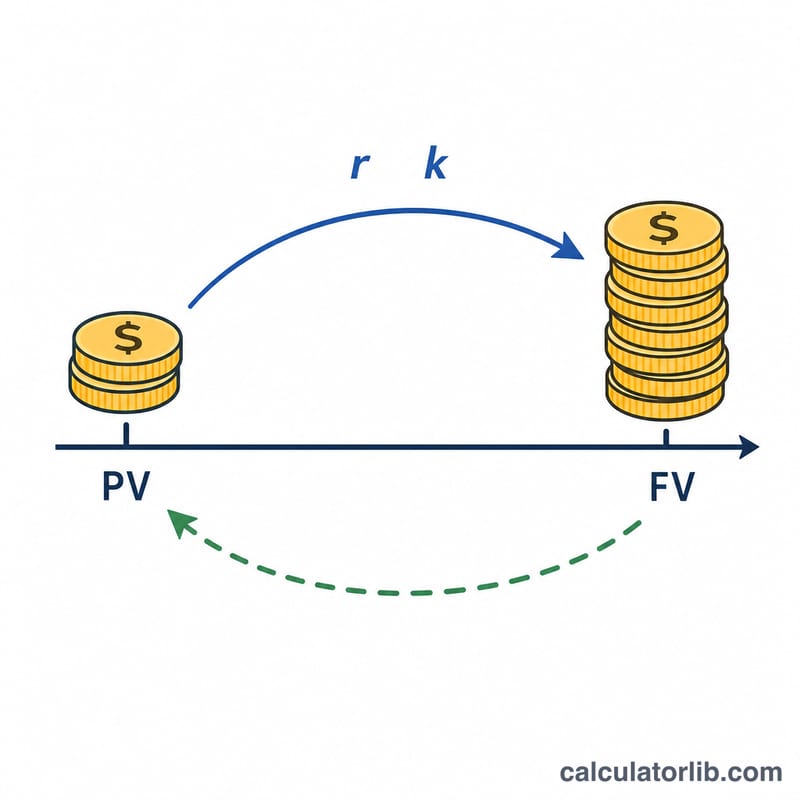

What this calculator does

This is a pure compound-interest finance tool that works the same in every country. Given a known future value (maturity total), an annual interest rate, a number of years, and how often interest compounds, it tells you the principal — the present value — you would need to invest today to reach that future amount. Because real banks apply their own rounding and fraction-handling rules, the result here is theoretical.

How to use it

Enter the future value you are targeting, the annual interest rate as a percent, and the number of elapsed years (decimals are allowed). Choose a rate type: Nominal rate uses periodic compounding driven by the compounding-frequency selector, while Effective rate treats the rate as an effective annual figure and ignores the frequency. Finally pick the compounding frequency — annually, semi-annually, quarterly, monthly, or daily — which only affects the nominal-rate mode.

The formula explained

For a nominal rate, the future value grows by a factor of \(1 + \frac{r}{k}\) once per compounding period, with \(n \times k\) periods total, so the present value is FV divided by that factor:

$$PV = \dfrac{FV}{\left(1 + \frac{r}{k}\right)^{n\,k}}$$Here \(r\) is the annual rate as a decimal (5% becomes 0.05) and \(k\) is the periods per year. For an effective annual rate \(R\), growth is simply \((1 + R)^n\), so

$$PV = \dfrac{FV}{(1 + R)^{n}}$$

Worked example

Suppose you want 120,000 in 10 years at a 5% nominal annual rate compounded annually (\(k = 1\)). The growth factor is \((1.05)^{10} = 1.628895\), so

$$PV = \frac{120{,}000}{1.628895} = \text{about } 73{,}669.27$$If interest compounded monthly instead (\(k = 12\)), the factor becomes \(\left(1 + \frac{0.05}{12}\right)^{120} = 1.647009\), giving PV of about 72,859.55 — slightly less, because more frequent compounding earns more.

FAQ

What is the difference between nominal and effective rate? A nominal rate is stated per year but applied per period (so the compounding frequency matters), while an effective rate already reflects compounding over a year and is applied once annually.

Can the rate be zero? Yes. With a 0% rate the growth factor is 1, so the principal equals the future value.

Why does more frequent compounding lower the principal? More compounding periods make money grow faster, so you need less up front to reach the same target.