What is the Present Value Calculator?

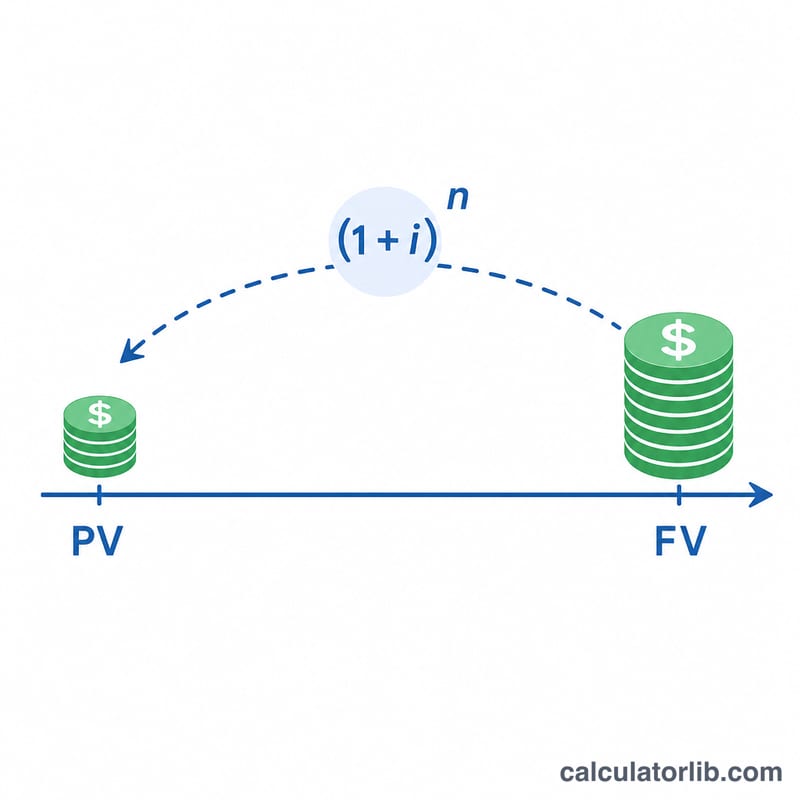

This calculator finds the present value (PV) of a single future amount of money — what a sum you will receive (or pay) in the future is worth in today's dollars. Because money available today can be invested and earn interest, a dollar received in the future is worth less than a dollar today. Discounting reverses compounding: it strips out the interest that would otherwise accrue, leaving the equivalent value now.

How to use it

Enter four values: the Number of Years until you receive the money, the annual Interest Rate as a percent, the Compounding frequency (Daily, Monthly, Quarterly or Yearly), and the Future Value (FV) in dollars. The tool returns the present value plus the Present Value Interest Factor (PVIF), the discount factor applied to one dollar.

The formula explained

Let m be the number of compounding periods per year (365, 12, 4 or 1). The per-period rate is \(i = (\text{rate}/100) / m\) and the total number of periods is \(n = \text{years} \times m\). Then $$PVIF = \frac{1}{(1 + i)^{n}}$$ and $$PV = FV \times PVIF.$$ The key principle is that the rate, the number of periods and the compounding frequency must all use the same time unit; this calculator handles that conversion internally.

Worked example

Suppose FV = $15,000 due in 3.5 years at 5.25% per year, compounded monthly. Then \(m = 12\), \(i = 0.0525 / 12 = 0.004375\) and \(n = 3.5 \times 12 = 42\). So $$(1.004375)^{42} \approx 1.201236,$$ giving \(PVIF = 0.832477\) and $$PV = 15{,}000 \times 0.832477 \approx \mathbf{\$12{,}487.16}.$$

Key Terms Explained

- Present Value (PV)

- The value today of a sum of money to be received or paid at a future date, after "discounting" it for the time value of money. It answers the question: how much is a future amount worth right now?

