What Is Accumulated Depreciation?

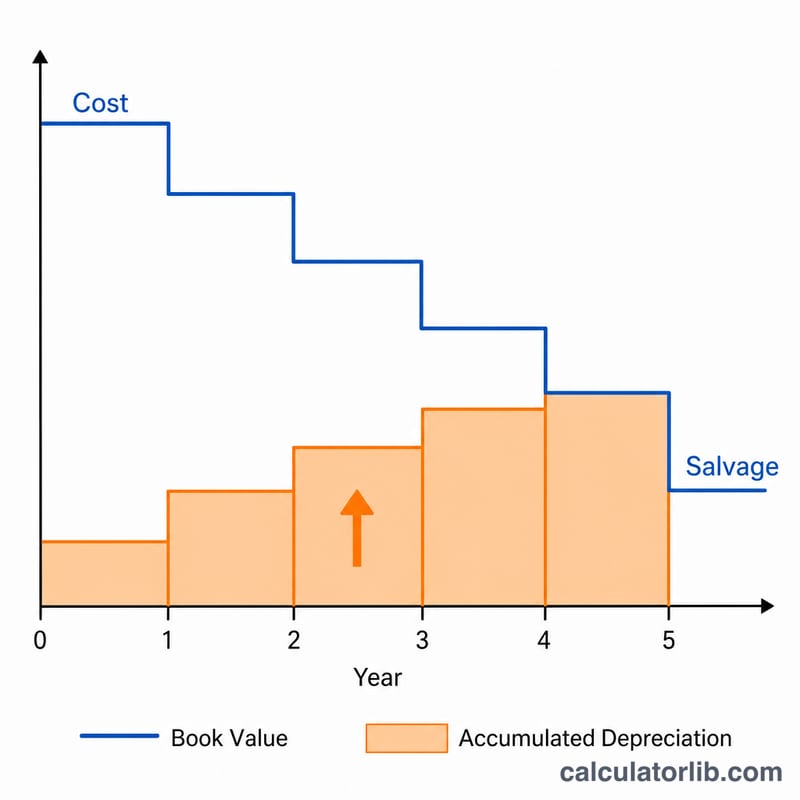

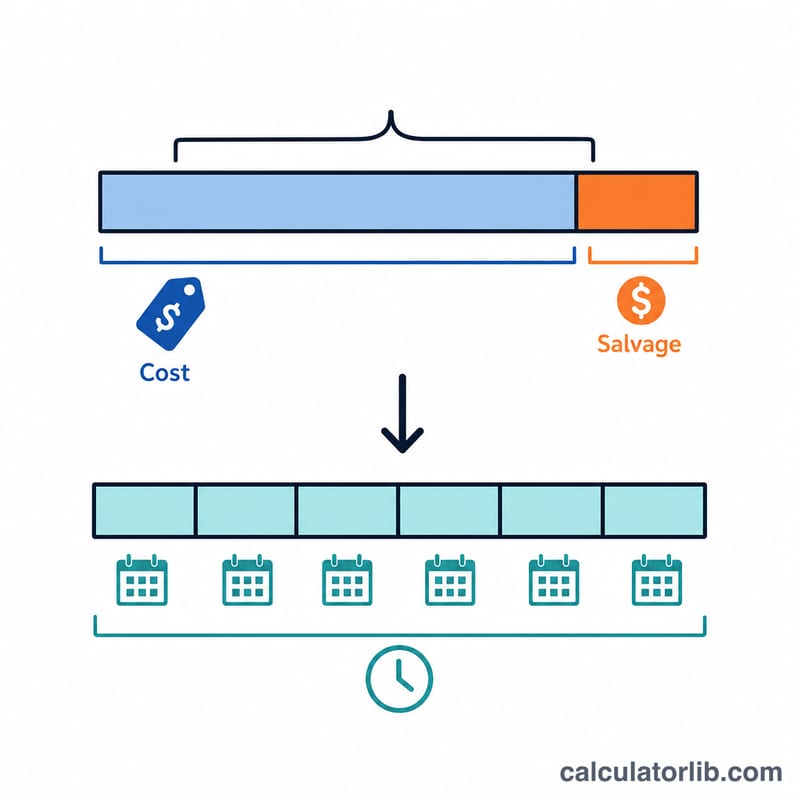

Accumulated depreciation is the total amount of depreciation expense that has been recorded against a fixed asset since it was put into service. It is a contra-asset account that reduces the gross value of property, plant, and equipment on the balance sheet. This calculator uses the straight-line method, the most common and simplest approach, which spreads an asset's depreciable cost evenly across its useful life.

