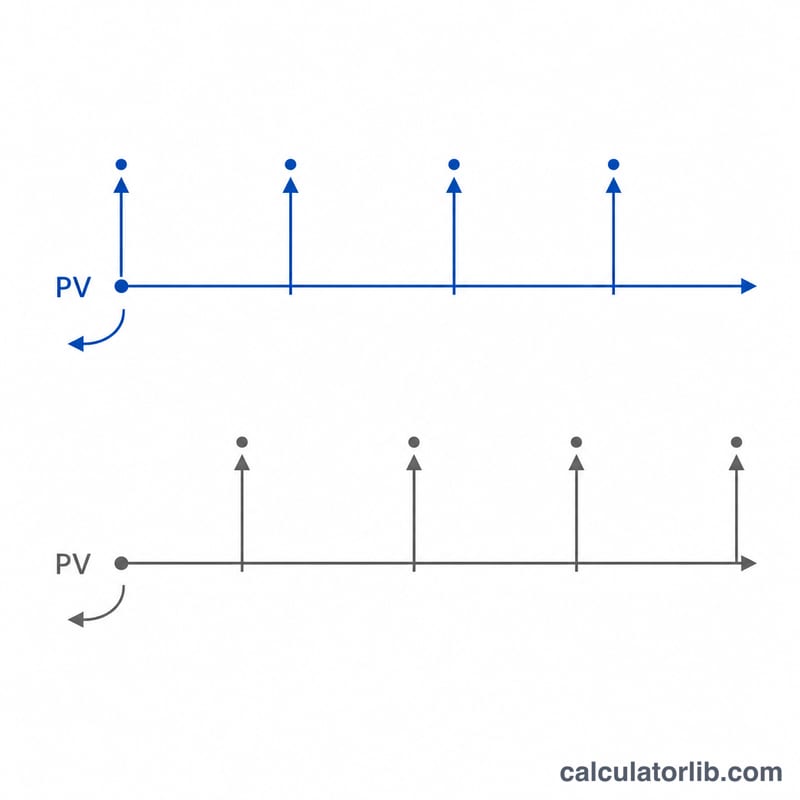

What Is the Present Value of an Annuity Due?

An annuity due is a series of equal payments made at the beginning of each period — think rent, leases, or insurance premiums paid in advance. The present value (PV) tells you how much that future stream of payments is worth in today's money, given a discount or interest rate. Because each payment arrives one period earlier than in an ordinary annuity, the present value is slightly higher.

How to Use This Calculator

Enter the periodic payment amount (PMT), the interest rate per period as a percentage, and the total number of periods. The calculator returns the present value, the total of all payments, and how much of that total is "discount" (the time value of money you save by valuing it today).

The Formula Explained

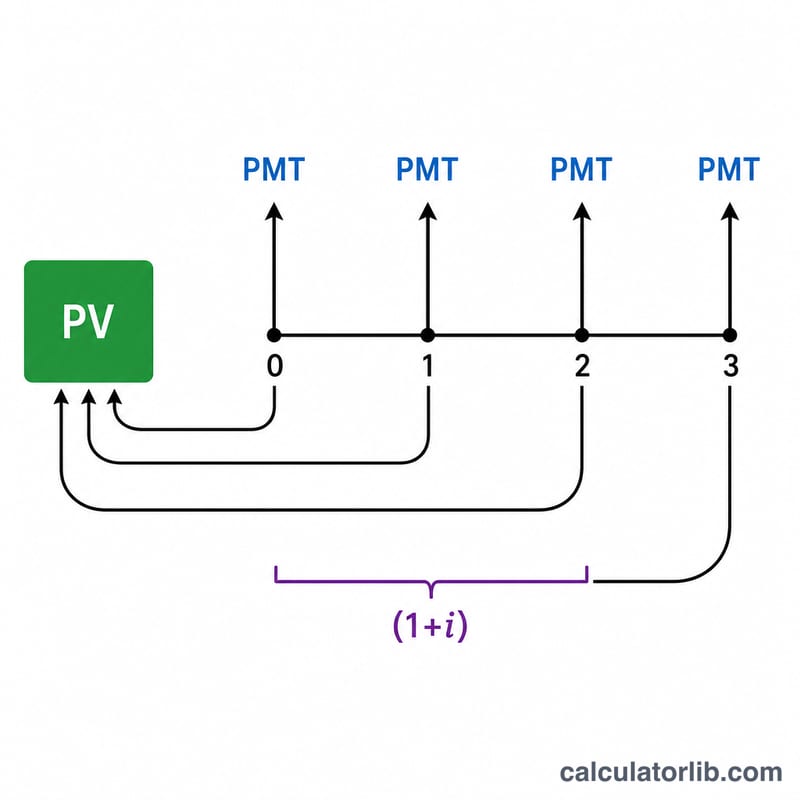

The present value of an annuity due is the ordinary-annuity formula multiplied by \((1+i)\):

$$PV = PMT \times \frac{1 - (1 + i)^{-n}}{i} \times (1 + i)$$where \(PMT\) = payment per period, \(i\) = interest rate per period in decimal form, and \(n\) = number of periods. When \(i = 0\) the present value is simply \(PMT \times n\).

Worked Example

Suppose you receive 1,000 at the start of each year for 10 years and the rate is 5% per period:

$$PV = 1000 \times \frac{1 - (1.05)^{-10}}{0.05} \times 1.05$$$$PV = 1000 \times 7.72173 \times 1.05 \approx 8{,}107.82$$So the stream is worth about 8,107.82 today.

FAQ

How is an annuity due different from an ordinary annuity? Payments occur at the start of each period instead of the end, so the present value is multiplied by an extra \((1+i)\).

What rate should I use? Use the interest or discount rate that matches the payment frequency — a monthly annuity needs a monthly rate.

Why is the present value less than the total paid? Money received later is worth less today; the difference is the time value of money.