What is straight-line depreciation?

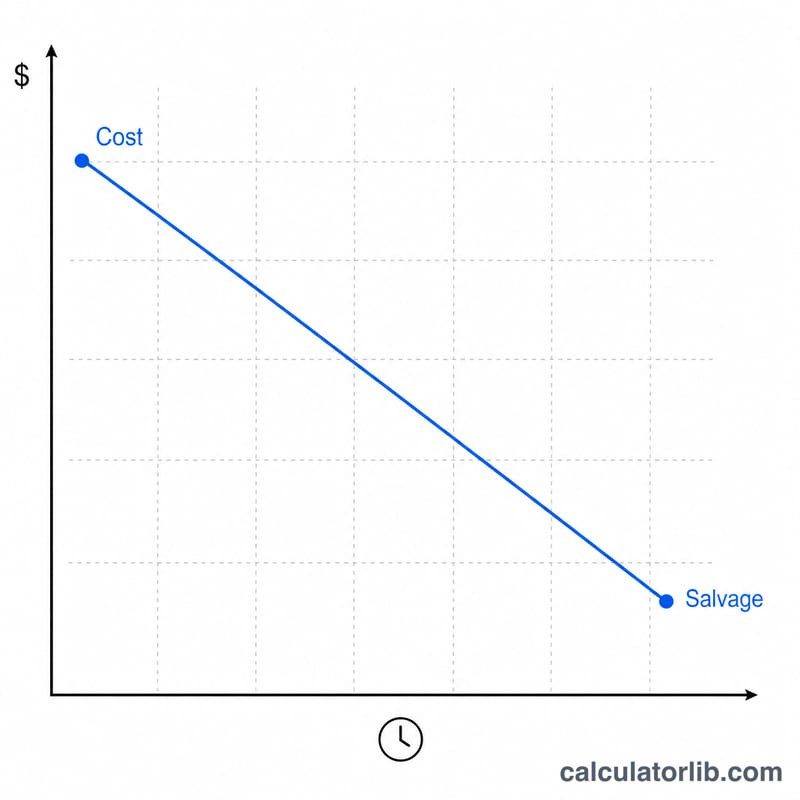

Straight-line depreciation spreads the cost of a fixed asset evenly over its useful life. It is the simplest and most widely used depreciation method in accounting. The annual expense equals the depreciable base (cost minus salvage value) divided by the number of years of useful life, exactly matching Microsoft Excel's =SLN(cost, salvage, life) function. This calculator goes further by prorating the first (and trailing) fiscal year so the schedule reflects exactly when the asset was placed in service.

How to use this calculator

Enter the asset cost, its estimated salvage value, and the useful life in years. Select the month and year the asset was placed in service, then choose your fiscal (tax) year start month. Pick a depreciation convention — full-month, mid-month, mid-quarter, or half-year — to control how much of the placement period is taken. Toggle "Round to Dollars" for whole-dollar amounts and choose "Full Schedule" to see a year-by-year breakdown of expense, accumulated depreciation, and ending book value.

The formula explained

The annual amount is $$\text{Annual Depreciation} = \dfrac{\text{Cost} - \text{Salvage}}{\text{Useful Life}}$$ The monthly amount is that divided by 12. Because an asset rarely starts at the beginning of a fiscal year, the first year receives only a fraction: \(\text{first-year months} \div 12\). The leftover fraction carries into one extra trailing year so the totals always sum to \(\text{Cost} - \text{Salvage}\). Conventions adjust the placement period: mid-month gives half a month, mid-quarter places the asset at the quarter midpoint, and half-year always takes six months in the first year.

Worked example

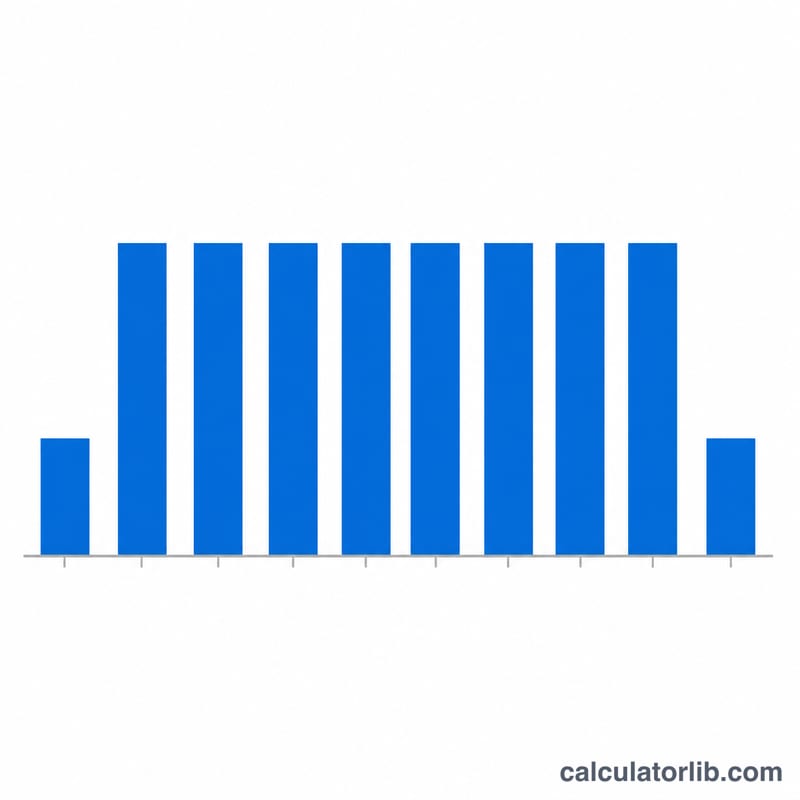

Cost $10,000, salvage $1,000, life 5 years, placed in service March 2020, Jan–Dec fiscal year, full-month convention. Depreciable base = $9,000; annual depreciation = $$\$9{,}000 / 5 = \$1{,}800$$ monthly = $150. March is the 3rd fiscal month, so 13 − 3 = 10 months of depreciation in 2020: $$\$150 \times 10 = \$1{,}500$$ Years 2021–2024 each take $1,800, and the trailing year 2025 takes the remaining $300. The expenses sum to exactly $9,000, leaving a final book value of $1,000 (the salvage).

FAQ

Why does the schedule span one extra year? Because the first year is partial, the unused fraction rolls into an additional trailing fiscal year so the asset is fully depreciated to its salvage value.

What if salvage value is greater than cost? The depreciable base cannot be negative, so depreciation is set to zero and the book value stays at cost.

Does the book value ever go below salvage? No. The final year absorbs any rounding remainder so accumulated depreciation equals cost minus salvage exactly and the ending book value equals the salvage value.