What Is Straight-Line Depreciation?

Straight-line depreciation is the simplest and most widely used method for allocating the cost of a fixed asset over its useful life. Each year you expense the same fixed amount, which makes financial reporting predictable and easy to audit. This calculator works for any currency and is used worldwide for accounting and tax planning, though specific tax rules vary by jurisdiction.

How to Use This Calculator

Enter the asset's original purchase cost, its estimated salvage (residual) value at the end of its life, and the number of years you expect to use it. The calculator instantly returns the annual depreciation expense, the equivalent monthly figure, the total depreciable base, and the yearly depreciation rate.

The Formula Explained

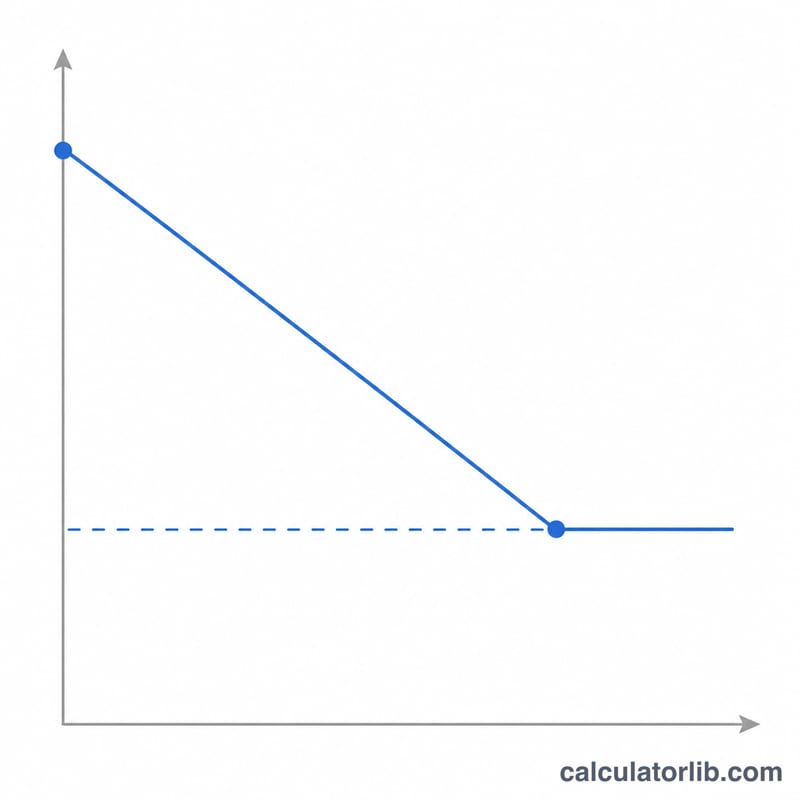

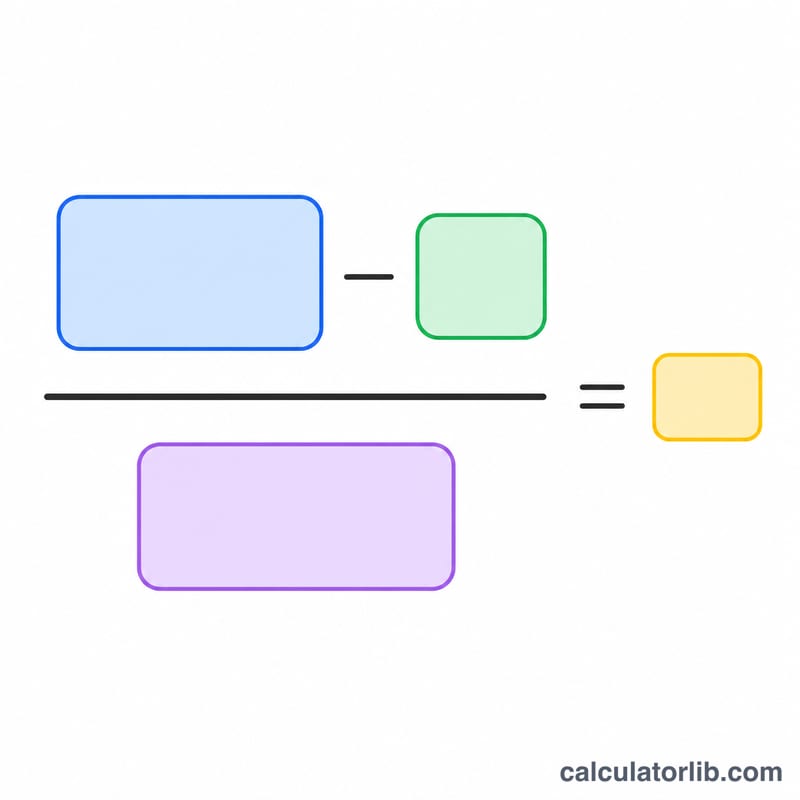

The depreciable base is the cost minus the salvage value — the portion of the asset's value you will actually consume. Dividing that base by the useful life in years gives the constant annual expense:

$$\text{Annual Depreciation} = \frac{\text{Cost} - \text{Salvage Value}}{\text{Useful Life}}$$

The depreciation rate is simply one divided by the useful life, expressed as a percentage.

Worked Example

Suppose a company buys a machine for $10,000, expects to sell it for $1,000 (salvage) after 5 years of use. The depreciable base is \(\$10{,}000 - \$1{,}000 = \$9{,}000\). Dividing by 5 years gives $$\frac{\$9{,}000}{5} = \$1{,}800$$ of depreciation per year, or $150 per month. The annual rate is \(1 \div 5 = 20\%\).

FAQ

Can salvage value be zero? Yes. If you expect no resale value, enter 0 and the full cost is depreciated over the useful life.

Does this account for partial first years? No — this gives the full-year amount. For an asset placed mid-year, prorate the first year using the monthly figure shown.

How is this different from declining balance? Straight-line expenses an equal amount every year; declining-balance methods front-load larger expenses in early years.