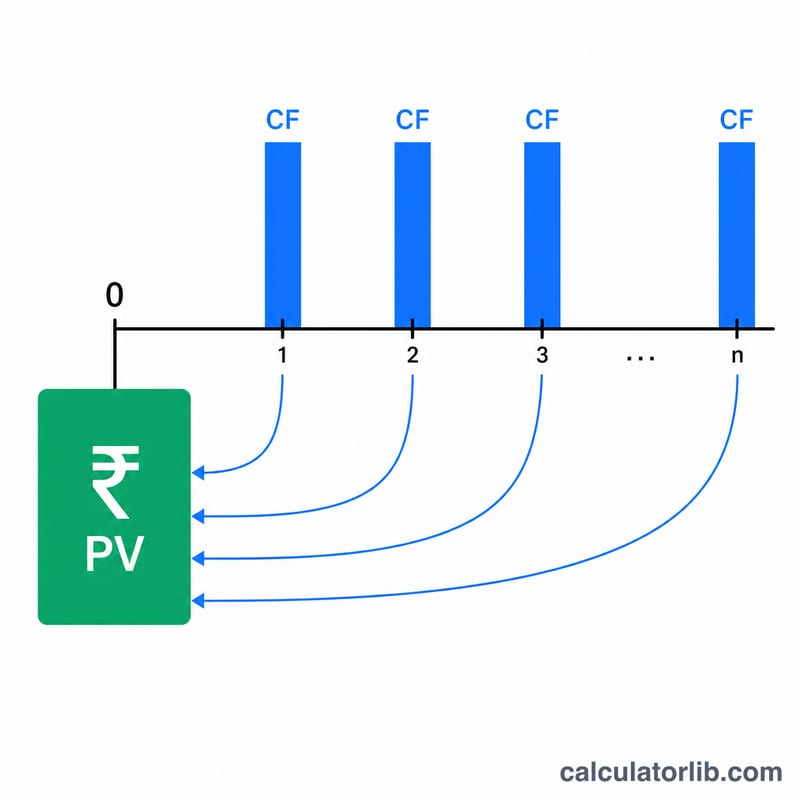

What Is the Present Value of a Pension?

The present value (PV) of a pension is the single lump-sum amount today that is financially equivalent to receiving a series of future annual pension payments. Because money available now can be invested and grow, a dollar received in the future is worth less than a dollar today. Discounting those future payments back to the present gives you a fair comparison value — useful when deciding between a lump-sum buyout and a lifetime annuity, or when valuing pension benefits in a divorce, estate, or retirement plan.

How to Use This Calculator

Enter three values: the annual pension payment you expect to receive, the discount rate (the annual rate of return you could otherwise earn, expressed as a percentage), and the number of years the payments will continue. The calculator returns the present value plus the total undiscounted payments for comparison.

The Formula Explained

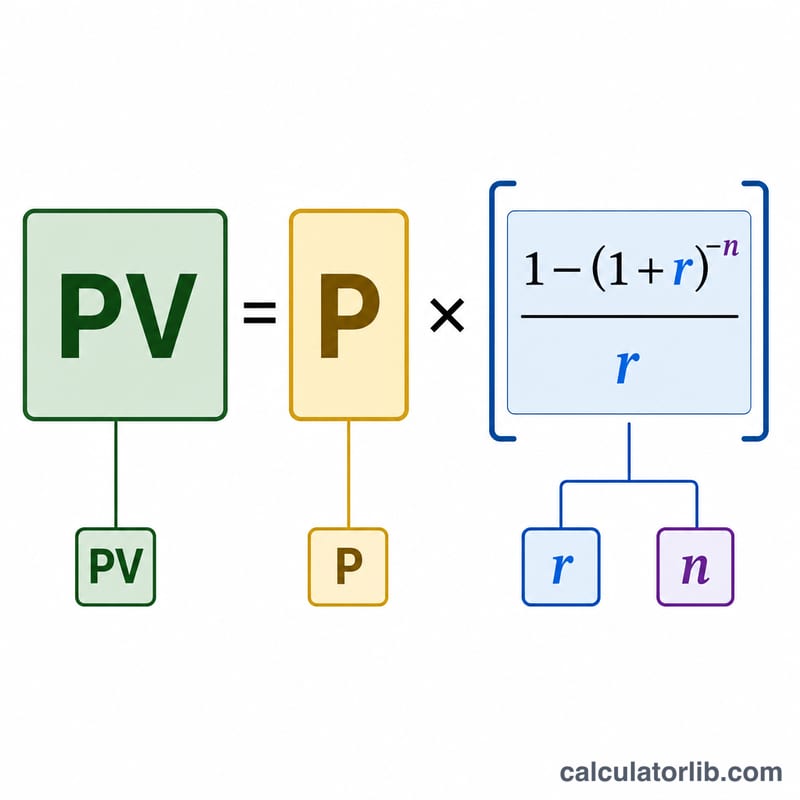

This tool uses the ordinary annuity present-value formula:

$$PV = P \times \frac{1 - \left(1 + r\right)^{-n}}{r}$$Here P is the annual payment, r is the decimal discount rate (5% = 0.05), and n is the number of years. The term \( \frac{1 - \left(1+r\right)^{-n}}{r} \) is the "annuity factor" — it sums the discount factors for every payment. If the rate is 0, the present value is simply \( P \times n \).

Worked Example

Suppose you will receive $30,000 per year for 20 years and your discount rate is 5%. Then \( r = 0.05 \) and \( (1.05)^{-20} \approx 0.376889 \). The annuity factor is \( \frac{1 - 0.376889}{0.05} \approx 12.46221 \). Multiplying: $$\$30{,}000 \times 12.46221 \approx \$373{,}866$$ So receiving $30,000 a year for 20 years is worth about $373,866 today, even though the total payments add up to $600,000.

FAQ

What discount rate should I use? Use a rate that reflects a realistic, low-to-moderate risk return you could earn — often a long-term bond yield or your expected investment return, commonly 3%–6%.

Does this account for inflation? Not directly. To get a real (inflation-adjusted) present value, use a real discount rate (nominal rate minus inflation).

Are payments assumed at year-end? Yes — this is an ordinary annuity with payments at the end of each year. Payments at the start of each period (annuity-due) would be slightly higher in value.