What Is Straight-Line Depreciation?

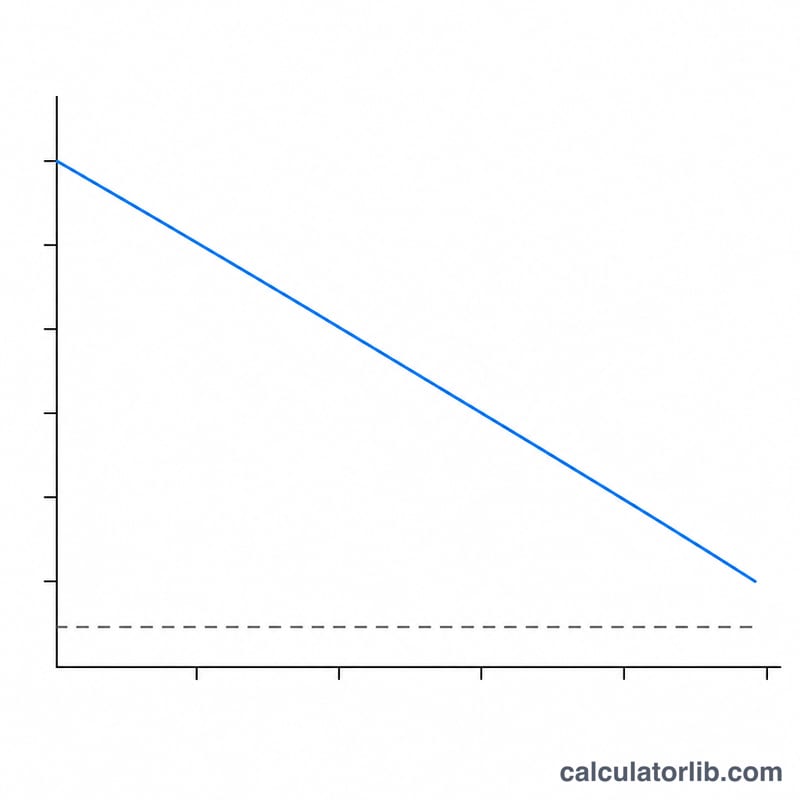

Straight-line depreciation is the simplest and most widely used method for allocating the cost of a fixed asset over its useful life. Instead of expensing the entire purchase in the year it was bought, you spread an equal amount across every year the asset is in service. This produces a steady, predictable expense that is easy to budget for and that appears consistently on your income statement and balance sheet.

How to Use This Calculator

Enter three values: the asset cost (the full purchase price plus any costs to get it ready for use), the salvage value (the estimated resale or scrap value at the end of its life), and the useful life in years. The calculator instantly returns the annual depreciation expense, the equivalent monthly figure, the total depreciable base, and the annual depreciation rate as a percentage of cost.

The Formula Explained

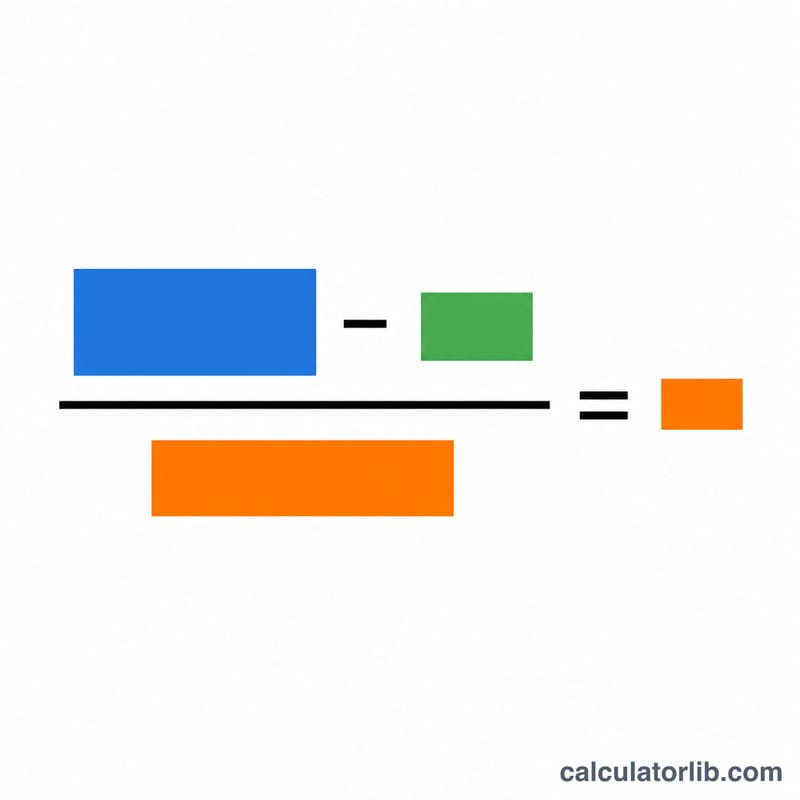

The core equation is $$\text{Annual Depreciation} = \frac{\text{Cost} - \text{Salvage Value}}{\text{Useful Life}}$$. The numerator, Cost − Salvage Value, is called the depreciable base—it is the portion of the asset's value that will actually be consumed. Dividing this base by the number of years gives the constant annual charge. Because the figure never changes from year to year, the method is called "straight-line."

Worked Example

Suppose a company buys a machine for $10,000, expects to sell it for $1,000 after 5 years. The depreciable base is $$\$10{,}000 - \$1{,}000 = \$9{,}000.$$ Dividing by 5 years gives $$\frac{\$9{,}000}{5} = \$1{,}800$$ of depreciation each year, or \(\$150\) per month. The annual rate is $$\frac{\$1{,}800}{\$10{,}000} = 18\%$$ of the original cost per year.

FAQ

Can salvage value be zero? Yes. If you expect the asset to be worthless at the end of its life, enter 0 and the full cost becomes the depreciable base.

What is useful life? It is the estimated number of years the asset will remain productive. Tax authorities and accounting standards often publish recommended lives for different asset classes.

How is straight-line different from declining balance? Straight-line charges the same amount every year, while declining-balance methods front-load larger expenses in the early years. Straight-line is preferred when an asset delivers value evenly over time.