What this calculator does

The debt snowball and debt avalanche are the two most popular strategies for paying off multiple debts faster. Both make the minimum payment on every debt and then throw all remaining money at one target debt. They differ only in which debt gets the extra payment first. This calculator simulates both, month by month, using the same total monthly budget, so you can see exactly how much time and interest each approach costs.

Snowball vs avalanche: the difference

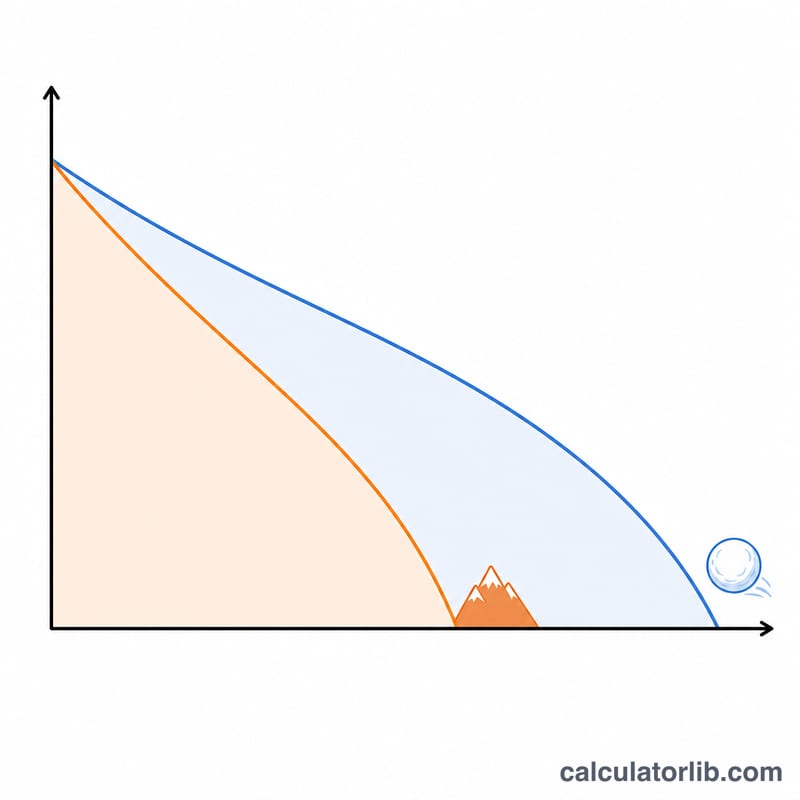

The avalanche method attacks the debt with the highest APR first. Because interest is the real enemy, this mathematically minimizes the total interest you pay and usually clears all debt in the fewest months. The snowball method attacks the smallest balance first. It costs a little more interest, but you eliminate whole accounts quickly, which gives a motivating psychological "win" early on.

$$\begin{gathered} \text{Each month: } b_i \mathrel{+}= b_i\cdot\frac{\text{APR}_i}{1200}, \quad \text{then apply } \text{Budget} \\[1.5em] \text{where}\quad \left\{ \begin{aligned} \text{Avalanche} &: \text{extra} \to \text{highest } \text{APR}\text{ first} \\ \text{Snowball} &: \text{extra} \to \text{smallest } \text{Balance}\text{ first} \\ \text{Saved} &= \text{Interest}_{\text{sno}} - \text{Interest}_{\text{ava}} \end{aligned} \right. \end{gathered}$$

How to use it

Enter your total monthly payment budget — this must be at least the sum of all minimum payments. Then enter each debt's balance, APR, and minimum payment (up to four debts; leave a balance at 0 to skip it). The calculator runs both simulations and shows months to debt-free and total interest for each, plus how much avalanche saves.

Worked example

Suppose you owe $2,000 at 22% (min $50) and $5,000 at 15% (min $100), with a $500 monthly budget. Avalanche targets the 22% card first; snowball also targets the $2,000 card first (it is both smaller and higher rate), so here the two strategies behave identically. When the smallest balance is not the highest rate, avalanche pulls ahead in interest saved.

FAQ

Which method is better? Avalanche is cheaper; snowball is more motivating. If you reliably stick to a plan, choose avalanche.

Why does the result show a huge number of months? Your budget is too small to outpace interest. Increase it above the sum of your minimum payments.

Does it assume fixed rates? Yes — APRs and minimums are held constant for the simulation, which is standard for planning estimates.