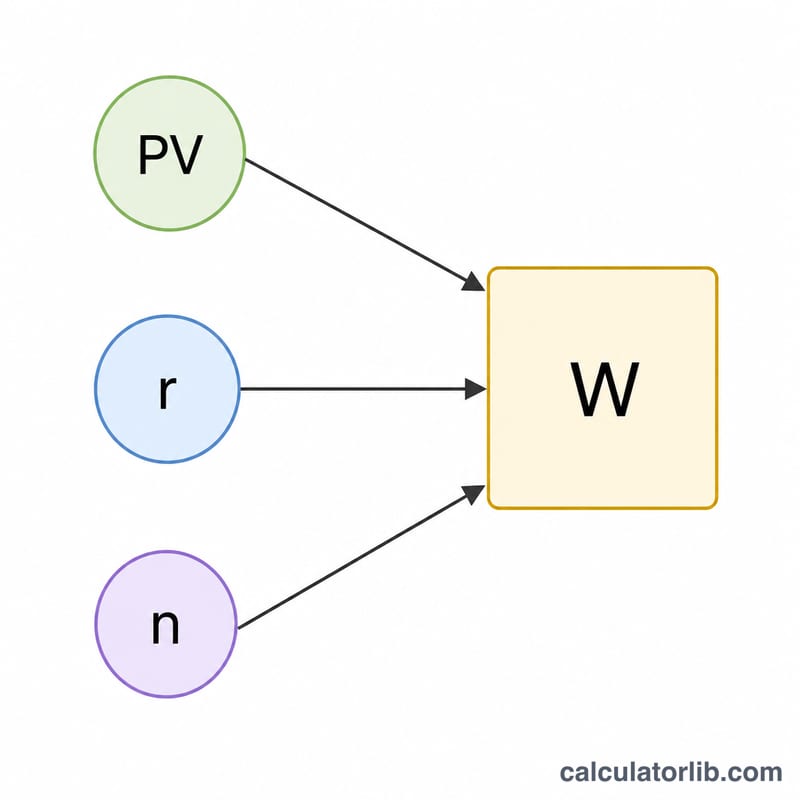

The core equation is the present-value annuity formula solved for the payment:

$$W = \frac{PV \cdot r}{1 - (1 + r)^{-n}}$$

Here PV is your starting balance, r is the periodic interest rate (annual rate divided by the number of periods per year), and n is the total number of withdrawals (years × periods per year). If the rate is zero, the formula simplifies to \(W = PV / n\).

Worked Example

Suppose you have $100,000 earning 5% annually and want monthly income for 10 years. The periodic rate is \(r = 0.05 / 12 = 0.0041667\) and \(n = 120\) withdrawals. Plugging in: $$W = \frac{100{,}000 \times 0.0041667}{1 - 1.0041667^{-120}} \approx \$1{,}060.66 \text{ per month}.$$ Over 120 months you receive about $127,279 — roughly $27,279 of which is interest.

FAQ

Does the balance run out exactly at the end? Yes — the formula is designed so the final withdrawal brings the balance to zero.

What if I want the savings to last forever? That is a perpetuity: you would only withdraw the interest each period (\(PV \times r\)) and never touch the principal.

Is this guaranteed? No. It assumes a constant interest rate. Real returns vary, so treat the result as a planning estimate, not a promise.