What Is a Mortgage Recast?

A mortgage recast (also called re-amortization) is when you make a large lump-sum payment toward your loan principal, and your lender re-calculates your monthly payment based on the reduced balance — while keeping your original interest rate and remaining term. Unlike refinancing, a recast keeps the same loan, requires no credit check or closing costs (usually just a small fee), and lowers your monthly payment immediately. This tool uses standard amortization math and applies to typical fixed-rate mortgages.

How to Use This Calculator

Enter your current loan balance, the lump-sum amount you plan to apply, your annual interest rate, and the number of months remaining on the loan. The calculator subtracts the lump sum from the balance, then re-amortizes the new principal over the same remaining term to show your new monthly payment, your monthly savings, and the total interest you'll pay over the rest of the loan.

The Formula Explained

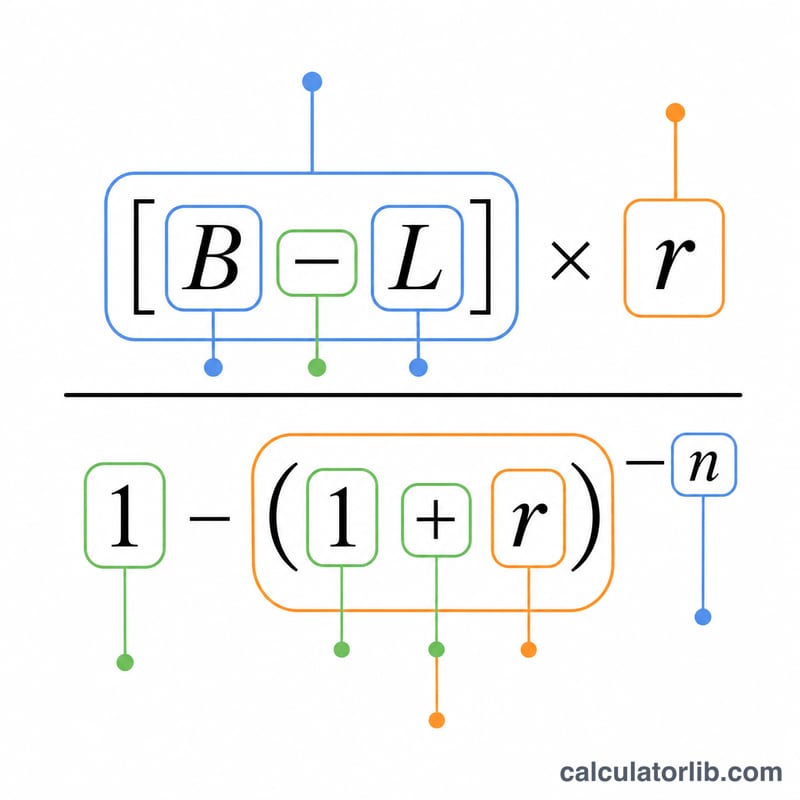

The new payment uses the standard amortization equation:

$$M_{\text{new}} = P \cdot \frac{r}{1-(1+r)^{-n}}$$Here \(B\) is the current balance, \(L\) is the lump sum, \(r\) is the monthly interest rate (annual rate \(\div 12 \div 100\)), and \(n\) is the number of remaining months. Because the term \(n\) stays the same, recasting reduces every payment rather than shortening the loan.

Worked Example

Suppose you owe $300,000 at 6% annual interest with 300 months remaining, and you pay a $50,000 lump sum. The monthly rate is \(r = 0.06 \div 12 = 0.005\). The new principal is $250,000. New payment $$= 250{,}000 \times \frac{0.005}{1 - 1.005^{-300}} \approx \mathbf{\$1{,}610.75}$$ down from about $1,932.90 — a monthly saving of roughly $322.

FAQ

Does recasting change my interest rate? No. A recast keeps your existing rate and term; only the balance and resulting payment change.

Is recasting better than refinancing? If you already have a good rate and want a lower payment without closing costs, recasting is often cheaper. Refinancing makes sense when you can secure a meaningfully lower rate.

Will a recast pay off my loan faster? No — it lowers the payment over the same term. To pay off faster, keep making your original payment after recasting.