What is an equal-principal loan?

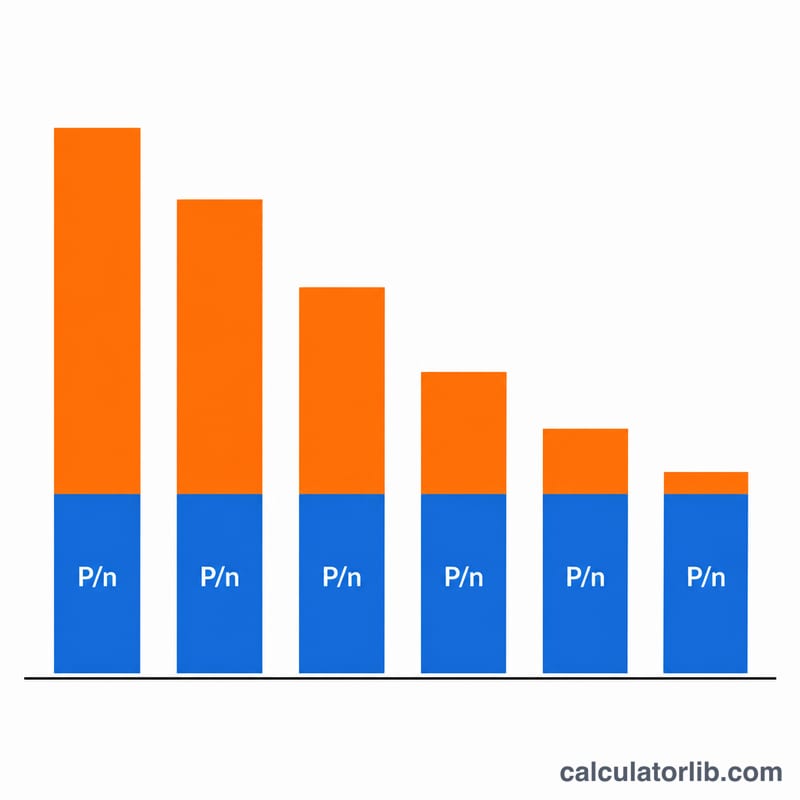

An equal-principal loan (also called a fixed-principal, constant-amortization, or declining-interest loan) repays the same amount of principal every period. Because interest is charged only on the remaining balance, and that balance steadily falls, the interest portion shrinks each period and the total payment declines over time. This is different from a standard amortized loan, where the total payment stays constant and the principal/interest split shifts gradually.

How to use this calculator

Enter the loan amount (principal), the nominal annual interest rate as a percent, the total number of payments over the term, and how often payments occur. The frequency converts the annual rate into a periodic rate by dividing by the number of periods per year. The tool returns the constant principal portion, the first (largest) and last (smallest) payment, the total interest paid, the total of all payments, and a full period-by-period schedule.

The formula explained

Let \(P\) be the loan amount, \(n\) the number of payments, \(r\) the annual rate as a fraction, and \(f\) the payments per year. The periodic rate is \(i = r / f\). Each period you repay principal of \(P / n\). The outstanding balance before payment \(k\) is \(P(n - k + 1) / n\), so the interest for that period is $$I_k = P\cdot\frac{n-k+1}{n}\cdot i,\quad i=\frac{r}{f}$$ and the total payment is $$\text{Total}_k = \frac{P}{n} + P\cdot\frac{n-k+1}{n}\cdot i.$$ The total interest over the whole loan simplifies neatly to $$I_{total} = i\cdot P\cdot\frac{n+1}{2}.$$

Worked example

Borrow $12,000 at 12% per year, 12 monthly payments. The monthly rate is $$0.12 / 12 = 0.01\ (1\%).$$ Principal per payment is $$12{,}000 / 12 = \$1{,}000.$$ Payment 1 charges interest of $$12{,}000 \times 0.01 = \$120,$$ so the total is $1,120. Each month interest drops by $10, so payment 12 is just $1,010. Total interest is $$0.01 \times 12{,}000 \times 13 / 2 = \$780,$$ and the total repaid is $12,780.

FAQ

How is this different from a normal mortgage payment? A standard mortgage uses equal total payments; here the principal is equal and the total payment falls each period, so you pay less total interest but higher payments early on.

What if the rate is 0%? Every payment is just the constant principal \(P/n\), total interest is zero, and the total repaid equals the loan amount.

Why does the last payment principal sometimes look adjusted? Any tiny rounding residual is absorbed into the final period so the ending balance closes to exactly zero.