What this calculator does

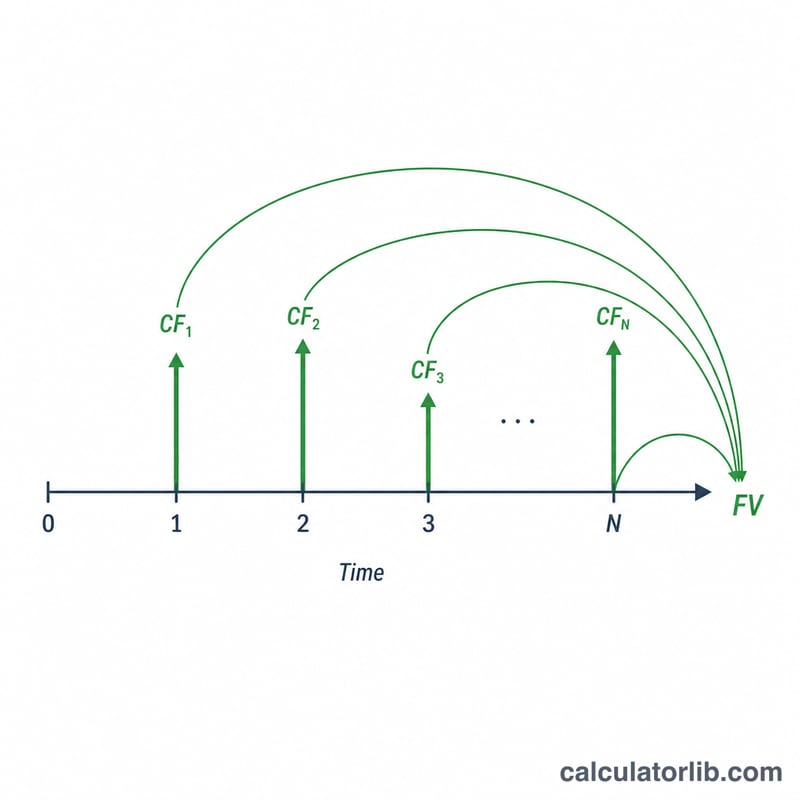

This tool computes the future value (FV) of a series of periodic cash flows — even (all the same) or uneven (different amounts at different times). You describe the stream as a set of lines, where each line says "this amount recurs for this many consecutive periods." The calculator expands those lines into individual cash flows, grows each one forward to the end of your time horizon at a compound interest rate, and sums them. It is the equivalent of combining Excel's NPV and FV functions.

How to use it

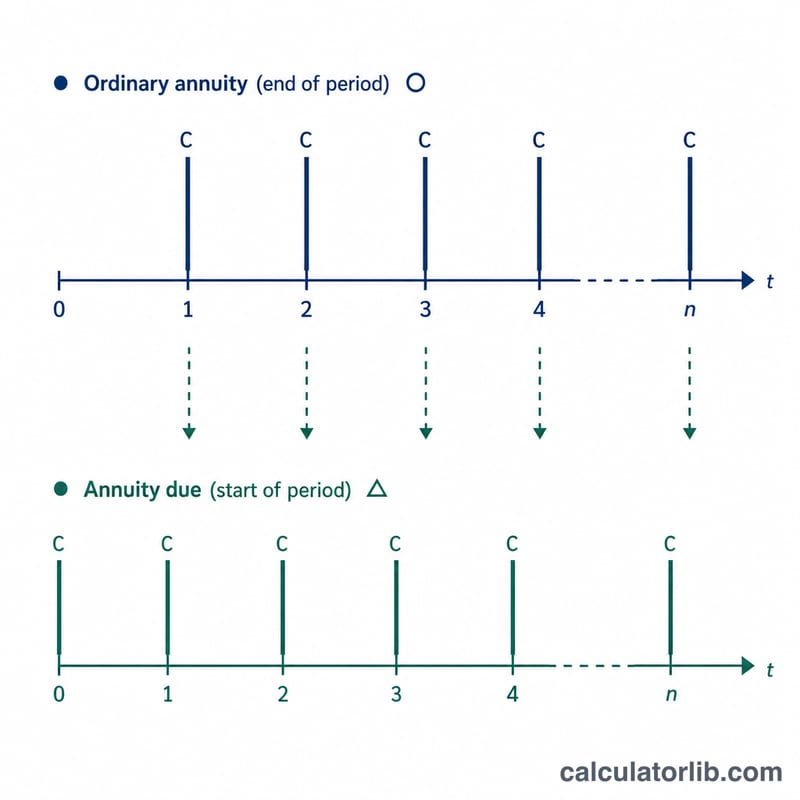

Enter the interest rate per period (a percentage), how many times interest compounds within each period, and whether cash flows occur at the end of each period (ordinary annuity) or the beginning (annuity-due). Then pick the number of lines and fill in, for each line, the number of periods and the recurring cash flow amount. The result shows a per-period detail table and the total future value.

The formula explained

The nominal rate is \(i = \text{rate} / 100\). With \(m\) compounds per period, the effective per-period growth factor is $$g = \left(1 + \tfrac{i}{m}\right)^{m}.$$ A cash flow at the end of period \(t\) earns interest for \((N - t)\) periods, so $$\text{FV}_t = \text{CF}_t \cdot g^{(N - t)}.$$ If cash flows occur at the beginning of each period, every exponent rises by one. The total is the sum of all \(\text{FV}_t\): $$\text{FV} = \sum_{t=1}^{N} \text{CF}_t \cdot \left(1 + \tfrac{i}{m}\right)^{m\,(N - t + d)}.$$

Worked example

Rate 4%, \(m = 1\) (so \(g = 1.04\)), end-of-period timing, and lines (2×200), (2×300), (2×500), (1×700). That is \(N = 7\) cash flows. Growing each to period 7: $$200\cdot1.04^{6} = 253.06,\ 200\cdot1.04^{5} = 243.33,\ 300\cdot1.04^{4} = 350.96,\ 300\cdot1.04^{3} = 337.46,\ 500\cdot1.04^{2} = 540.80,\ 500\cdot1.04 = 520.00,\ 700 = 700.00.$$ The total future value is 2,945.61.

FAQ

What if the rate is 0%? The growth factor becomes 1, so the future value equals the simple sum of all cash flows.

What's the difference between beginning and end timing? Beginning-of-period (annuity-due) cash flows each earn one extra period of interest, so the FV is larger by a factor of \(g\).

Can periods be months or quarters? Yes. "Period" is generic — just make sure the rate and compounding are expressed in that same unit.