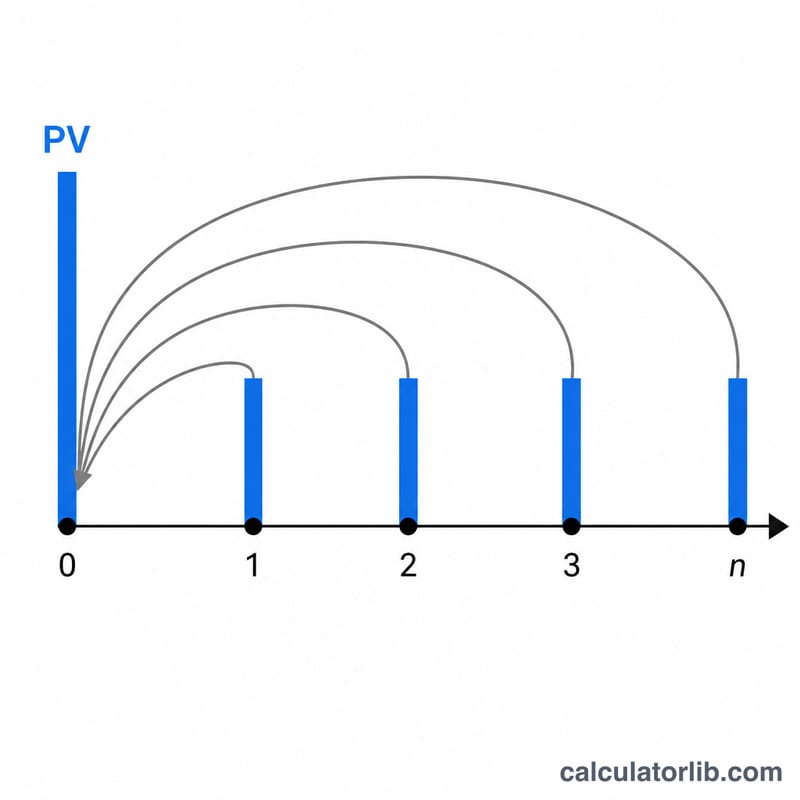

What is present value?

Present value (PV) is what a future amount of money is worth today, given a discount (interest) rate. Because a dollar received in the future is worth less than a dollar today, future cash flows are "discounted" back to the present. This calculator handles three common cases at once: a single future lump sum (FV), a stream of equal periodic payments (an annuity), and payments that continue forever (a perpetuity). It also supports growing payments and any compounding frequency.

How to use it

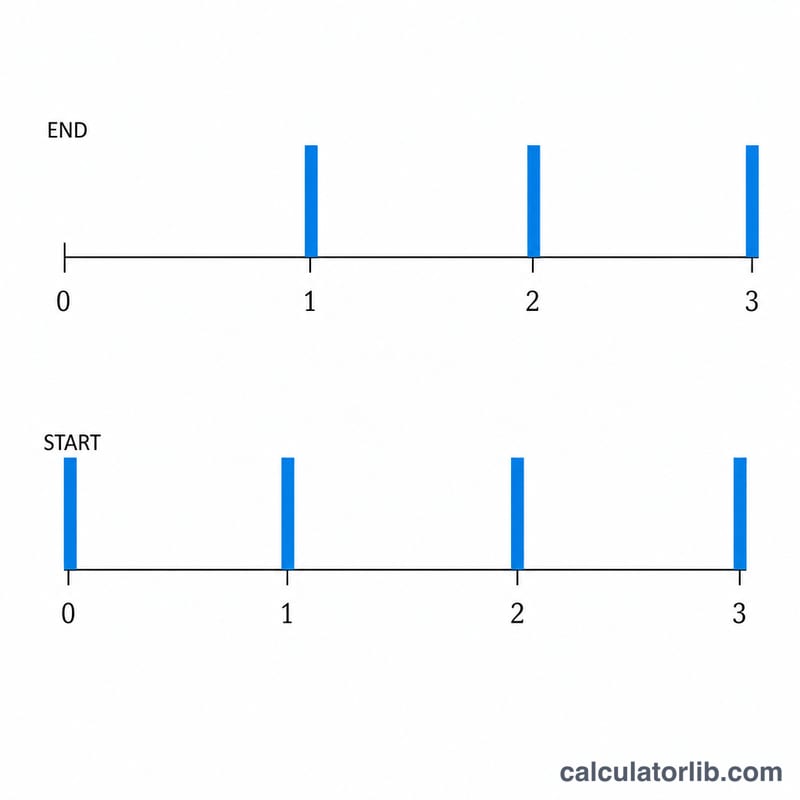

Enter the future lump sum (set it to 0 if you only want to value payments) and the payment per period (set to 0 if you only want a lump sum). Provide the annual interest rate, the number of years, the compounding frequency, and whether payments arrive at the end (ordinary annuity) or the beginning (annuity due) of each period. Use the growth rate for payments that increase each period, and tick "Perpetuity" for cash flows that never end.

The formula explained

The periodic rate is \(i = r / m\) and the number of periods is \(n = m \times t\). The lump-sum term is discounted as \(FV / (1+i)^n\). The annuity term is \((PMT / i) \times [1 - 1/(1+i)^n] \times (1 + iT)\), where the \((1 + iT)\) factor shifts ordinary payments (T=0) to annuity-due (T=1). The full present value is $$PV = \frac{FV}{(1+i)^n} + \frac{PMT}{i}\left[1 - \frac{1}{(1+i)^n}\right](1 + iT)$$ For a level perpetuity the annuity term simplifies to \(PMT / i\). When \(i = 0\) the present value of payments is simply \(PMT \times n\). For growing payments the annuity and perpetuity terms become $$PV_{ann} = \frac{PMT}{i-g}\left[1 - \left(\frac{1+g}{1+i}\right)^n\right](1+iT), \quad PV_{perp} = \frac{PMT}{i-g}(1+iT)$$

Worked example

FV = 1000, PMT = 100, r = 6%, t = 10 years, annual compounding, ordinary annuity, no growth. Then \(i = 0.06\) and \(n = 10\). Lump part: $$\frac{1000}{1.06^{10}} = 558.40$$ Annuity part: $$\frac{100}{0.06} \times \left[1 - \frac{1}{1.06^{10}}\right] = 1666.67 \times 0.441605 = 736.01$$ $$PV = 558.40 + 736.01 = \mathbf{1{,}294.40}$$

FAQ

Ordinary annuity vs annuity due? An ordinary annuity pays at the end of each period; an annuity due pays at the beginning, so its present value is higher by a factor of \((1 + i)\).

Why can a perpetuity be "not finite"? If the payment growth rate is greater than or equal to the discount rate, the series does not converge, so no finite present value exists.

What does compounding frequency change? More frequent compounding raises the effective discount applied per year, slightly lowering the present value for a given nominal annual rate.