What Is an Interest-Only Payment?

An interest-only payment covers only the interest accruing on a loan, with none of the payment going toward reducing the principal balance. Interest-only loans and mortgages are common in early loan phases, bridge financing, and certain investment property structures. Because no principal is repaid, the loan balance stays the same and the payment is typically lower than a fully amortizing payment.

How to Use This Calculator

Enter your loan amount (the outstanding principal), the annual interest rate as a percentage, and how often you make payments. The calculator returns the amount due each payment period plus the total interest you would pay across a full year.

The Formula Explained

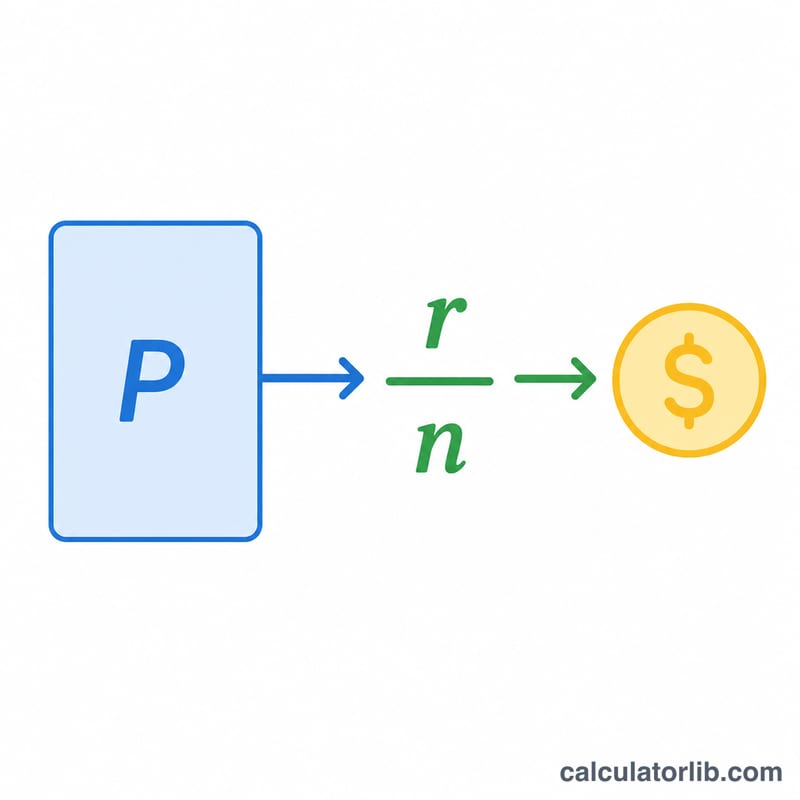

The interest-only payment is calculated as:

$$\text{Payment} = \text{Principal} \times \left( \text{annual rate} \div \text{payments per year} \right)$$

First the annual percentage rate is converted to a decimal (for example, 5% becomes \(0.05\)). It is then divided by the number of payments per year to get the periodic rate, and multiplied by the principal. Since principal never decreases, every interest-only payment is identical.

Worked Example

Suppose you borrow $200,000 at a 5% annual rate with monthly payments. The monthly periodic rate is \(0.05 \div 12 = 0.0041667\). Multiply by the principal: $$\$200{,}000 \times 0.0041667 = \$833.33 \text{ per month}.$$ Over a year you pay \(\$200{,}000 \times 0.05 = \$10{,}000\) in interest.

FAQ

Does an interest-only payment reduce my loan balance? No. You only pay the interest, so the principal stays the same until you start making principal payments or repay it as a lump sum.

Why is the interest-only payment lower than a normal payment? A fully amortizing payment includes both interest and principal repayment, so it is larger. Interest-only payments skip the principal portion.

What happens after the interest-only period ends? The loan typically converts to a fully amortizing schedule, often causing payments to rise significantly because the principal must now be repaid over the remaining term.