What Is the Activity Method of Depreciation?

The activity method — also called the units-of-production method — spreads the cost of a fixed asset across how much it is actually used, rather than across time. Instead of charging the same expense every year, you charge depreciation based on output: miles driven, machine cycles run, hours operated, or widgets produced. This makes it ideal for assets whose wear and tear depends on usage, such as vehicles, manufacturing equipment, and aircraft.

How to Use This Calculator

Enter the Asset Cost (what you paid to acquire and ready the asset), the Salvage Value (its estimated worth at the end of its life), the Useful Units (Life) (total units it is expected to produce over its lifetime), and the Units Used in Period (activity during the period you are measuring). Pick the rounding precision and read off the depreciation per unit, the depreciation for the period, and the depreciable base.

The Formula Explained

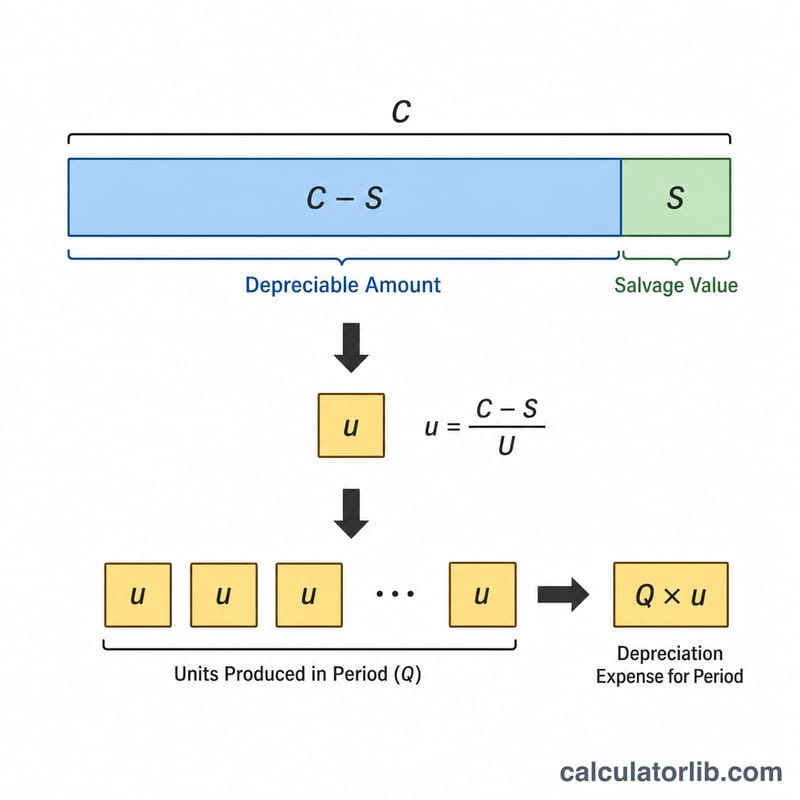

First find the depreciable base: Cost − Salvage Value. Divide it by the total useful units to get the depreciation per unit. Multiply that rate by the units used in the period to get the period's depreciation expense. Both unit fields must use the same unit of measure (miles with miles, cycles with cycles).

$$\text{Depreciation} = \frac{\text{Cost} - \text{Salvage}}{\text{Useful Units}} \times \text{Units Used}$$$$\text{Per Unit} = \frac{\text{Cost} - \text{Salvage}}{\text{Useful Units}}$$

$$\text{Period} = \text{Units Used} \times \text{Per Unit}$$

Worked Example

A delivery truck costs $50,000 with a $5,000 salvage value and a useful life of 90,000 miles. Depreciable base = \(50{,}000 - 5{,}000 = \$45{,}000\). Per unit = \(45{,}000 \div 90{,}000 = \$0.50\) per mile. If the truck is driven 15,000 miles this period, depreciation = \(15{,}000 \times 0.50 = \$7{,}500\).

$$\text{Depreciation} = \frac{50{,}000 - 5{,}000}{90{,}000} \times 15{,}000 = \$7{,}500$$

Key Terms Defined

The activity (units-of-production) method allocates an asset's cost based on actual usage rather than the passage of time. Understanding each input and output term makes the result easy to interpret.

- Asset cost — The total capitalized cost of acquiring the asset and preparing it for use. This includes the purchase price plus freight, installation, taxes and other costs necessary to bring the asset to working condition.

- Salvage (residual) value — The estimated amount expected to be recovered when the asset is disposed of at the end of its useful life, net of disposal costs. Depreciation is never charged below this value.

- Depreciable base — The portion of cost subject to depreciation, computed as cost minus salvage value: \(\text{Cost} - \text{Salvage}\). This total is spread across the asset's useful units.

- Useful units (units of life) — The total output the asset is expected to produce over its life, expressed in a relevant measure such as units produced, machine-hours, or miles driven.

- Units used in period — The actual activity recorded for the reporting period (e.g., units made or hours run), which drives that period's depreciation charge.

- Depreciation per unit — The cost allocated to each unit of activity: $$\text{Per Unit} = \frac{\text{Cost} - \text{Salvage}}{\text{Useful Units}}$$

- Book value (carrying value) — The asset's recorded value on the balance sheet, equal to cost minus accumulated depreciation.

- Accumulated depreciation — The running total of all depreciation expense recognized on the asset since it was placed in service, shown as a contra-asset account that reduces gross cost to book value.

FAQ

What if salvage value exceeds cost? The depreciable base becomes negative, which is invalid — salvage should never be greater than cost.

What happens if useful units is zero? Depreciation per unit is undefined, so the calculator returns zero and you must enter a positive number of useful units.

Does this track cumulative depreciation? No — this tool computes a single period. In a full schedule, ensure cumulative usage never drives book value below salvage value.