What is the annuity present value factor?

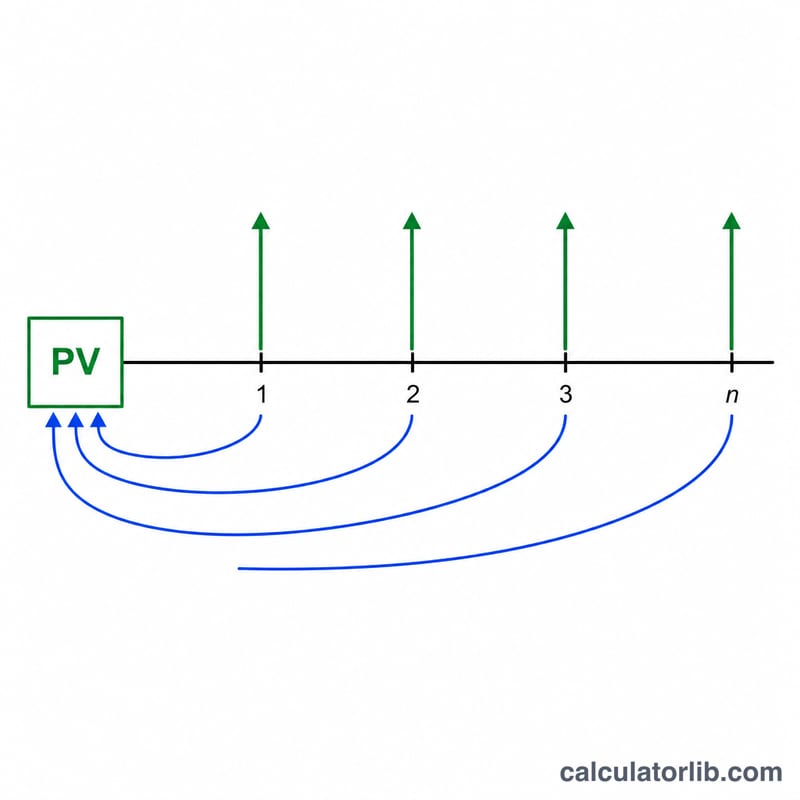

The annuity present value factor (sometimes written PVIFA) converts a stream of equal annual payments into a single present-value amount. It answers two practical questions: how large a loan can be repaid with a fixed annual payment, and how big a lump sum is needed today to fund a fixed annual pension. This is a universal time-value-of-money formula and is not specific to any country, though it is widely used in financial planning.

How to use it

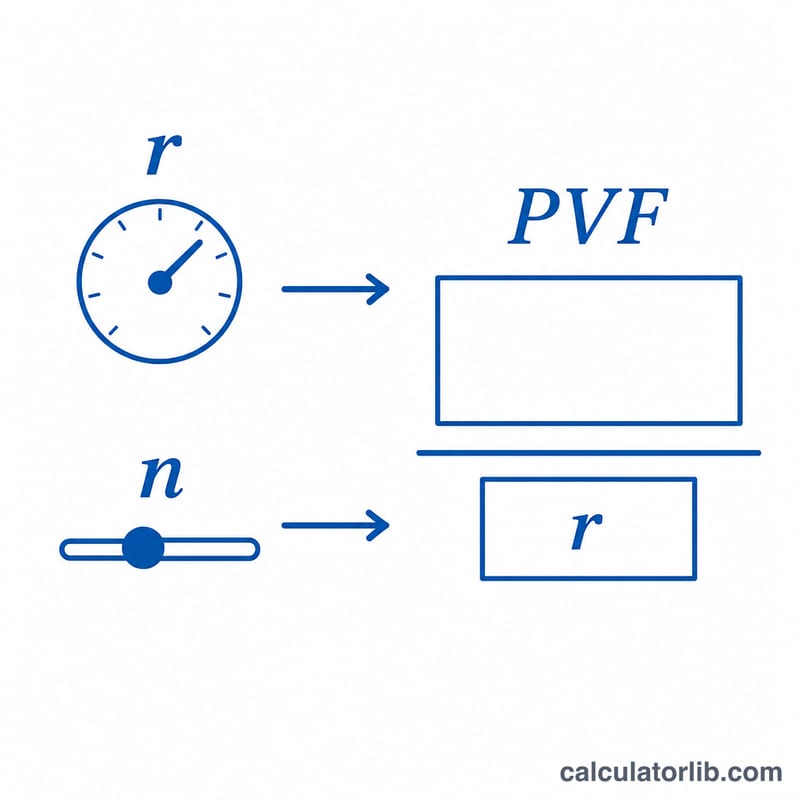

Enter the annual payment or pension amount (PMT), the annual interest rate as a percentage, and the number of years (the count of annual payments). Choose how many decimal places to display and the rounding mode. The calculator returns the factor and the present value, where present value = payment × factor.

The formula explained

The factor is $$PVF = \frac{1 - (1 + r)^{-n}}{r}$$ where \(r\) is the rate written as a decimal (so 3% becomes 0.03) and \(n\) is the number of years. Each future payment is discounted back to today and summed. When the rate is exactly 0%, division by zero is avoided and the factor simply equals \(n\), since there is no discounting.

Worked example

For PMT = 1, rate = 3%, and n = 20: \(r = 0.03\), and \(1.03^{-20} \approx 0.553676\). Then $$PVF = \frac{1 - 0.553676}{0.03} \approx 14.877.$$ The present value is \(1 \times 14.877 = 14.877\). So receiving (or repaying) 1 unit per year for 20 years at 3% is worth about 14.877 units today.

Interpreting Your Result

The annuity present value factor tells you how many years' worth of a single annual payment that stream is worth in today's dollars. A factor of 12.46, for instance, means a series of equal annual payments is worth about 12.46 times one payment right now — far less than the simple sum of all the payments, because money received in future years is discounted back to the present.

Two inputs move the factor in opposite directions:

- Higher interest (discount) rate → lower factor. A higher rate means future dollars are worth less today, so each payment shrinks more the further out it falls.

- Longer term → higher factor, but with diminishing returns. Each additional year adds less than the one before, because distant payments are discounted heavily. At high rates the factor approaches a ceiling of \(1/r\) (a perpetuity); for example at 10% it never exceeds 10.

The same factor answers two practical questions depending on which way you read it:

- Maximum loan size: if you can afford a fixed annual payment, multiplying it by the factor gives the largest loan principal that payment can support at that rate and term.

- Lump sum needed for a pension or income stream: if you want to receive a fixed payment each year, multiplying it by the factor gives the lump sum you would need today (at the assumed rate) to fund that stream.

This table and tool use the ordinary annuity convention (payments at the end of each period). If payments occur at the start of each period (an annuity due), multiply the factor by \((1+r)\), which raises the present value. Make sure the rate you enter matches the payment frequency and reflects the discount rate appropriate to the cash flow's risk.

This is general educational information, not personal financial advice. The factor reflects only the rate and term you enter; consult a qualified professional before making borrowing, pension, or investment decisions.

FAQ

Is this an ordinary annuity or an annuity due? This uses the ordinary annuity (end-of-period) form. An annuity due (payments at period start) multiplies the result by \((1 + r)\).

What happens at 0% interest? The factor equals the number of years \(n\), because nothing is discounted.

Can the rate be negative? The formula is defined for any \(r\) greater than -1 (i.e. -100%). Results are informational; actual rounding and fraction handling can differ by financial institution.