How to Use This Calculator

Enter four values: the original asset cost, the estimated salvage value (what the asset is expected to be worth at the end of its life), the useful life in years, and the number of years elapsed since the asset was placed in service. The calculator returns the accumulated depreciation, the annual depreciation expense, and the current book value.

The Formula Explained

The annual straight-line depreciation equals the depreciable base (cost minus salvage value) divided by the useful life. Multiply that annual figure by the number of years elapsed to get accumulated depreciation:

$$\text{Accumulated Depreciation} = \dfrac{\text{Cost} - \text{Salvage}}{\text{Useful Life}} \times \text{Years Elapsed}$$Book value is then simply the cost minus accumulated depreciation. Note that accumulated depreciation never exceeds the depreciable base, so years elapsed is capped at the useful life.

Worked Example

Suppose a machine costs $10,000, has a salvage value of $1,000, and a useful life of 5 years. The annual depreciation is $$(\$10{,}000 - \$1{,}000) \div 5 = \$1{,}800.$$ After 2 years, accumulated depreciation is $$\$1{,}800 \times 2 = \$3{,}600,$$ and the book value is $$\$10{,}000 - \$3{,}600 = \$6{,}400.$$

Typical Useful Life by Asset Class

The straight-line method spreads an asset's depreciable base (cost minus salvage value) evenly across its useful life. Choosing a reasonable useful life is therefore central to the calculation. The ranges below reflect common accounting conventions and IRS guidance for general business assets; the exact life you use should follow your accounting policy, the asset's expected service period, and—for tax purposes—the recovery period assigned by IRS Publication 946 (MACRS).

| Asset Class | Examples | Typical Useful Life (years) |

|---|---|---|

| Buildings (nonresidential) | Offices, warehouses, retail structures | 39 (IRS); 30–40 book |

| Buildings (residential rental) | Apartment buildings, rental homes | 27.5 (IRS) |

| Machinery & equipment | Production machines, heavy equipment | 7–15 |

| Vehicles | Cars, light trucks, vans | 5 |

| Office equipment | Copiers, printers, telephone systems | 5–7 |

| Furniture & fixtures | Desks, chairs, shelving, cabinets | 7 |

| Computers & peripherals | PCs, servers, laptops, monitors | 3–5 |

For example, a machine purchased for $50,000 with a $5,000 salvage value and a 10-year useful life depreciates at \((50000-5000)/10 = \$4{,}500\) per year. After 4 years, accumulated depreciation is \(\$4{,}500 \times 4 =\) $18,000.

Interpreting Your Result

Accumulated depreciation is a contra-asset account. On the balance sheet it is reported as a deduction directly beneath (or netted against) the related property, plant, and equipment (PP&E) line. It carries a credit balance that grows each period as depreciation expense is recorded, while the asset's original cost stays unchanged at its historical amount.

The relationship to net PP&E (also called net book value or carrying value) is:

$$\text{Net Book Value} = \text{Cost} - \text{Accumulated Depreciation}$$

Continuing the earlier example, an asset costing $50,000 with $18,000 of accumulated depreciation has a net book value of \(50000 - 18000 = \$32{,}000\). Each year that figure declines by the annual depreciation amount until it reaches the asset's salvage value, after which no further straight-line depreciation is taken.

Two points are important when reading this result:

- It is a book value, not market value. Net book value reflects an allocation of historical cost over time; it is not an estimate of what the asset would sell for. The market value of equipment, vehicles, or buildings can be substantially higher or lower than their carrying amount.

- It is book depreciation, not tax depreciation. Financial-statement (book) depreciation under the straight-line method often differs from the amount claimed on a tax return, which in the United States typically uses MACRS recovery periods and accelerated rates. These timing differences are a common source of deferred taxes.

This explanation is general accounting information, not financial, tax, or accounting advice. Consult a qualified professional for the treatment appropriate to your specific situation.

FAQ

Is this the same as depreciation expense? No. Depreciation expense is the amount for a single period, while accumulated depreciation is the running total recorded to date.

Can accumulated depreciation exceed the asset cost? No. It is limited to the depreciable base (cost minus salvage), so book value never falls below salvage value.

What if I use a different method? This tool assumes straight-line depreciation. Declining-balance or units-of-production methods produce different schedules.