- Future Value (FV)

- The known cash amount expected at a specific point in the future. In this calculator FV is the input you are discounting back to the present.

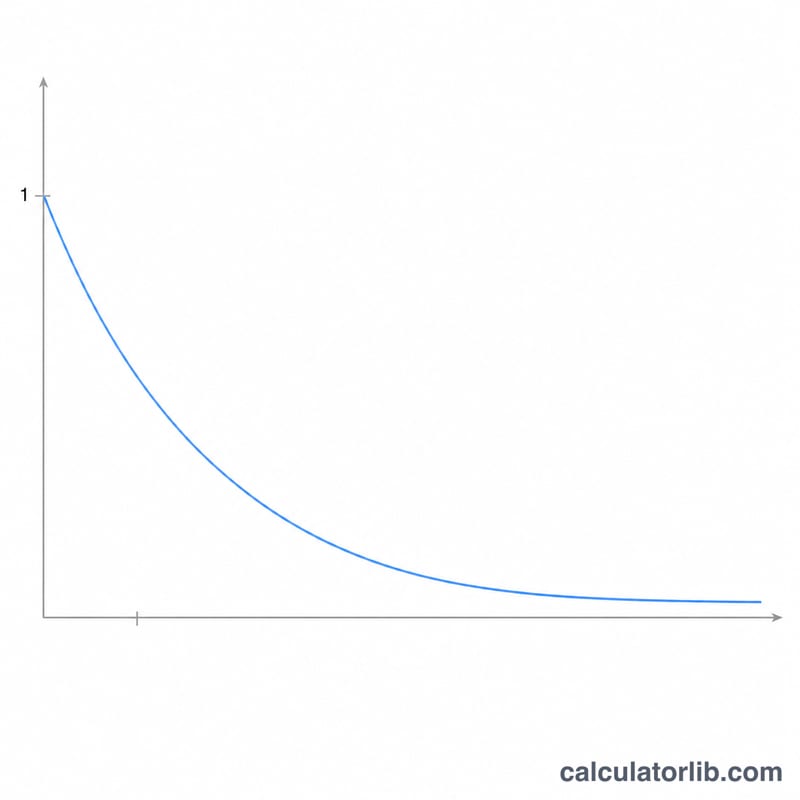

- Present Value Interest Factor (PVIF)

- The discount multiplier \((1 + i)^{-n}\) applied to a future amount. Multiply FV by the PVIF to obtain PV. Its value always lies between 0 and 1 for positive rates and periods.

- Discount Rate

- The annual rate of return used to translate future dollars into present dollars. It typically reflects the opportunity cost of capital, an expected investment return, or a required rate of return for the risk involved.

- Compounding Frequency (m)

- How many times per year interest is applied: yearly (1), quarterly (4), monthly (12) or daily (365). More frequent compounding produces a slightly smaller present value for the same annual rate.

- Per-period Rate (i)

- The rate applied each compounding period, equal to the annual rate divided by the frequency: \(i = \frac{\text{annual rate}}{m}\). For example, an 8% annual rate compounded monthly gives \(i = 0.08 / 12 \approx 0.6667\%\) per month.

- Number of Periods (n)

- The total count of compounding periods over the time horizon, equal to years multiplied by frequency: \(n = \text{years} \times m\). Three years of quarterly compounding is \(n = 12\) periods.

- Discounting

- The process of reducing a future amount to its present value, the reverse of compounding. Where compounding grows money forward in time by multiplying by \((1 + i)^{n}\), discounting moves it backward by dividing by \((1 + i)^{n}\).

FAQ

What happens if the rate is 0%? With no interest there is nothing to discount, so \(PVIF = 1\) and \(PV = FV\).

Does compounding frequency matter? Yes. For the same annual rate, more frequent compounding produces a slightly larger discount factor denominator, so PV falls modestly as you move from yearly toward daily compounding.

Can FV be negative? Yes — a future cost or liability can be entered as a negative number, and the present value will carry the same sign.