What is the Capital Recovery Factor?

The capital recovery factor (CRF) is a standard time-value-of-money ratio that converts a present lump sum into a stream of equal annual payments. Multiply a present value (a loan principal or an annuity fund) by the CRF and you get the constant amount that must be paid each year to fully amortize that sum over the chosen term at the chosen interest rate. This is a universal financial formula and applies in any currency — just enter the principal in whatever monetary unit you use, and the payment comes back in the same unit.

How to use this calculator

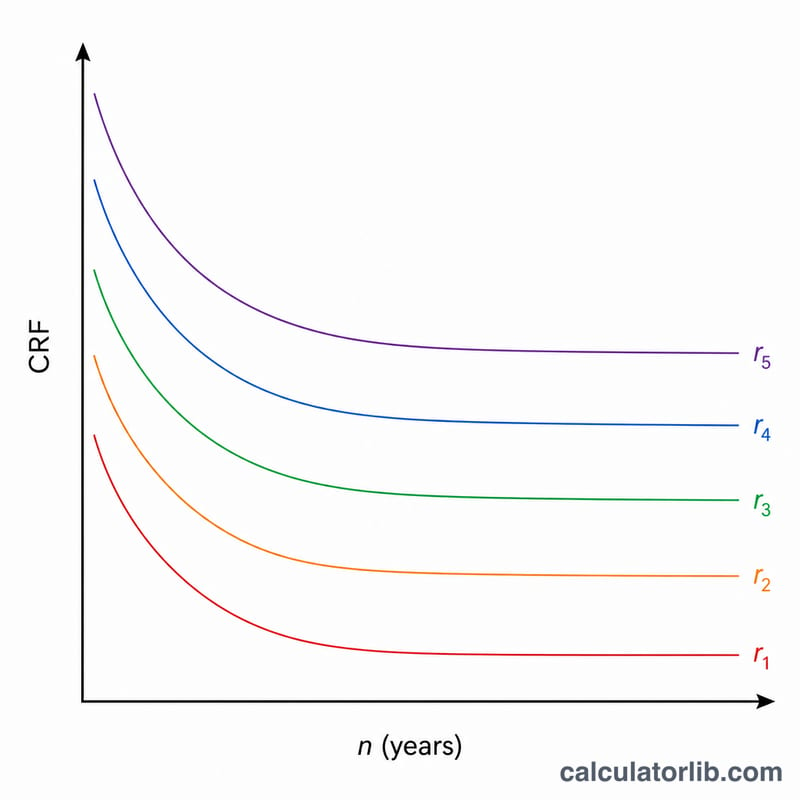

Enter the principal (present value), the annual interest rate as a percent, and the number of years. Choose how many decimal places to keep and the rounding rule (truncate, round half up, or ceiling). The tool returns the CRF, the equal annual payment, and a year-by-year table showing how the CRF shrinks as the term lengthens at the same rate.

The formula explained

With \(r\) as the decimal annual rate and \(n\) the number of years, $$\text{CRF} = \frac{r}{1-(1+r)^{-n}}$$ and the annual payment is $$\text{PMT} = \text{PV} \times \text{CRF}.$$ When the rate is exactly zero the expression becomes \(0/0\), so the calculator uses the mathematical limit \(\text{CRF} = 1/n\), meaning you simply repay the principal in equal slices.

Worked example

Take a present value of 1 unit at a 3% annual rate over 20 years. Here \(1.03^{20} \approx 1.806111\), so \(1.03^{-20} \approx 0.553676\) and \(1 - 0.553676 = 0.446324\). Then $$\text{CRF} = \frac{0.03}{0.446324} \approx 0.067216,$$ which rounds to \(0.067\) at three decimals. The annual payment is \(1 \times 0.067216 \approx 0.067\) per year.

FAQ

What happens at 0% interest? The CRF equals \(1/n\), so a 100-unit principal over 10 years gives a payment of 10 per year — pure principal repayment.

Is the CRF the same as a mortgage payment factor? Yes for annual compounding. For monthly payments you would use a monthly rate and a count of months instead.

Are the results exact? Rounding and fraction-handling rules differ between financial institutions, so treat these figures as reference values.