What Is Double Declining Balance Depreciation?

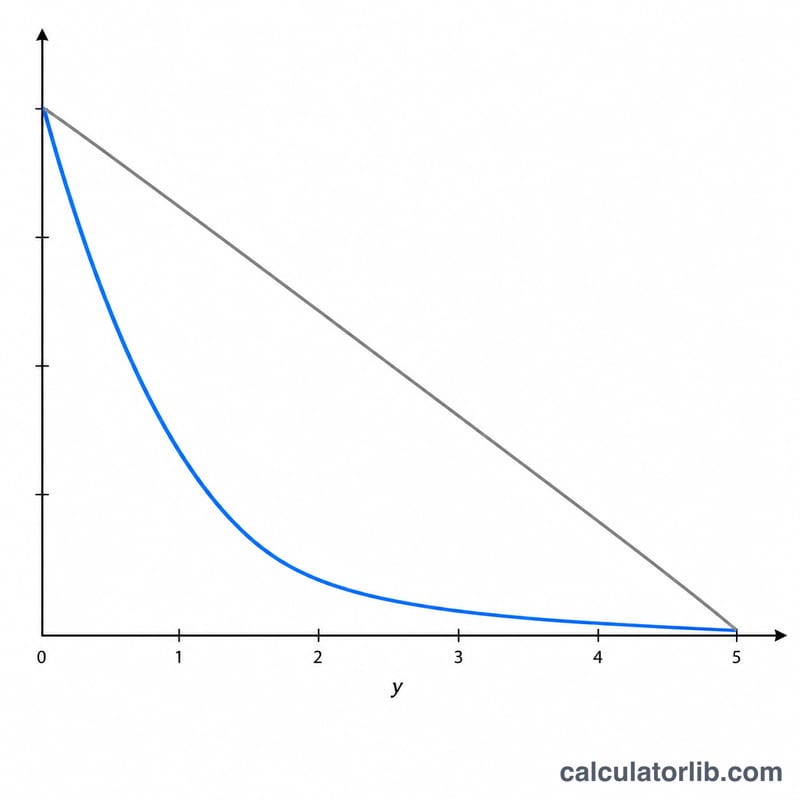

The double declining balance (DDB) method is an accelerated depreciation technique that records larger depreciation expenses in the early years of an asset's life and smaller amounts later. It is popular for assets like vehicles, computers, and machinery that lose value quickly. This calculator finds the first-year depreciation, the DDB rate, and the resulting book value.

How to Use This Calculator

Enter the asset's original cost, its estimated salvage value (what it will be worth at the end of its life), and the useful life in years. The tool computes the depreciation for the first year. In later years you simply apply the same rate to the new (lower) book value — depreciation stops once the book value reaches the salvage value.

