What Is Variable Declining Balance Depreciation?

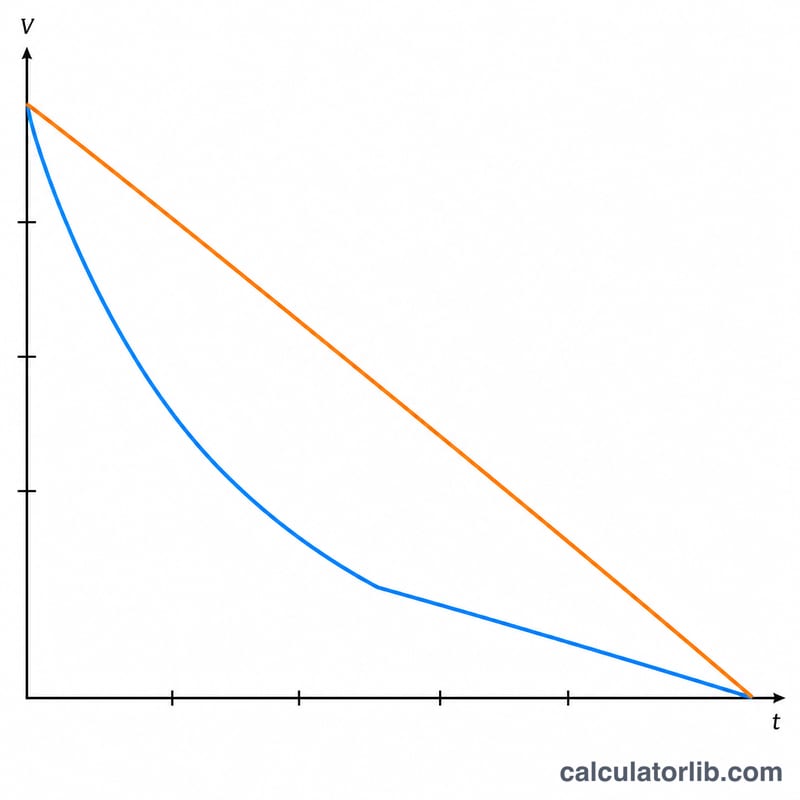

Variable Declining Balance (VDB) is an accelerated depreciation method that writes off more of an asset's value in its early years. Unlike straight-line depreciation, which spreads cost evenly, the declining balance approach applies a constant rate to the asset's shrinking book value, producing larger expenses up front. The "variable" factor lets you choose how aggressive the acceleration is — a factor of 2 gives the popular Double Declining Balance (200%) method, while 1.5 gives 150% declining balance.

How to Use This Calculator

Enter the asset's original cost, its expected salvage value (what it's worth at the end of its life), the useful life in years, and the declining factor. Pick which year you want to inspect. The calculator returns that year's depreciation expense, the depreciation rate, the cumulative depreciation through that year, and the ending book value. Depreciation is automatically capped so the book value never falls below salvage.

The Formula Explained

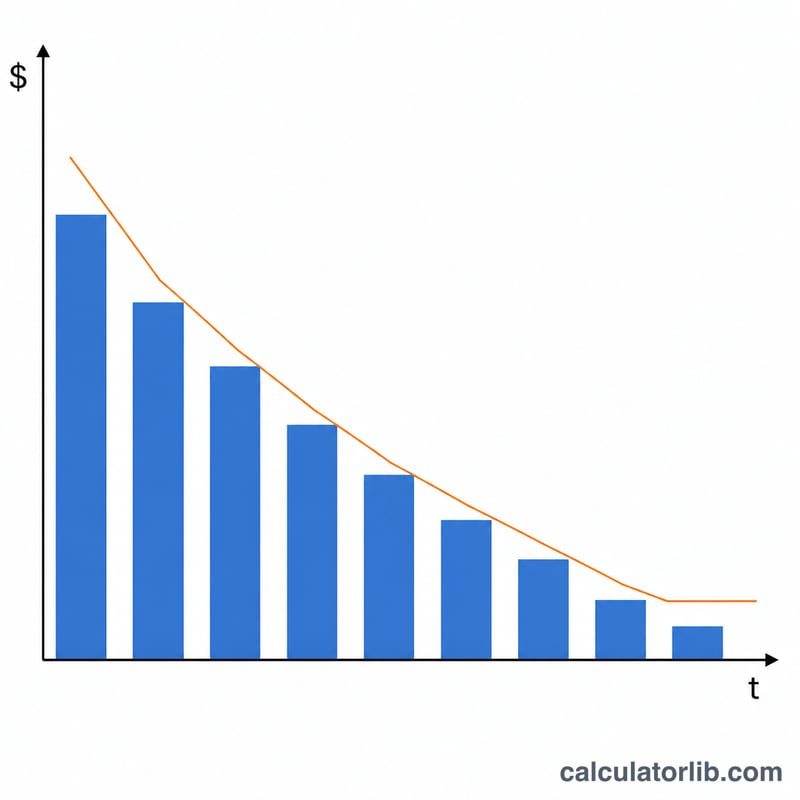

First the rate is calculated as factor ÷ useful life. Each year, depreciation equals the beginning book value times that rate. Because book value falls every year, the dollar amount of depreciation also falls. If applying the full rate would push book value below salvage, only the remaining amount above salvage is depreciated.

$$\text{Rate} = \frac{\text{Factor}}{\text{Useful Life}}$$

$$D_t = BV_{t-1} \times \text{Rate}$$

Worked Example

Suppose an asset costs $10,000 with a $1,000 salvage value, a 5-year life, and a factor of 2. The rate is \(2 \div 5 = 40\%\). Year 1 depreciation:

$$\$10{,}000 \times 40\% = \$4{,}000$$

leaving a book value of $6,000. Year 2:

$$\$6{,}000 \times 40\% = \$2{,}400$$

leaving $3,600. The accelerated expense in early years matches how many assets lose value fastest when new.

FAQ

What factor should I use? Use 2 for the 200% (double) declining balance method, or 1.5 for 150% declining balance. Higher factors front-load more depreciation.

Why won't it depreciate to zero? Depreciation stops at the salvage value — the estimated residual worth at the end of the asset's life.

Is this method allowed for taxes? Declining balance methods are widely used in accounting and tax (e.g. MACRS in the US), but specific rules and conventions vary by jurisdiction. Confirm with local guidance.