What this calculator does

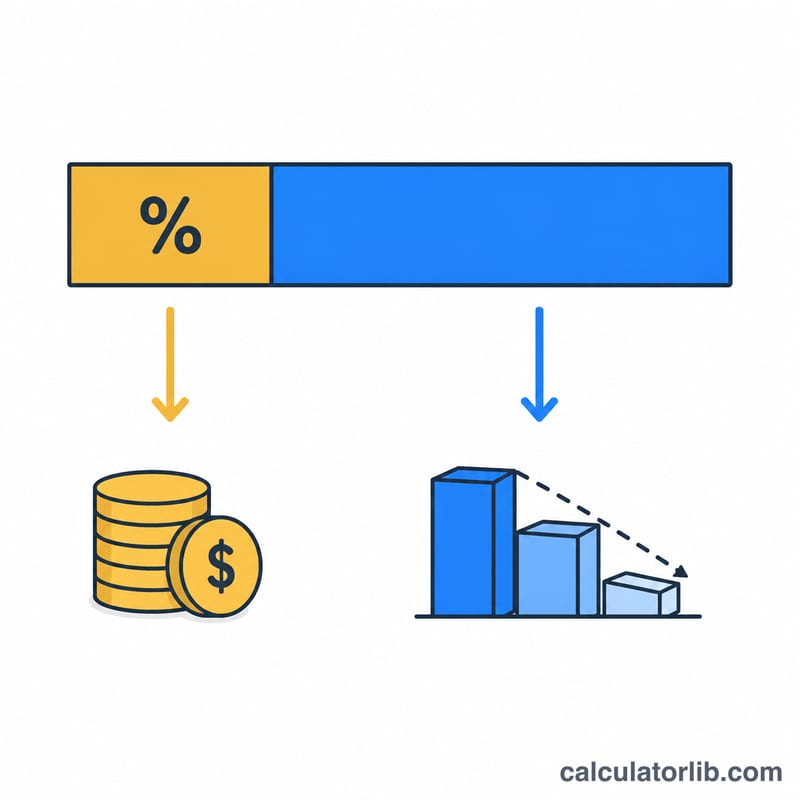

Every loan payment on an amortizing loan is split into two parts: interest (the cost of borrowing) and principal (the amount that actually reduces what you owe). This tool breaks down a single payment so you can see exactly where your money goes for the current period.

How to use it

Enter three numbers: your current loan balance, the annual interest rate as a percentage, and your monthly payment. The calculator returns the interest charged this month, the principal paid, the percentage split, and your balance after the payment clears.

The formula explained

Lenders charge interest on the outstanding balance for each period. For a monthly loan the periodic rate is the annual rate divided by 12 (and by 100 to convert from a percentage):

$$\text{Interest} = \text{Balance} \times \frac{\text{Rate}}{1200}$$

Whatever is left of your payment after covering interest pays down the balance:

$$\text{Principal} = \text{Payment} - \text{Interest}$$ and $$\text{New Balance} = \text{Balance} - \text{Principal}$$

Worked example

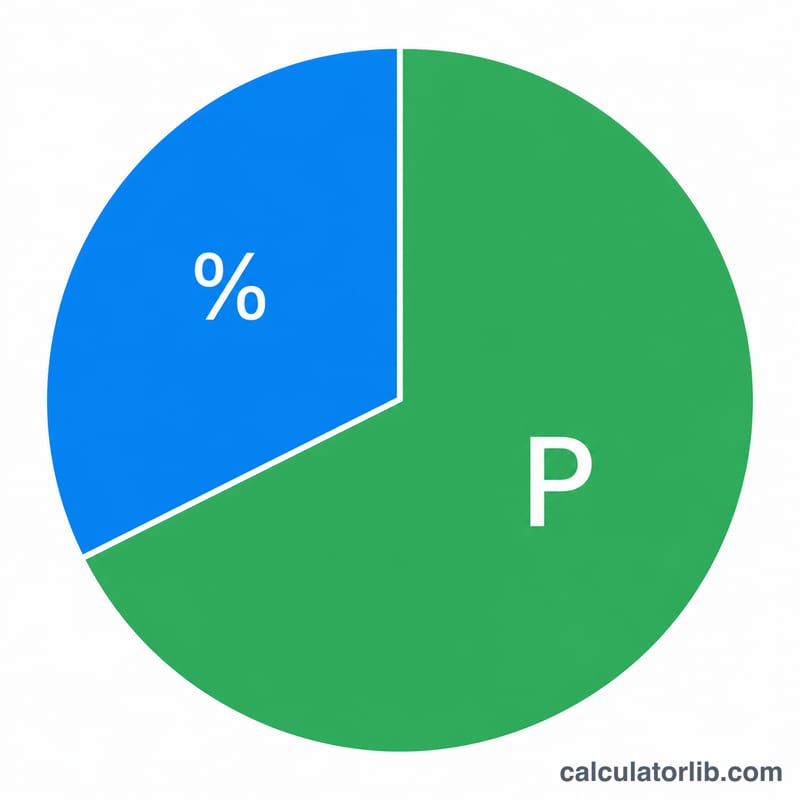

Suppose you owe $200,000 at 6% annual interest and pay $1,199.10 this month. The monthly rate is \(6 / 1200 = 0.005\). Interest \(= 200{,}000 \times 0.005 = \$1{,}000\). Principal \(= 1{,}199.10 - 1{,}000 = \$199.10\). So only about 17% of this early payment reduces your debt — the rest is interest. Your balance falls to $199,800.90.

FAQ

Why is so little going to principal? Early in a loan the balance is high, so interest dominates. As the balance shrinks, more of each fixed payment goes to principal.

What if my payment is less than the interest? The principal portion becomes negative, meaning your balance grows (negative amortization). Increase the payment to avoid this.

Does this work for any loan? Yes — mortgages, auto loans, and personal loans that charge interest monthly on the outstanding balance all follow this formula.