What the Savings Goal Calculator Does

This calculator works out how much you need to save each month to reach a specific financial target by a set date. Instead of guessing, you enter your goal and time frame, and the tool reverse-engineers the required monthly contribution while accounting for compound interest earned along the way. It's useful for planning a house deposit, an emergency fund, a holiday, or any dated savings goal.

The Inputs You Provide

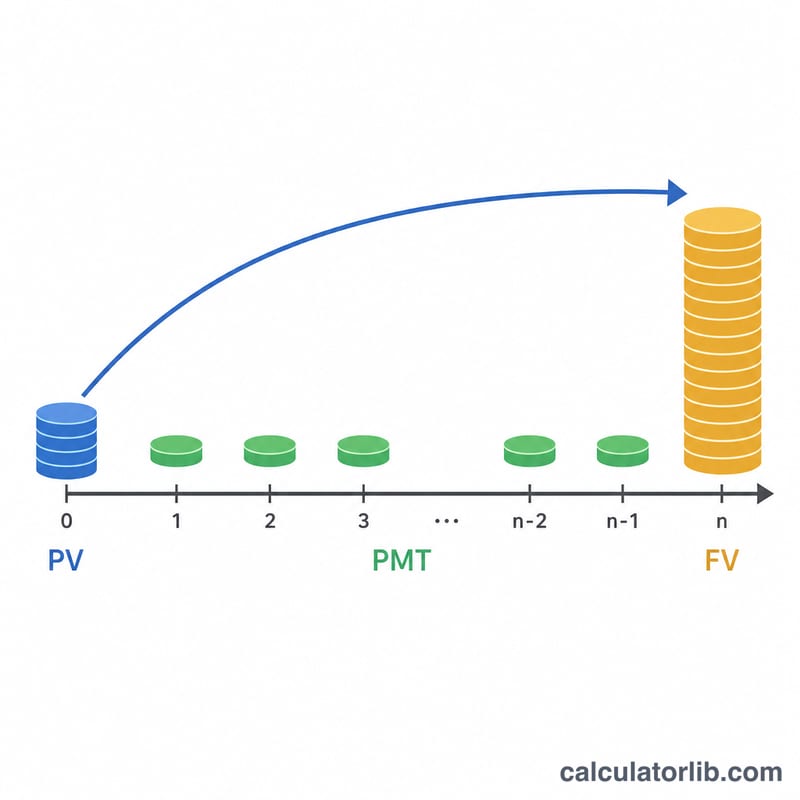

- Savings Goal Amount – the future value you want to reach.

- Initial Deposit – money you already have to start with (the present value), which grows with interest.

- Years to Grow – how long you have until you need the money.

- Annual Interest Rate (%) – the expected yearly return on your savings.

- Compound Frequency – how often interest is added: Annually, Semi-annually, Quarterly, Monthly, or Daily.

The Formula Explained

The calculator first finds the periodic rate r = (annual rate ÷ 100) ÷ frequency and the total number of compounding periods n × t = years × frequency. It then solves the future-value-of-an-annuity equation for the required payment:

PMT = (FV − PV × (1+r)n×t) × (r × frequency / 12) ÷ ((1+r)n×t − 1)

Here FV is your goal, PV your initial deposit, and (1+r)n×t is the growth factor. The r × frequency / 12 term converts the periodic payment into a monthly figure. If the interest rate is 0%, the tool simply divides the remaining amount by the number of months. It also reports total contributions (initial deposit + monthly payments × months) and the interest earned.

Worked Example

Suppose you want $20,000 in 5 years, start with a $2,000 deposit, earn 4% compounded monthly (frequency = 12). The periodic rate is 0.04 ÷ 12 ≈ 0.003333, and there are 60 periods. The growth factor (1.003333)60 ≈ 1.2210. Your deposit grows to about $2,442, leaving roughly $17,558 to fund. The formula returns a required monthly saving of about $265. Over 60 months you'd contribute around $15,900 plus your $2,000 deposit, with the rest coming from interest.

Frequently Asked Questions

Does the compound frequency really matter? Yes—more frequent compounding (e.g. daily) slightly increases interest earned, lowering the monthly amount you need to save.

What if the result is negative? A negative monthly payment means your initial deposit alone will already exceed the goal with interest, so no extra saving is required.

Is the interest rate guaranteed? No. The rate is an assumption. Use a conservative estimate for variable returns, and re-run the calculator if conditions change.