What Is the Property Depreciation Calculator?

This tool applies to US rental and investment real estate under the IRS Modified Accelerated Cost Recovery System (MACRS), which uses the straight-line method for buildings. It estimates how much of a property you can deduct each year for wear and tear. Because land never wears out, only the building portion (the depreciable basis) is depreciated.

How to Use It

Enter the property cost basis (purchase price plus qualifying improvements), the land value, the recovery period (27.5 years for residential rental, 39 years for commercial), and the number of years held. The calculator returns the annual deduction, the depreciable basis, accumulated depreciation, and the remaining basis.

The Formula

The depreciable basis is the building value after removing land. The straight-line annual deduction is:

$$D = \frac{C - L}{N}$$where \(C\) = total cost basis, \(L\) = land value, and \(N\) = recovery period in years. Accumulated depreciation after \(Y\) years is \(A = D \times Y\).

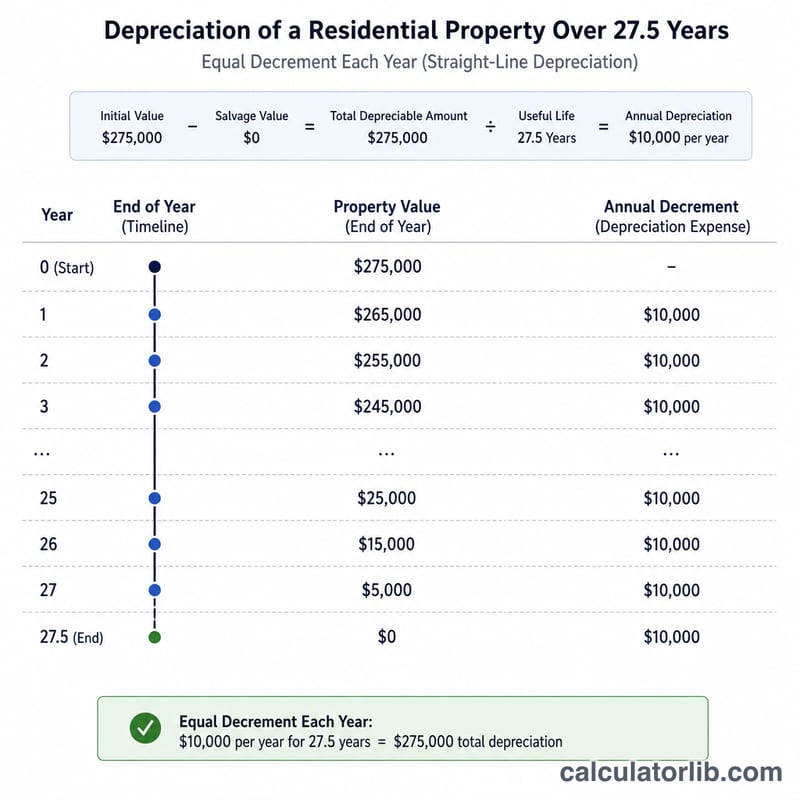

Worked Example

A residential rental costs $300,000 with land worth $50,000, held for 5 years on a 27.5-year schedule:

$$D = \frac{300000 - 50000}{27.5} = \$9090.91$$ $$A = 9090.91 \times 5 = \$45454.55$$The remaining basis is \(250000 - 45454.55 = \$204545.45\).

Key Terms Defined

- Cost Basis

- The total amount invested in the property for tax purposes — generally the purchase price plus certain acquisition costs (such as legal fees, title fees, and recording charges) and the cost of capital improvements.

- Depreciable Basis

- The portion of the cost basis that may be depreciated. It equals the cost basis minus the land value, because land does not wear out and cannot be depreciated.

- Land Value

- The allocated value of the underlying land, commonly estimated from the property tax assessor's ratio of land to total assessed value. This amount is excluded from the depreciable basis.

- Recovery Period

- The number of years over which the IRS allows the building to be depreciated: 27.5 years for residential rental property and 39 years for nonresidential (commercial) property.

- MACRS

- The Modified Accelerated Cost Recovery System, the depreciation system required for most US real property placed in service after 1986. For real estate, MACRS uses the straight-line method over the assigned recovery period.

- Straight-Line Method

- A depreciation method that deducts an equal amount of the depreciable basis each year, calculated as the depreciable basis divided by the recovery period. Real property under MACRS must use this method.

- Accumulated Depreciation

- The running total of all depreciation deductions claimed (or allowable) on the property since it was placed in service.

- Adjusted Basis

- The cost basis increased by capital improvements and decreased by accumulated depreciation. It is used to determine taxable gain or loss when the property is sold.

- Depreciation Recapture

- At sale, the requirement to treat gain attributable to prior depreciation as a distinct category of income. For real property this is unrecaptured Section 1250 gain, taxed at a federal maximum of 25%.

- Mid-Month Convention

- The MACRS rule for real property treating the asset as placed in service (and disposed of) at the midpoint of the month, so the first and last years receive a prorated deduction rather than a full year.

FAQ

Why exclude land? The IRS does not allow depreciation on land because it does not deteriorate over time.

What is the recovery period? Residential rental property uses 27.5 years; non-residential (commercial) property uses 39 years.

Is this tax advice? No. This is a simplified straight-line estimate that ignores the mid-month convention and partial first-year proration. Consult a tax professional.