What this calculator does

This tool builds a complete year-by-year depreciation schedule for a fixed asset. It supports five common accounting methods — Straight Line, Double Declining Balance, 150% Declining Balance, Sum of Years' Digits, and Units of Production — and shows either a simple list of annual expenses or a full schedule with beginning book value, depreciation, accumulated depreciation, and ending book value.

The underlying math is universal accounting depreciation. The fiscal-year and convention options (mid-month, mid-quarter, half-year) mirror US tax practice such as MACRS conventions, but no jurisdiction-specific tax tables are applied, so the schedule is useful for general financial planning anywhere.

How to use it

Pick a method, then enter the asset cost, salvage (residual) value, and useful life in years. Choose the month and year the asset was placed in service, your fiscal year, and a convention that decides how much of the first partial period is taken. Turn on "Round to Dollars" for whole-dollar entries, and choose "Full Schedule" to see every column. For Units of Production, enter the total units expected over the asset's life and a comma-separated list of units produced each year.

The formulas explained

The depreciable base is cost minus salvage, \(B = C - S\). Straight Line spreads \(B\) evenly:

$$D = \frac{B}{L}$$Sum of Years' Digits weights early years using

$$D_t = B \times \frac{L - t + 1}{L(L+1)/2}$$Declining balance methods apply a fixed rate (\(2/L\) or \(1.5/L\)) to the shrinking book value and never let it fall below salvage. Units of Production charges \(B / \text{total units}\) for each unit made.

Worked example

Straight Line, cost $10,000, salvage $1,000, life 5 years, placed in service January, calendar fiscal year, full-month, rounded. Base \(= \$9{,}000\), annual \(= \$1{,}800\). The schedule runs $1,800 each year for five years, ending book value lands exactly on the $1,000 salvage with $9,000 total depreciation.

Key Terms Defined

- Cost basis

- The total capitalized cost of acquiring and readying an asset for use — purchase price plus freight, installation, taxes, and setup. This is the \(C\) in the formulas and the starting book value.

- Salvage (residual) value

- The estimated amount the asset will be worth at the end of its useful life, \(S\). Depreciation stops once book value reaches salvage.

- Depreciable base

- The portion of cost that gets expensed over the asset's life: \(C - S\). Declining-balance methods apply their rate to book value rather than the base, but still stop at salvage.

- Useful life

- The number of periods (\(L\), usually years) over which the asset is expected to generate value. Used directly by SL, SYD, and the declining-balance rate.

- Book value

- Cost minus accumulated depreciation at a point in time — the asset's carrying amount on the balance sheet.

- Accumulated depreciation

- The running total of all depreciation expense taken to date. It is a contra-asset that reduces gross asset cost to book value.

- Half-year convention

- Assumes the asset was placed in service at the midpoint of the year, granting one half-year of depreciation in the first (and last) year regardless of the actual month.

- Mid-month convention

- Treats the asset as placed in or disposed of at the middle of the month, common for real property; the first month counts as half a month.

- Mid-quarter convention

- Treats assets placed in service during a quarter as placed at that quarter's midpoint — often required when a large share of assets is acquired late in the year.

- Units of production

- An activity-based method that ties expense to actual output: \(\tfrac{C-S}{\text{total estimated units}}\) per unit, multiplied by units produced each period.

What Your Depreciation Schedule Means

Each row of the schedule reports four linked figures. Beginning book value is the asset's carrying amount at the start of the year; subtracting that year's depreciation expense gives the ending book value, which becomes next year's beginning value. Accumulated depreciation is simply the sum of all expense recognized so far — it grows every period until it equals the depreciable base.

On financial statements, the income statement shows depreciation expense (lowering net income and, in turn, taxable income), while the balance sheet shows the asset at cost less accumulated depreciation. Because depreciation is a non-cash expense, it is added back on the cash-flow statement.

