What Is Declining Balance Depreciation?

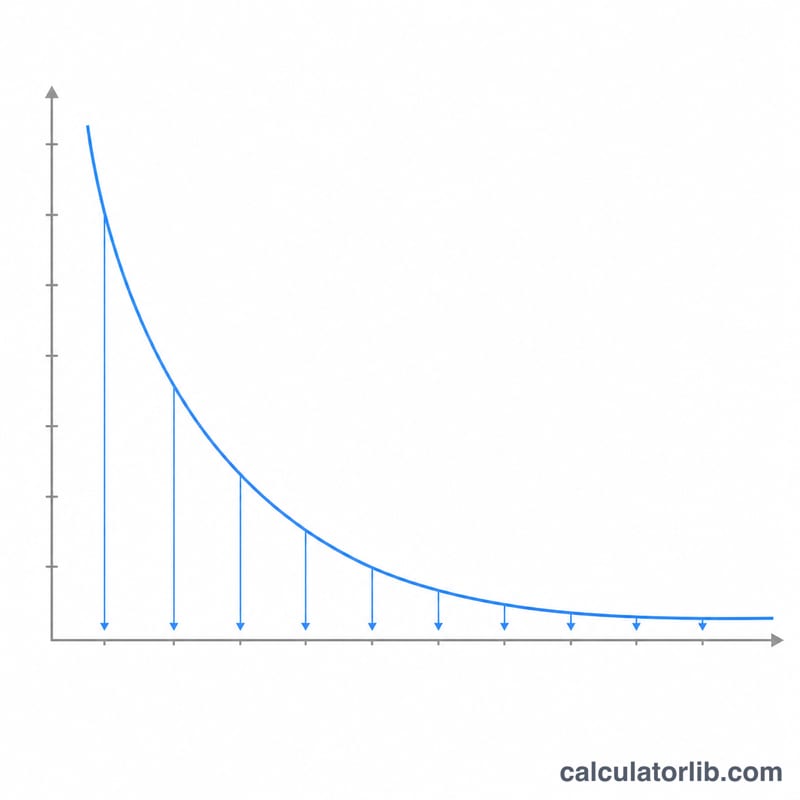

The declining balance method is an accelerated depreciation technique that writes off a larger portion of an asset's value in its early years and progressively less over time. Unlike straight-line depreciation, which spreads cost evenly, declining balance applies a fixed percentage rate to the asset's remaining book value each year. This mirrors how many assets — vehicles, machinery, and electronics — lose value fastest when new.

How to Use This Calculator

Enter the asset's original cost, its estimated salvage value (what it's worth at the end of its useful life), the useful life in years, and the depreciation factor. A factor of 2 produces the popular Double Declining Balance (DDB) method, while 1.5 gives the 150% method. The calculator returns the depreciation rate, the first year's depreciation expense, the book value after year one, and the total depreciation over the asset's full life — never depreciating below salvage value.

The Formula Explained

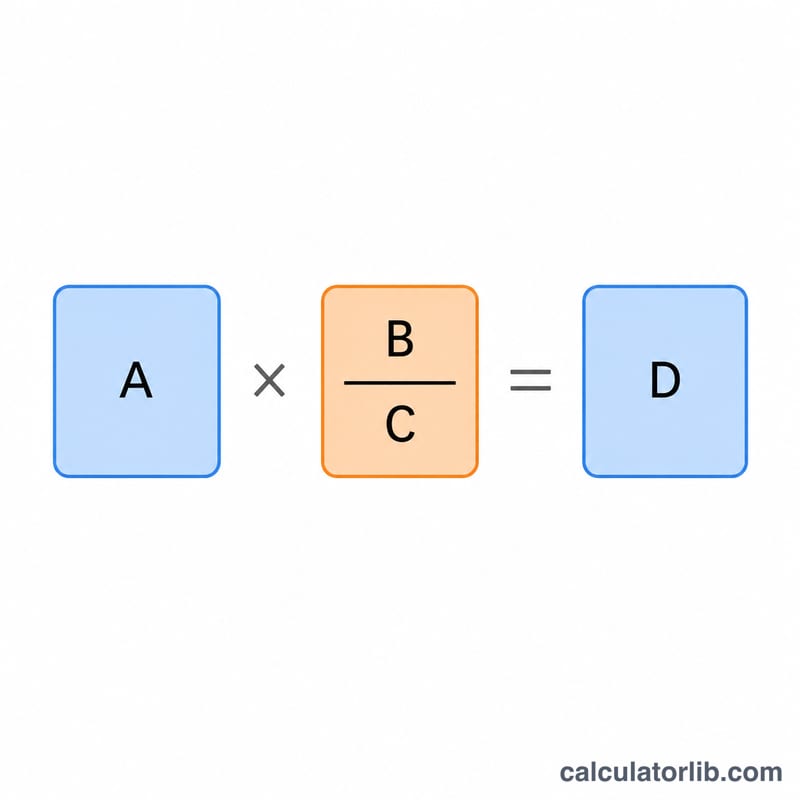

First compute the rate: \(\text{rate} = \frac{\text{factor}}{\text{useful life}}\). Then each year, \(\text{Depreciation} = \text{Book Value}_{start} \times \text{rate}\), and the ending book value is the starting value minus that depreciation. Because the rate stays constant but is applied to a shrinking balance, the dollar amount declines every year.

$$\text{Depreciation} = \text{Book Value}_{start} \times \frac{\text{factor}}{\text{useful life}}$$

Worked Example

Suppose a machine costs $10,000 with a $1,000 salvage value, a 5-year life, and a factor of 2. The rate is \(2 \div 5 = 40\%\). Year 1 depreciation is

$$\$10{,}000 \times 40\% = \$4{,}000$$leaving a book value of $6,000. The schedule continues until the book value reaches the $1,000 salvage floor.

FAQ

What is the difference between declining balance and double declining balance? Double declining balance simply uses a factor of 2. Declining balance is the general method that can use any factor.

Why doesn't depreciation reach zero? An asset should never be depreciated below its salvage value, so the final year's expense is capped to land the book value exactly at salvage.

Can the rate exceed 100%? For very short useful lives a high factor can produce a rate over 100%; in practice the salvage floor limits how much can be written off.