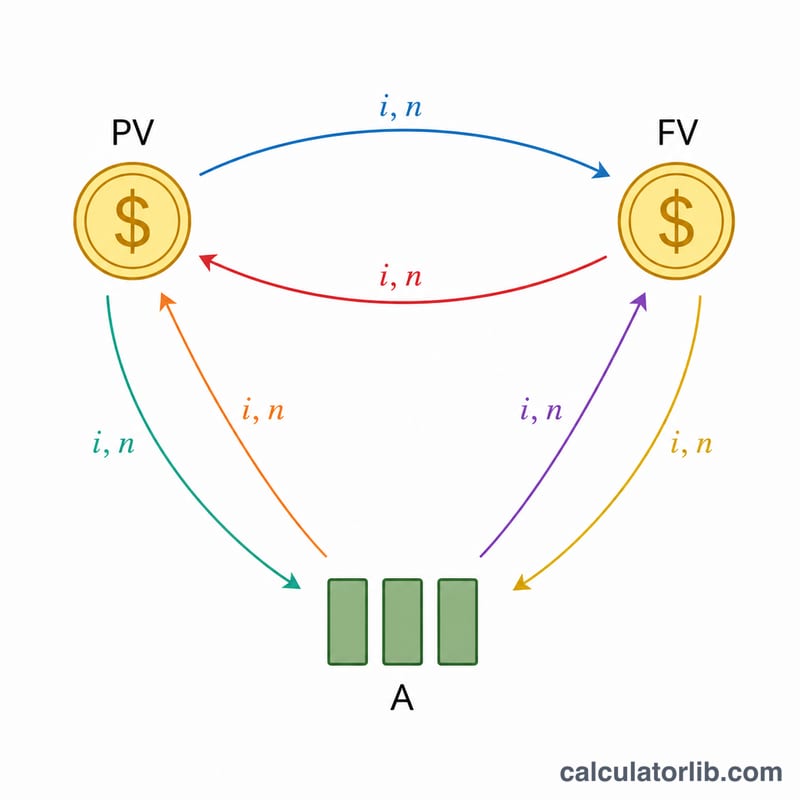

What it is

The Six Coefficients of Asset Management are the standard time-value-of-money (TVM) factors used in savings, loan, and annuity (pension) planning. They are famous in Japan's FP (Financial Planner) certification exam as the "six coefficients", but the underlying mathematics is universal and applies anywhere. This tool computes all six at once for a given annual interest rate and number of years, so you can read a lump sum into a future value, a future target into a required deposit, a loan principal into a periodic payment, and so on.

The six factors

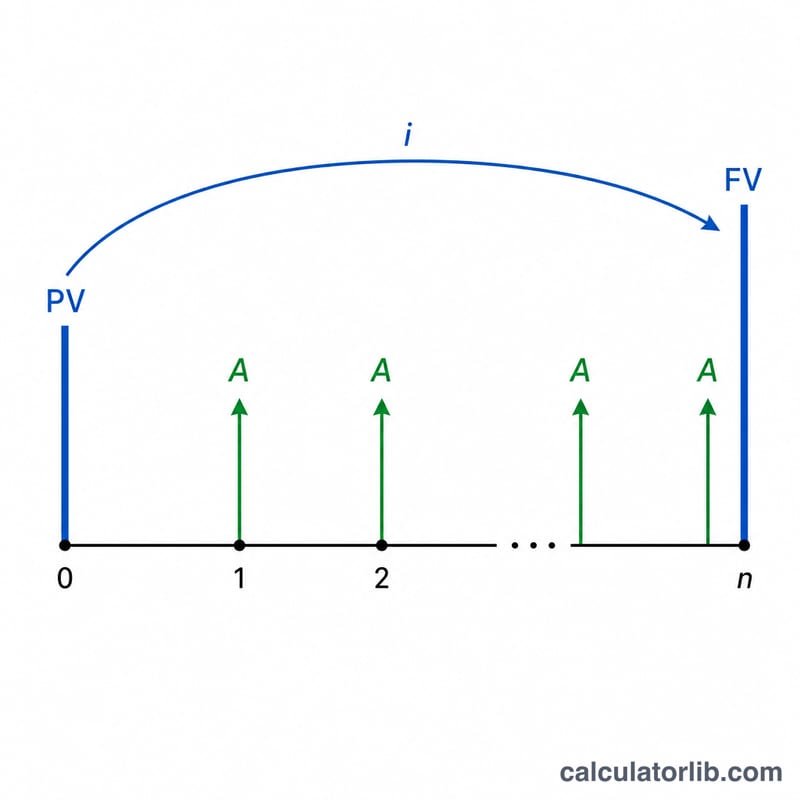

1. Future Value Factor = \((1+i)^{n}\) — grows a present lump sum. 2. Present Value Factor = \(\frac{1}{(1+i)^{n}}\) — discounts a future lump sum to today, the reciprocal of factor 1. 3. Sinking Fund Factor = \(\frac{i}{(1+i)^{n}-1}\) — the level deposit needed to reach a future target. 4. Capital Recovery Factor = \(\frac{i\,(1+i)^{n}}{(1+i)^{n}-1}\) — the level payment a present lump sum supports (loan payment per unit principal). 5. Future Value of Annuity Factor = \(\frac{(1+i)^{n}-1}{i}\) — what level deposits accumulate to, reciprocal of factor 3. 6. Present Value of Annuity Factor = \(\frac{1-(1+i)^{-n}}{i}\) — today's value of level payments, reciprocal of factor 4. Payments are assumed at the end of each period (ordinary annuity), and interest compounds once per year.

$$\begin{gathered} \begin{aligned} \text{FVF} &= (1+i)^{n} & \text{PVF} &= \frac{1}{(1+i)^{n}} \\[0.6em] \text{SFF} &= \frac{i}{(1+i)^{n}-1} & \text{CRF} &= \frac{i\,(1+i)^{n}}{(1+i)^{n}-1} \\[0.6em] \text{AFVF} &= \frac{(1+i)^{n}-1}{i} & \text{APVF} &= \frac{1-(1+i)^{-n}}{i} \end{aligned} \\[1.5em] \text{where}\quad \left\{ \begin{aligned} i &= \frac{\text{Annual rate (\%)}}{100} \\ n &= \text{Years} \end{aligned} \right. \end{gathered}$$

How to use it

Enter the annual interest rate (%), the number of years, the decimal places to display, and a rounding mode. The result table lists all six coefficients. Multiply the relevant coefficient by your amount: e.g., a target of 1,000,000 in 30 years at 2% needs deposits of \(1{,}000{,}000 \times \text{sinking fund factor}\).

Worked example

At 2% for 30 years: \((1.02)^{30} = 1.811361\). Future Value Factor = 1.811, Present Value Factor = 0.552, Sinking Fund Factor = 0.025, Capital Recovery Factor = 0.045, Future Value of Annuity Factor = 40.568, Present Value of Annuity Factor = 22.396 (rounded to 3 decimals, half up).

FAQ

Are payments at the start or end of the period? The end (ordinary annuity), matching the conventional FP-exam tables.

What if the rate is 0%? Limiting forms apply: the lump-sum factors become 1, the annuity value factors become \(n\), and the deposit/payment factors become \(\frac{1}{n}\).

Why do some coefficients multiply to 1? They are reciprocal pairs: factor 1 \(\times\) factor 2 = 1, factor 3 \(\times\) factor 5 = 1, factor 4 \(\times\) factor 6 = 1.