What this calculator does

This tool estimates the future value of a one-time, lump-sum certificate of deposit (CD) at maturity using compound interest. A CD is a time deposit offered by banks and credit unions: you lock in a fixed amount for a set term at a stated interest rate, and the bank pays interest that compounds until the CD matures. Enter your deposit, term, rate, and compounding frequency to see the ending value, total interest earned, the annual percentage yield (APY), and a year-by-year growth schedule. An optional tax-rate field provides a simplified after-tax estimate.

How to use it

Enter the Initial Investment (the lump sum you deposit), the Term in months, and the nominal annual Interest Rate (APR). Choose how often interest compounds — monthly is the default and is common for CDs. Optionally enter a Tax Rate on Interest to estimate taxes owed. The calculator assumes a single deposit with no additional contributions and that interest is reinvested within the CD until maturity.

The formula explained

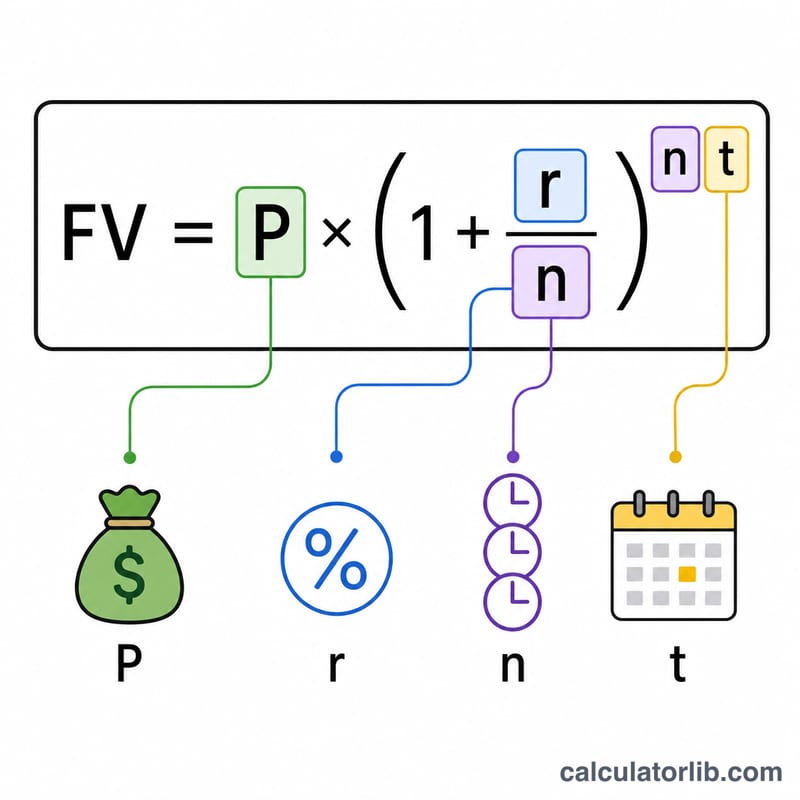

The maturity value is $$\text{FV} = P \left(1 + \frac{r}{n}\right)^{n t}$$ where \(P\) is the principal, \(r\) is the annual rate as a decimal, \(n\) is the number of compounding periods per year, and \(t\) is the term in years (months \(\div\) 12). Total interest is \(\text{FV} - P\). The effective annual yield is $$\text{APY} = \left(1 + \frac{r}{n}\right)^{n} - 1$$ which is higher than the nominal rate whenever interest compounds more than once a year.

Worked example

Deposit $20,000 for 60 months (5 years) at 5.5% compounded monthly. One year of growth multiplies by \(\left(1 + 0.055/12\right)^{12} \approx 1.056408\), so APY \(\approx 5.641\%\). After 5 years, \(\text{FV} \approx \$26{,}314.08\) and total interest \(\approx \$6{,}314.08\). With a 22% tax rate, taxes owed \(\approx \$1{,}389.10\) and the after-tax value \(\approx \$24{,}924.98\).

FAQ

Is the APY the same as the interest rate? No. The rate is the nominal annual rate; APY folds in compounding, so it reflects what you truly earn in a year.

Does this include recurring deposits? No — it models a single lump-sum CD with no extra contributions.

How accurate is the tax estimate? It is a simplified flat-rate estimate on total interest. In practice, CD interest is usually taxed annually as it is earned, and rules vary by country, so treat the after-tax figure as a rough guide.