What Is the MACRS Depreciation Calculator?

This calculator applies the United States Modified Accelerated Cost Recovery System (MACRS), the standard IRS method for depreciating business property placed in service after 1986. It uses the official IRS Publication 946 percentage tables for the half-year convention, where 200% declining balance applies to 3-, 5-, 7-, and 10-year property and 150% declining balance applies to 15- and 20-year property, both switching to straight-line when advantageous. This tool is US-specific and assumes the half-year convention (not mid-quarter or mid-month).

How to Use It

Enter the depreciable basis (typically the cost of the asset) and choose the property class that matches the asset's recovery period. The calculator returns the first-year deduction plus a full year-by-year schedule showing the IRS rate, annual depreciation, and accumulated depreciation. Common examples: computers and cars are 5-year property, office furniture is 7-year, and land improvements are 15-year.

The Formula Explained

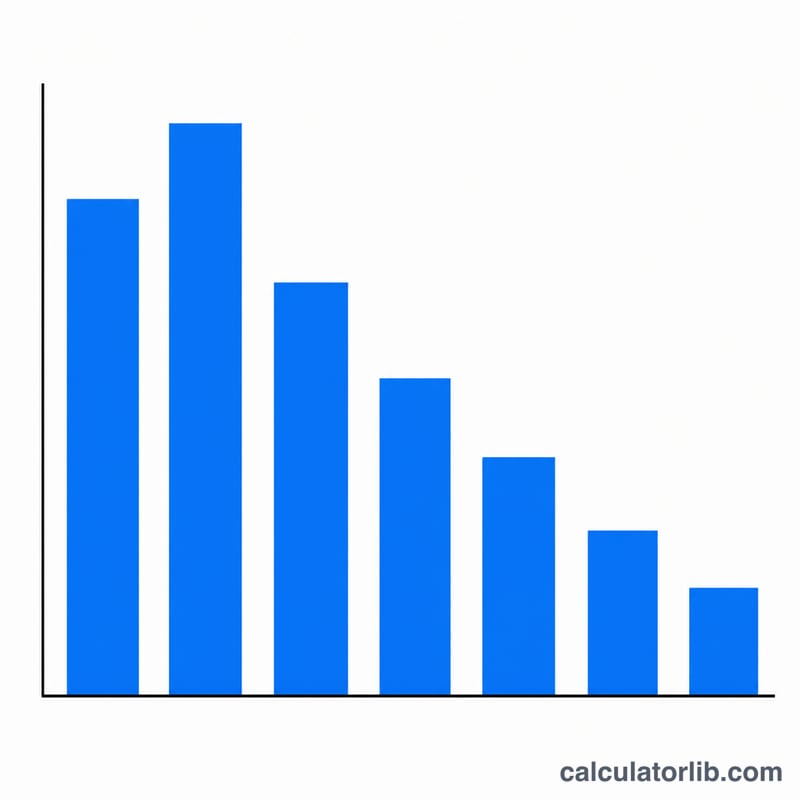

For each recovery year, depreciation equals the basis times the published percentage: $$D_{\text{year}} = \text{Basis} \times \frac{r_{\text{year}}}{100}$$ Because MACRS front-loads deductions, early years carry higher percentages. The half-year convention treats all property as placed in service at mid-year, which is why a 5-year asset is actually depreciated over six tax years.

Worked Example

A $10,000 asset classified as 5-year property has a first-year rate of 20.00%. First-year depreciation $$= \$10{,}000 \times 0.2000 = \$2{,}000$$ Year 2 uses 32.00% for \(\$3{,}200\), and so on until the basis is fully recovered over six years.

FAQ

Why does a 5-year asset take 6 years? The half-year convention spreads the first year's depreciation across a half year, leaving a remainder that is recovered in an extra final year.

Does this include bonus depreciation or Section 179? No. This shows regular MACRS only; bonus depreciation and Section 179 expensing are applied separately before MACRS.

Which convention does it use? The half-year convention, the most common default for personal property.