What is declining balance depreciation?

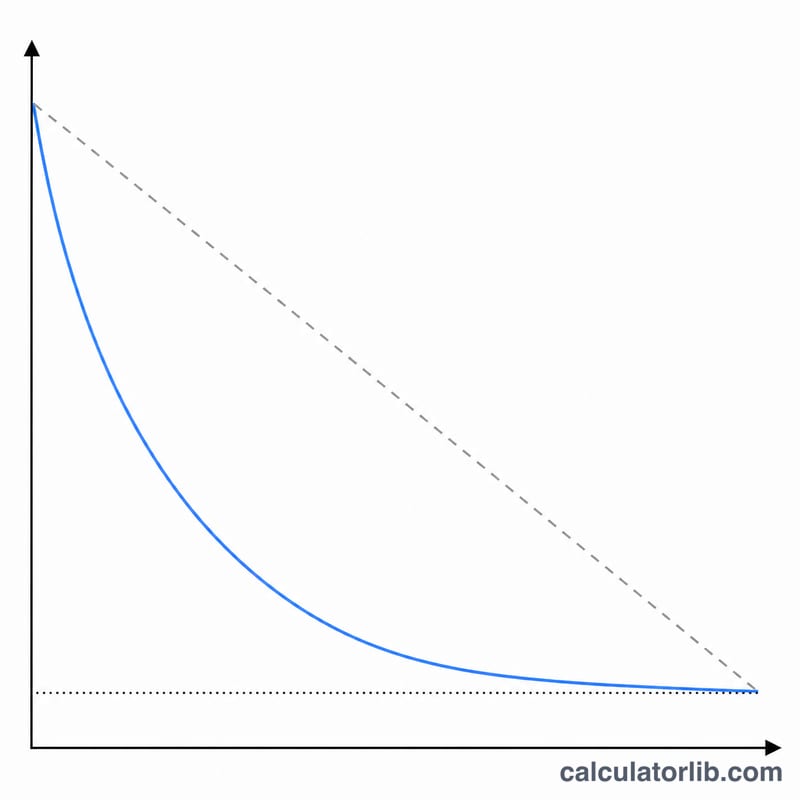

Declining balance depreciation is an accelerated method that writes off more of an asset's cost in its early years and less later on. Instead of spreading cost evenly like straight-line, it applies a fixed percentage rate to the asset's remaining book value each year. With a factor of 2 it becomes the popular Double Declining Balance (DDB) method; a factor of 1.5 gives 150% declining balance. This calculator is a universal accounting tool — the formula works the same in any country.

How to use the calculator

Enter the asset cost, salvage (residual) value, useful life in years, and a depreciation factor (2 = 200% DB / DDB, 1.5 = 150% DB, 1 = 100% DB). Pick the month and year the asset was placed in service, your fiscal year start, and a convention (Full-Month, Mid-Month, Mid-Quarter or Half-Year) that decides how much of the first partial year counts. Toggle "Round to Dollars" and choose whether to see just the expenses or the full schedule with running balances.

The formula explained

The annual rate is \(\text{rate} = \dfrac{\text{factor}}{\text{life}}\). Each year's expense is $$\text{Expense}_t = \frac{\text{factor}}{\text{life}} \times \text{BookValue}_{t-1}$$ where book value = cost minus accumulated depreciation. The salvage value is ignored when computing the rate but acts as a floor: an asset is never depreciated below its salvage value. In the final years the method finishes by depreciating the remaining balance down to salvage so total depreciation exactly equals cost minus salvage: $$\text{Expense}_t = \min\big(\text{rate}\times BV_{t-1},\; BV_{t-1}-\text{salvage}\big)$$

Worked example

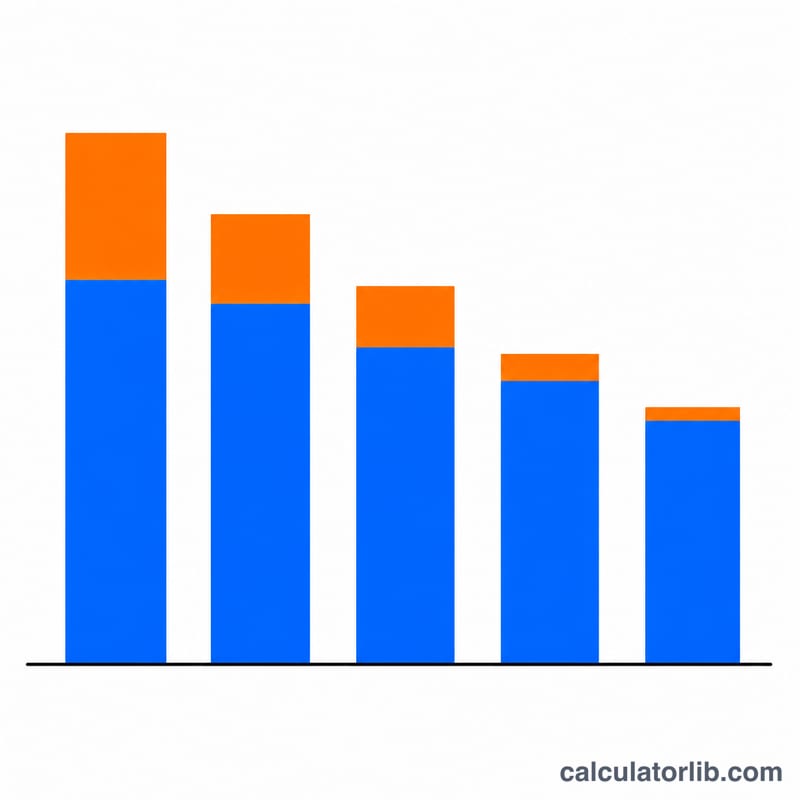

Cost $10,000, salvage $1,000, life 5 years, factor 2, Half-Year convention. Rate = \(2/5 = 40\%\). Year 1 (half year) = $$0.40 \times 10{,}000 \times 0.5 = \$2{,}000$$ Year 2 = $$0.40 \times 8{,}000 = \$3{,}200$$ Year 3 = $1,920, Year 4 = $1,152, Year 5 = $691.20, and a sixth partial year clears the remaining $36.80 to reach salvage. Total = $9,000 = cost − salvage.

FAQ

What is the difference between DDB and 150% declining balance? DDB uses factor 2 (200% of the straight-line rate); 150% DB uses factor 1.5. A higher factor accelerates write-off more steeply.

Why are there sometimes one more rows than the useful life? When the asset is placed in service after the start of the fiscal year, the first year is partial and the leftover fraction spills into an extra trailing year.

Does it match Excel's DDB function? The full-year amounts match Excel DDB(cost, salvage, life, period, factor); this tool adds convention-based proration and the finish-to-salvage adjustment.