The Formula Explained

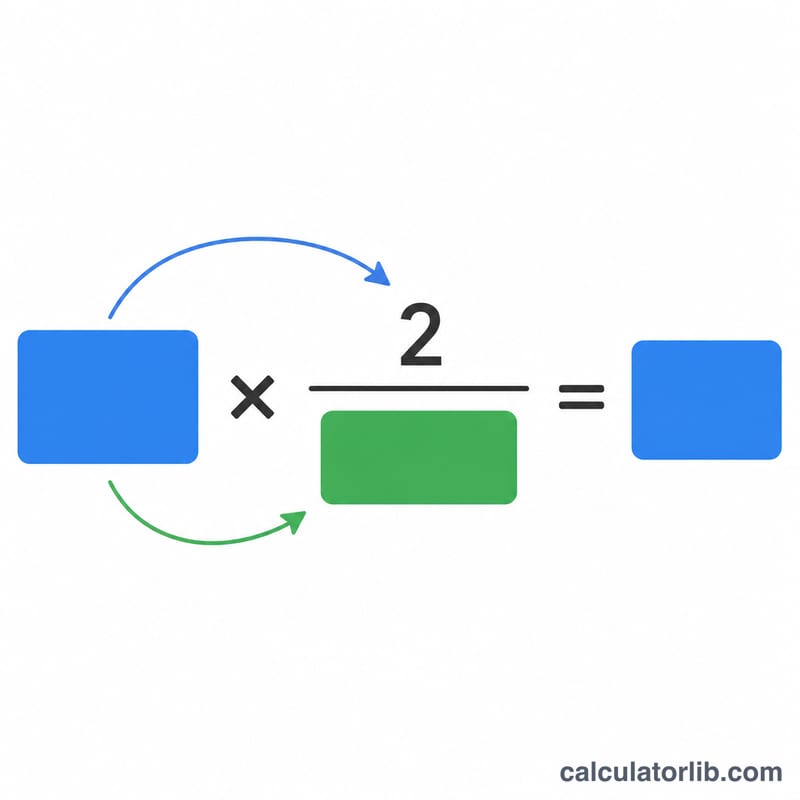

The DDB rate is twice the straight-line rate: \( \text{Rate} = \frac{2}{\text{Useful Life}} \). Each year's depreciation is the beginning book value multiplied by this rate:

$$\text{Depreciation}_{year} = \text{BookValue}_{start} \times \frac{2}{\text{Useful Life}}$$Salvage value is ignored when calculating the rate but acts as a floor — an asset is never depreciated below its salvage value.

Worked Example

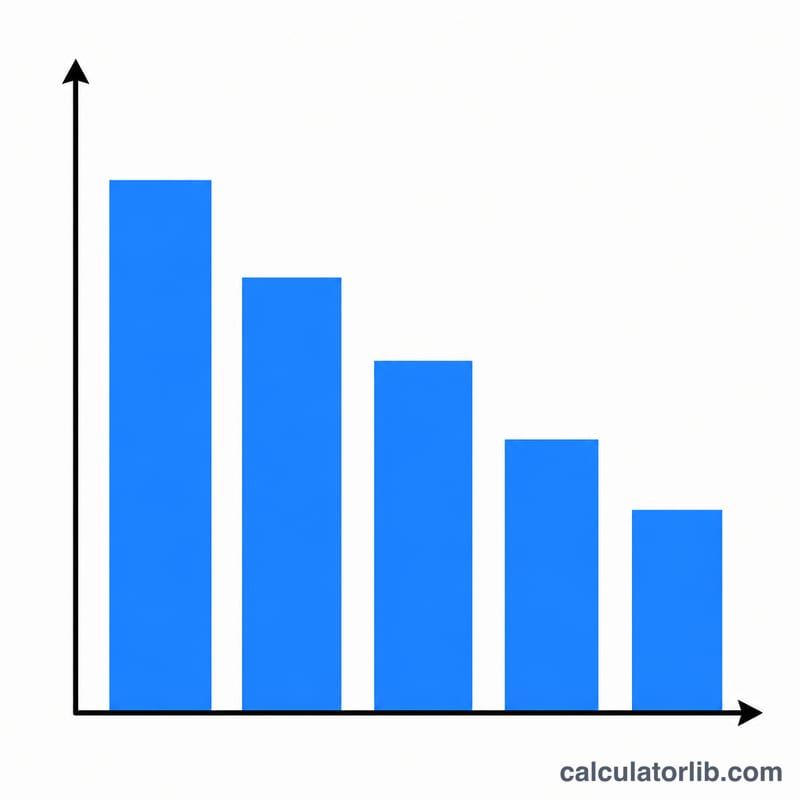

Suppose an asset costs $10,000 with a $1,000 salvage value and a 5-year useful life. The DDB rate is \( \frac{2}{5} = 40\% \). First-year depreciation is:

$$\$10{,}000 \times 40\% = \$4{,}000$$The book value at the end of year 1 is \( \$10{,}000 - \$4{,}000 = \$6{,}000 \). In year 2 you would depreciate \( \$6{,}000 \times 40\% = \$2{,}400 \), and so on.

FAQ

Why is salvage value not in the rate? Unlike straight-line depreciation, DDB applies the rate to the full book value. Salvage value only stops depreciation once book value reaches it.

Is DDB allowed for taxes? Accelerated methods like DDB are common in financial reporting; specific tax rules (such as MACRS in the US) vary by jurisdiction, so consult a tax professional.

What happens in the final years? Many companies switch to straight-line for the remaining book value once it exceeds the DDB amount, to fully depreciate the asset down to salvage value.