What is straight-line depreciation?

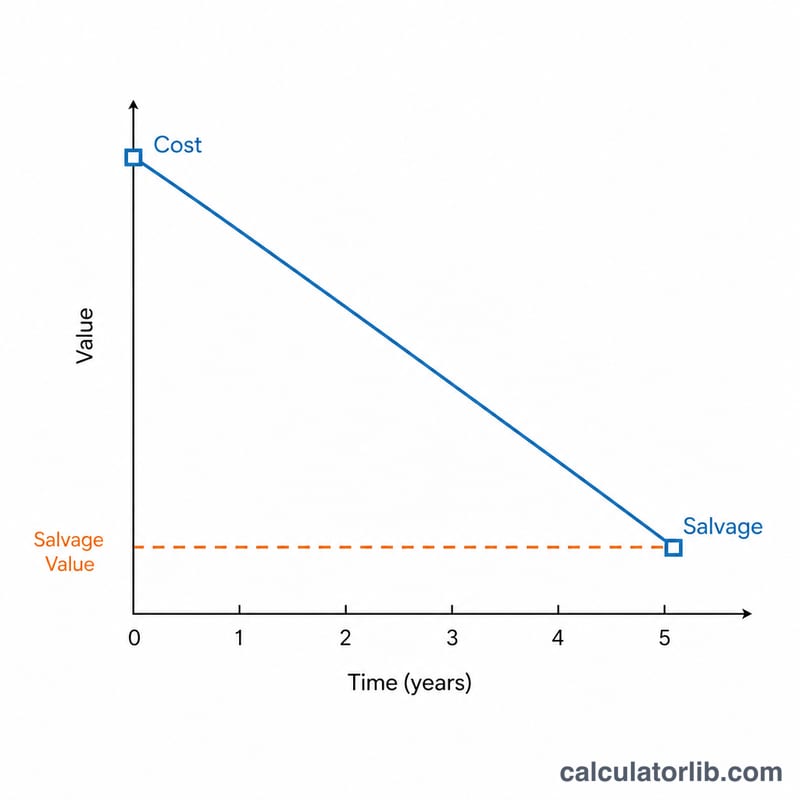

Straight-line (linear) depreciation spreads the cost of a fixed asset evenly across its useful life. Each year the same amount of expense is recorded, gradually reducing the asset book value from its original cost down to its salvage (residual) value. It is the simplest and most widely used depreciation method in accounting.

How to use this calculator

Enter the asset cost, its expected salvage value at the end of its life, the useful life in years, and how many years have elapsed (t). The calculator returns the constant annual depreciation, the accumulated depreciation to date, and the remaining book value.

The formula explained

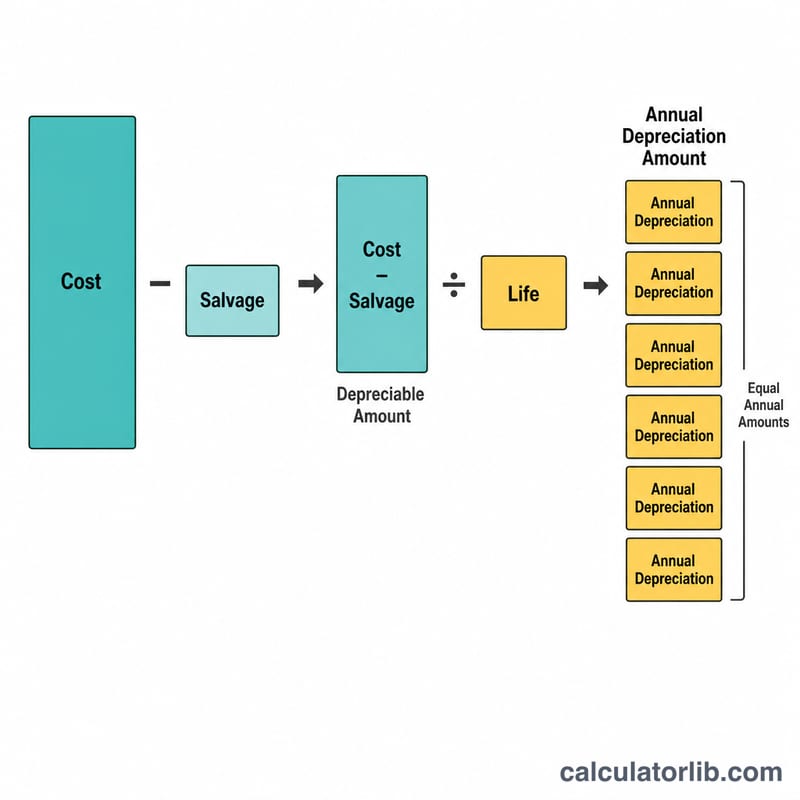

The depreciable base is the cost minus salvage value. Dividing by the useful life gives the annual depreciation expense: $$D = \frac{\text{Cost} - \text{Salvage}}{\text{Life}}$$ Multiplying by the number of years elapsed gives accumulated depreciation, and subtracting that from cost gives book value: $$V(t) = \text{Cost} - D \times t$$

Worked example

A machine costs 10,000 with a 1,000 salvage value and a 5-year life. The annual depreciation is $$\frac{10{,}000 - 1{,}000}{5} = 1{,}800 \text{ per year}$$ After 2 years the accumulated depreciation is 3,600, leaving a book value of \(10{,}000 - 3{,}600 = 6{,}400\).

FAQ

Can book value go below salvage value? Under straight-line accounting an asset should not be depreciated below salvage value, so stop once t reaches the useful life.

What is salvage value? It is the estimated amount the asset can be sold for at the end of its useful life, also called residual value.

Is this method allowed for taxes? Rules vary by country; many tax systems use accelerated methods instead, so check your local regulations before filing.