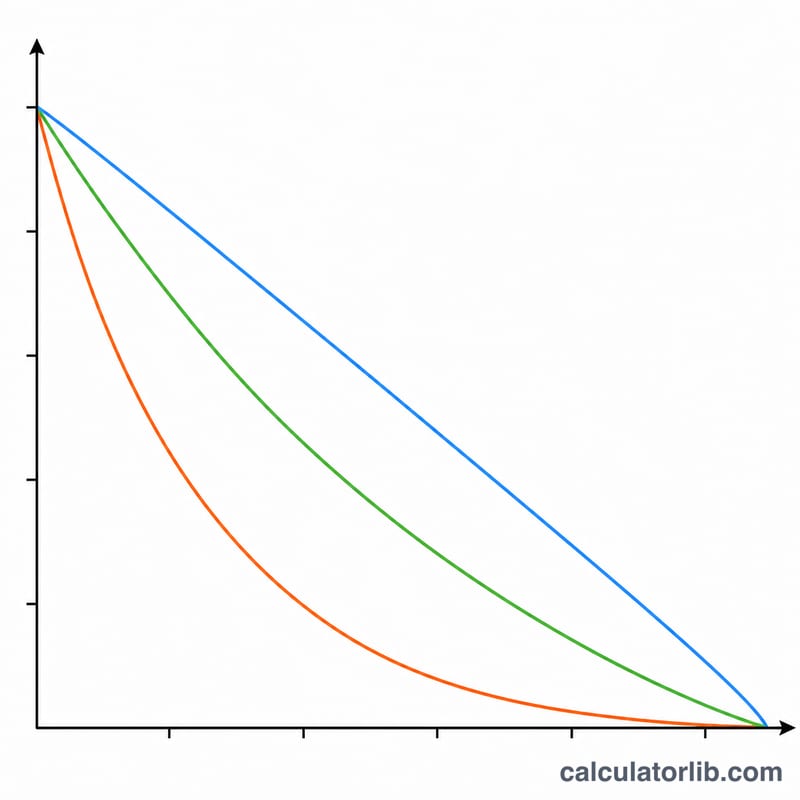

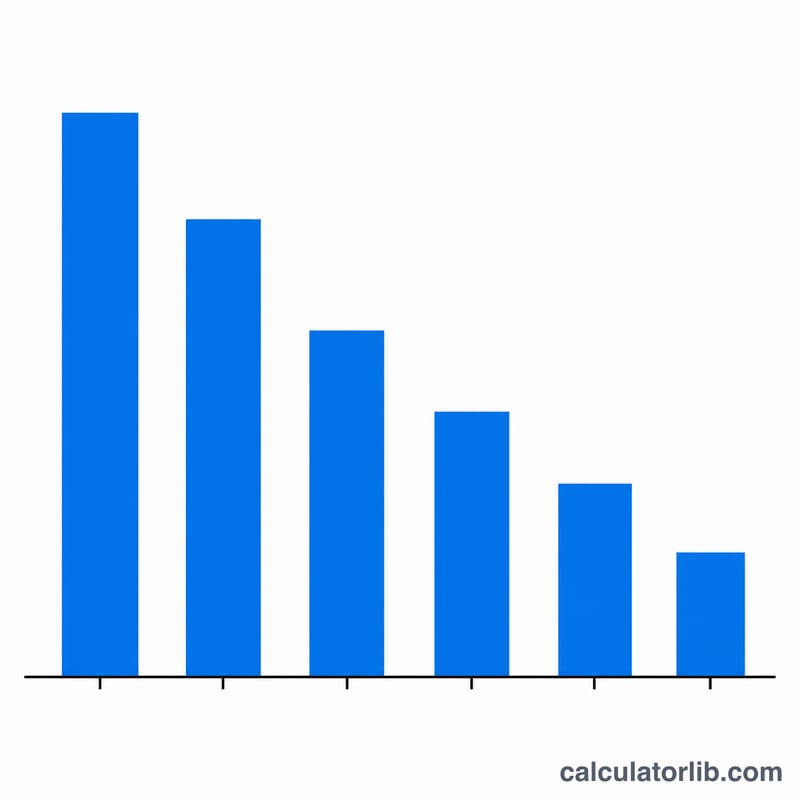

Why accelerated methods front-load expense: DDB, 150% DB, and SYD intentionally recognize more depreciation in early years and less later. This can better match the heavy early productivity (or rapid obsolescence) of equipment, defers tax in early years, and reduces reported book value faster. Straight line, by contrast, smooths expense evenly — preferred when an asset delivers value steadily across its life.

Choosing a method depends on the asset and your reporting goals: use Units of Production when wear depends on output (vehicles, machinery), accelerated methods for tech that loses value quickly, and straight line for stable, long-lived assets like buildings or furniture.

Planning note: this tool computes generic book-depreciation schedules and applies no jurisdiction-specific tax tables. For U.S. tax depreciation you would generally use prescribed MACRS percentages, and bonus depreciation or Section 179 rules can change first-year amounts entirely. Treat these results as general financial-planning estimates, not tax or accounting advice — confirm the correct method, life, and convention with your accountant or local tax authority before filing.

FAQ

Why does my schedule have an extra year? When the asset is placed in service partway through the fiscal year, a fraction of the first year's expense shifts forward, so a 5-year life can span six fiscal periods.

What does the half-year convention do? It takes exactly half a year of depreciation in year one and the remaining half after the last full year, regardless of the placed-in-service month.

Why is my book value never below salvage? Declining-balance methods are clamped so the asset is never depreciated below its salvage value; the final period is adjusted to land exactly on salvage.