What this calculator does

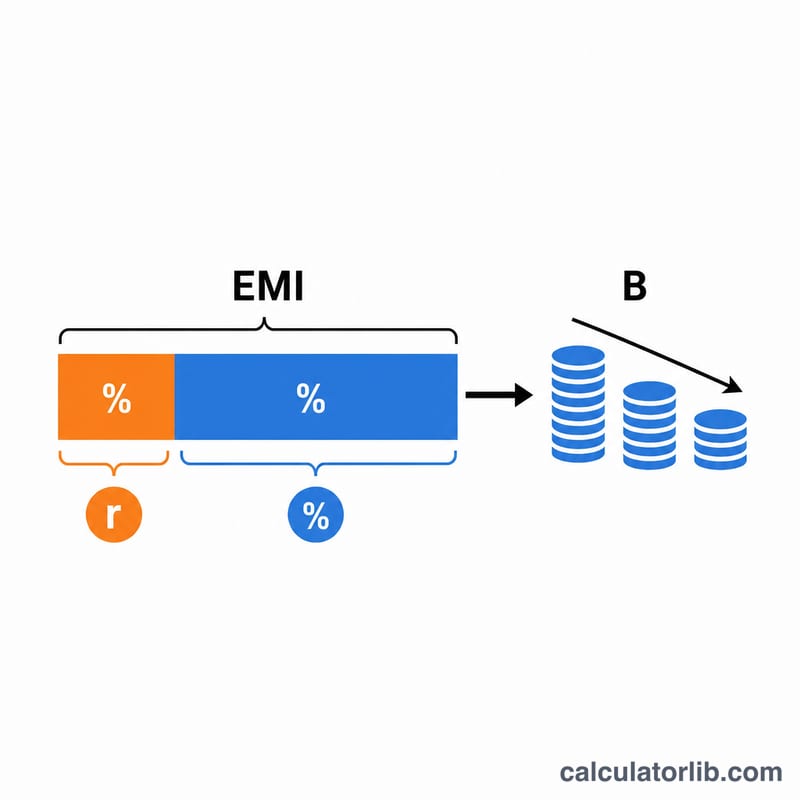

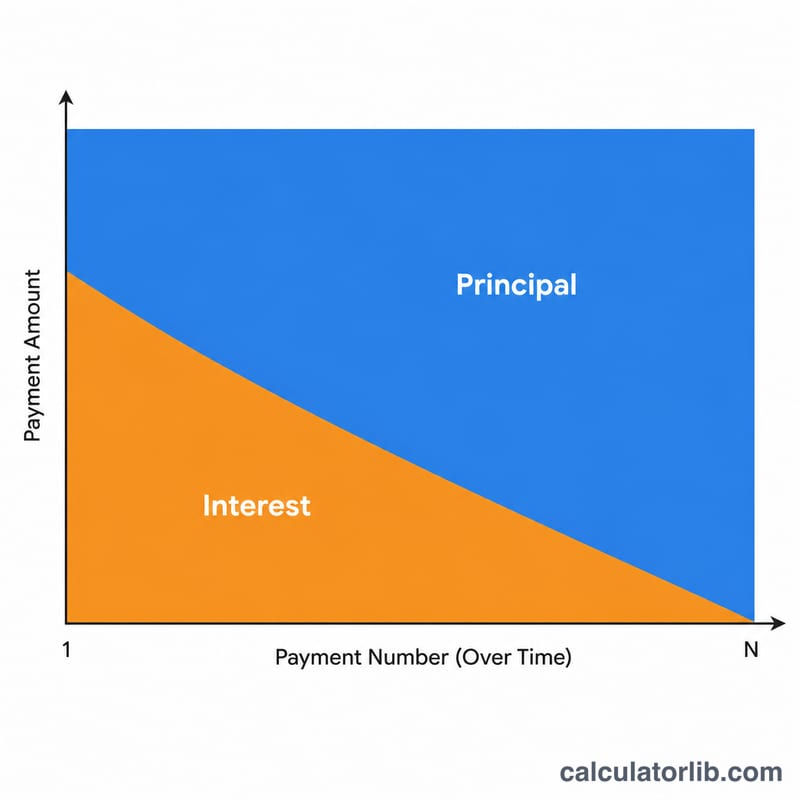

Every fixed-rate loan payment is split into two parts: interest (the lender's charge for the outstanding balance) and principal (the amount that actually reduces what you owe). Early in a loan most of each payment is interest; later, most goes to principal. This Principal vs Interest Breakdown Calculator shows the exact split for any single payment number on an amortizing loan such as a mortgage, car loan, or personal loan.

How to use it

Enter the original loan amount, the annual interest rate, the loan term in years, and the payment number you want to inspect. The calculator computes the level monthly payment (EMI), the outstanding balance just before that payment, and then splits the payment into principal and interest. It also shows the remaining balance after the payment is applied.

The formula explained

First the monthly payment is found with the standard amortization formula $$\text{EMI} = \frac{P\cdot r\cdot(1+r)^{n}}{(1+r)^{n}-1}$$ where \(r\) is the monthly rate (annual rate \(\div 12 \div 100\)) and \(n\) is the total number of payments. The balance just before payment \(k\) is $$B_{k-1} = P\cdot(1+r)^{k-1} - \text{EMI}\cdot\frac{(1+r)^{k-1}-1}{r}$$ Then $$\text{Interest}_k = B_{k-1}\times r \qquad \text{Principal}_k = \text{EMI} - \text{Interest}_k$$

Worked example

On a $200,000 loan at 6% annual for 30 years, the monthly payment is about $1,199.10. For payment #1 the balance before is the full $200,000, so interest = $$200{,}000 \times 0.005 = \$1{,}000.00$$ and principal = $$1{,}199.10 - 1{,}000.00 = \$199.10$$ The principal grows with every subsequent payment.

FAQ

Why is so much of my early payment interest? Interest is charged on the outstanding balance, which is highest at the start, so the interest slice is largest then.

Does this assume a fixed rate? Yes. It models a standard fully-amortizing fixed-rate loan with equal monthly payments.

What if my rate is 0%? With a 0% rate every payment is pure principal equal to the loan amount divided by the number of payments.