什麼是儲蓄提領計算機?

儲蓄提領計算機能告訴你,在選定的期間內,每一期(每月、每季或每年)可以從儲蓄帳戶或投資中固定領出多少錢,讓餘額在期末剛好歸零。由於尚未提領的餘額會持續滋生利息,因此你最終領回的總金額,通常會比一開始投入的本金還要多。這套計算方式,與退休金分期提領(drawdown)規劃和年金給付所採用的原理完全相同。

使用方法

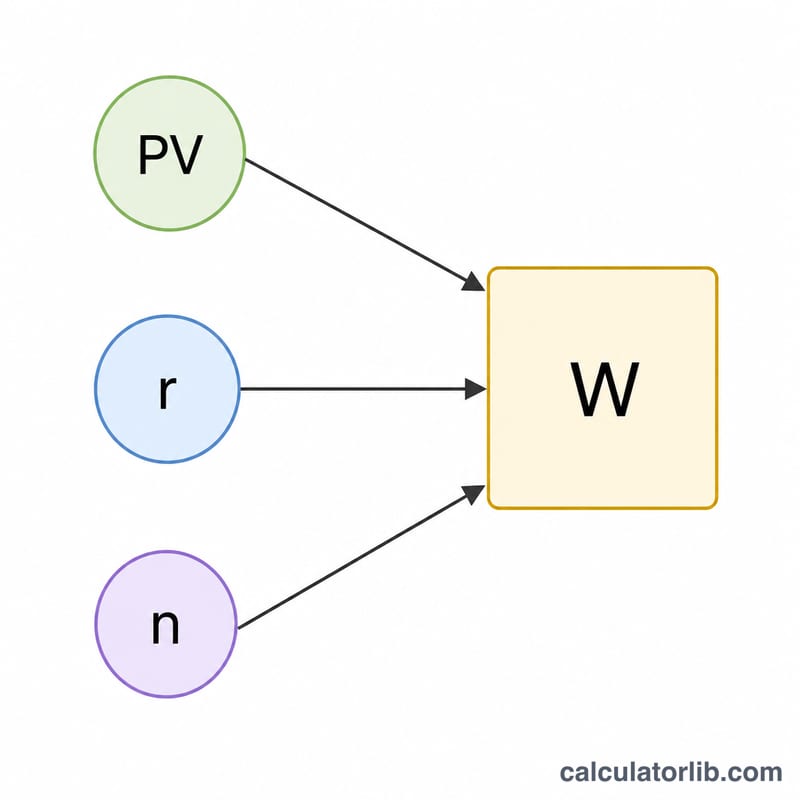

輸入目前的儲蓄餘額、帳戶的年利率、希望這筆錢能撐多少年,以及你打算多久提領一次。計算機會算出每期的固定提領金額、總提領次數、你最終可領回的總金額,以及其中有多少是來自利息。

公式說明

核心算式來自「現值年金公式」,並反解出每期的提領金額:

$$W = \frac{PV \cdot r}{1 - (1 + r)^{-n}}$$

其中 \(PV\) 是你的期初餘額,\(r\) 是每期利率(年利率除以每年的提領期數),\(n\) 則是總提領次數(年數 × 每年期數)。若利率為零,公式可簡化為 \(W = PV / n\)。

實例試算

假設你有 $100,000、年利率 5%,希望未來 10 年每月都能領一筆固定收入。每期利率為 \(r = 0.05 / 12 = 0.0041667\),總提領次數 \(n = 120\) 次。代入公式:$$W = \frac{100{,}000 \times 0.0041667}{1 - 1.0041667^{-120}} \approx 每月\ \$1{,}060.66$$120 個月累計下來,你大約可領回 $127,279,其中約有 $27,279 是利息。

常見問題

餘額真的會在期末剛好用完嗎?是的——這套公式的設計,就是讓最後一次提領後餘額正好歸零。

如果我希望這筆儲蓄永遠領不完呢?那就是「永續年金」的概念:你每期只領取利息(\(PV \times r\)),完全不動用本金。

這個結果有保證嗎?沒有。計算假設利率維持固定不變,但實際報酬會隨時間波動,因此請把結果當作規劃用的估算值,而非保證金額。