What Is an Interest-Only Mortgage?

An interest-only mortgage is a loan where, for a set period, you pay only the interest charged on the outstanding balance and none of the principal. Because the loan balance does not shrink, the monthly payment is lower than a fully amortizing loan—but you still owe the full principal at the end of the interest-only term. This calculator shows the recurring monthly payment and the total interest you pay per year.

How to Use This Calculator

Enter the loan amount (principal) and the annual interest rate as a percentage. The calculator divides the annual rate by 12 to find the monthly rate, then multiplies it by the principal to give your monthly interest-only payment. It also totals the interest you would pay over a full year.

The Formula Explained

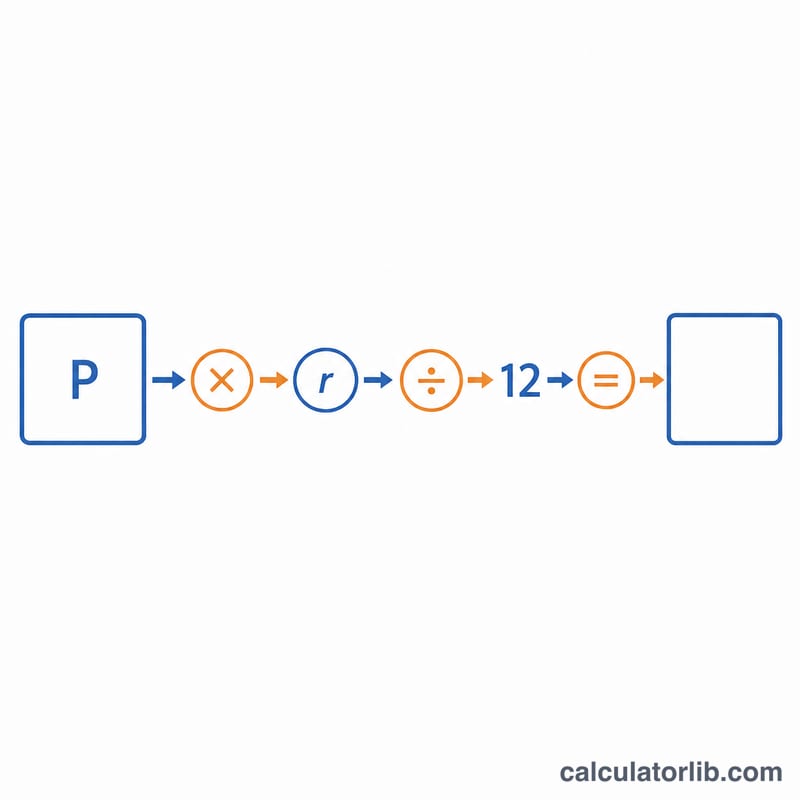

The core equation is $$\text{Payment} = P \times \frac{r}{12}$$, where \(P\) is the principal and \(r\) is the annual interest rate expressed as a decimal (for example, 6% = 0.06). Dividing \(r\) by 12 converts the annual rate into a monthly rate. Since no principal is repaid, the payment stays constant for the whole interest-only period.

Worked Example

Suppose you borrow $300,000 at a 6% annual rate. The monthly rate is \(0.06 / 12 = 0.005\). Your monthly payment is $$300{,}000 \times 0.005 = \$1{,}500.$$ Over one year that is \(\$1{,}500 \times 12 = \$18{,}000\) in interest, with the $300,000 balance still owed at the end.

FAQ

Does the loan balance go down? No. During the interest-only period the principal stays the same because you only pay interest.

Why are interest-only payments lower? They exclude principal repayment, so you only cover the financing cost—but you will need to repay or refinance the principal later.

Is this calculator country-specific? No. The math is universal; it applies to any currency or jurisdiction as long as the rate is a standard annual percentage.