What Is the Present Value of an Annuity?

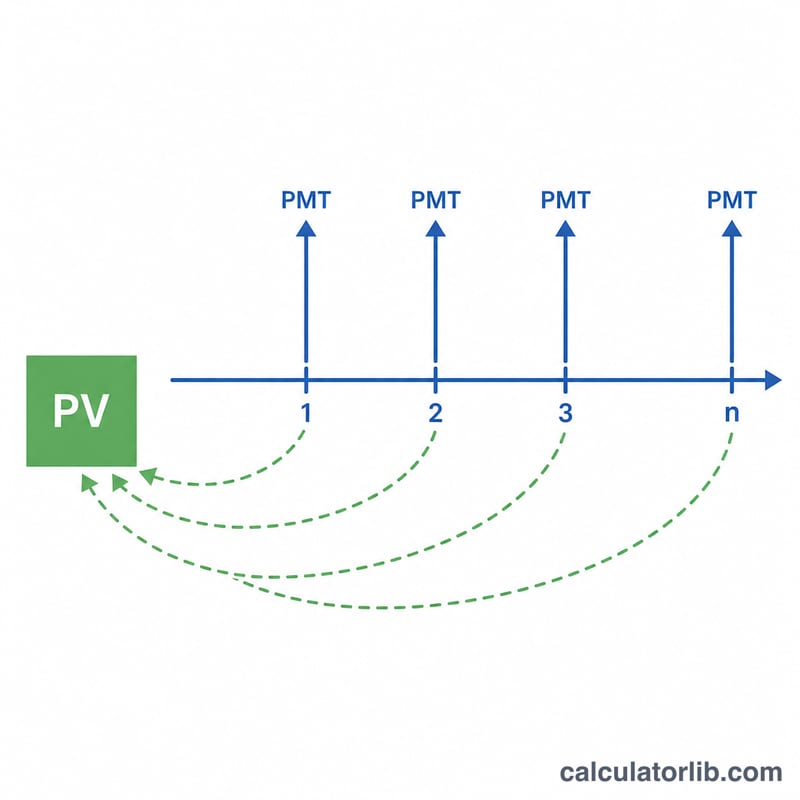

An annuity is a series of equal payments made at regular intervals. The present value (PV) of an annuity is what that whole stream of future payments is worth today, after discounting each payment for the time value of money. A dollar received in the future is worth less than a dollar today, so future payments are "shrunk" by the periodic interest (discount) rate. This calculator assumes an ordinary annuity, where payments occur at the end of each period.

How to Use This Calculator

Enter three values: the payment per period (PMT), the interest rate per period as a percentage, and the number of periods (n). Make sure the rate and the period count use the same time unit — if payments are monthly, use the monthly rate and the total number of months. The result shows the present value plus the total amount paid over the life of the annuity and the difference between them, which represents the time-value discount.

The Formula Explained

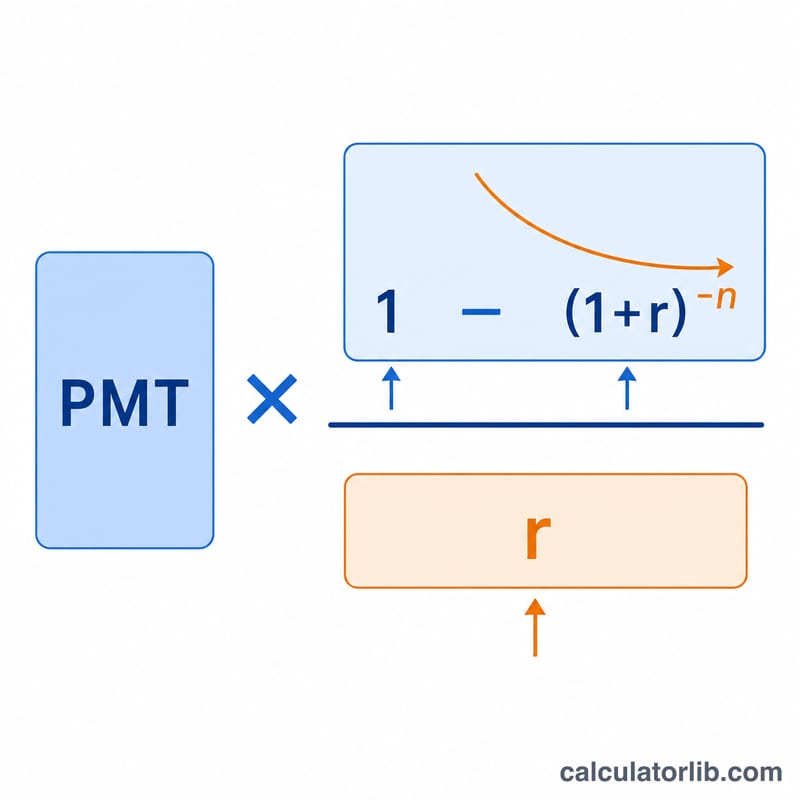

The core formula is:

$$PV = \text{PMT} \cdot \frac{1 - \left(1 + r\right)^{-\text{n}}}{r} \qquad r = \frac{\text{Rate (\%)}}{100}$$

Here \(r\) is the periodic rate written as a decimal (5% becomes 0.05). The term \((1 + r)^{-n}\) discounts the final payment back to today, and the full fraction is the "annuity factor" that bundles every discounted payment into a single multiplier. If \(r\) is 0, the formula reduces to \(PV = \text{PMT} \times n\).

Worked Example

Suppose you will receive $1,000 at the end of each year for 10 years, and the discount rate is 5% per year. Then \(r = 0.05\) and \(n = 10\). The annuity factor is $$\frac{1 - 1.05^{-10}}{0.05} \approx 7.7217.$$ Multiplying by $1,000 gives a present value of about $7,721.73. Although you receive $10,000 in total, it is worth only $7,721.73 today.

FAQ

Ordinary annuity vs. annuity due? This tool uses an ordinary annuity (payments at period end). An annuity due (payments at the start) is worth \((1 + r)\) times more.

What rate should I use? Use the periodic rate that matches your payment frequency — divide an annual rate by 12 for monthly payments.

Why is PV less than total payments? Because future money is discounted; the gap is the cost of waiting, shown as "Interest" in the results.