What is the ACB Loan Amortization Schedule Calculator?

This calculator works out the fixed monthly payment (EMI) on a loan and shows how that payment is split between interest and principal over time. It uses the standard reducing-balance amortization method, where interest is charged on the remaining balance each month, so the interest portion shrinks and the principal portion grows as the loan is paid down. It applies to any currency and any standard fixed-rate installment loan such as a mortgage, car loan, or personal loan.

How to use it

Enter three values: the loan amount (principal), the annual interest rate as a percentage, and the loan term in years. The calculator converts the annual rate to a monthly rate and the term to a number of monthly payments, then returns your monthly EMI, the total you will repay, the total interest, and the principal/interest split for the very first payment.

The formula explained

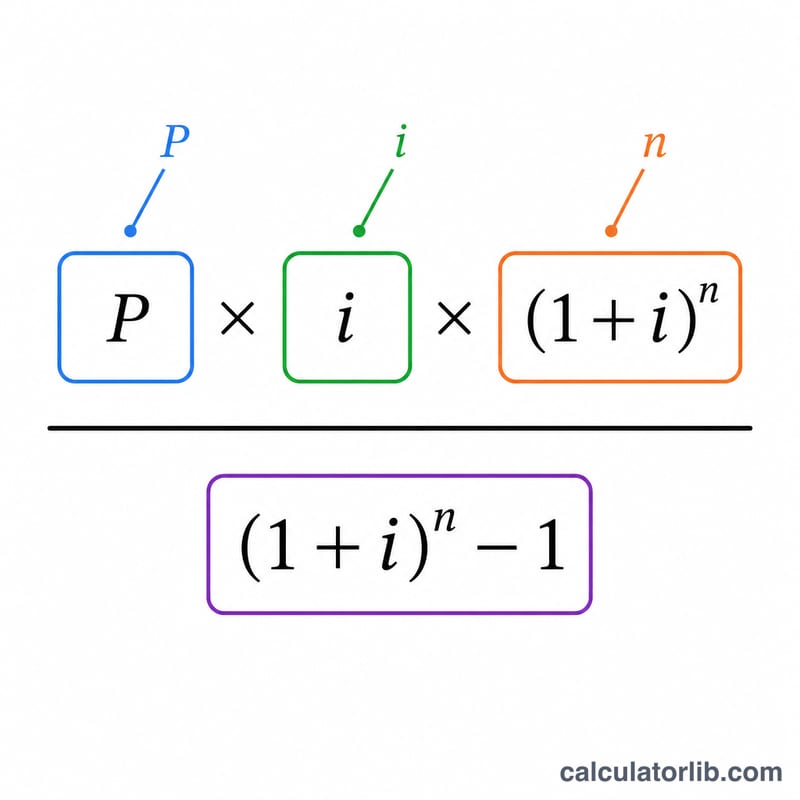

The core equation is $$\text{EMI} = \frac{P \cdot i \cdot (1+i)^n}{(1+i)^n - 1}$$ where \(P\) is the principal, \(i\) is the monthly interest rate (annual rate \(\div\) 12 \(\div\) 100), and \(n\) is the number of months. Each month the interest charged equals \(\text{Balance} \times i\), and the principal repaid is \(\text{EMI} - \text{Interest}\). If the rate is 0%, the EMI is simply \(P \div n\).

Worked example

For a $200,000 loan at 5% annual interest over 30 years: \(i = 0.05/12 \approx 0.0041667\) and \(n = 360\). The EMI works out to about $1,073.64 per month. The total repaid is roughly $386,511, meaning about $186,511 is interest. The first month's interest is $$200{,}000 \times 0.0041667 \approx \$833.33,$$ leaving about $240.31 toward the principal.

EMI Across Different Loan Scenarios

The table below shows the monthly EMI, total amount repaid over the life of the loan, and total interest paid, using the standard reducing-balance formula \( \text{EMI} = P \cdot \dfrac{i(1+i)^n}{(1+i)^n - 1} \). All figures assume no extra payments and a fixed rate for the entire term.

| Loan Amount | Rate | Term | Monthly EMI | Total Repaid | Total Interest |

|---|---|---|---|---|---|

| $100,000 | 4% | 15 yrs | $739.69 | $133,144 | $33,144 |

| $100,000 | 5% | 30 yrs | $536.82 | $193,256 | $93,256 |

| $200,000 | 5% | 20 yrs | $1,319.91 | $316,779 | $116,779 |

| $200,000 | 7% | 30 yrs | $1,330.60 | $479,017 | $279,017 |

| $300,000 | 4% | 30 yrs | $1,432.25 | $515,609 | $215,609 |

| $300,000 | 5% | 15 yrs | $2,372.38 | $427,029 | $127,029 |

| $300,000 | 7% | 30 yrs | $1,995.91 | $718,526 | $418,526 |

Two patterns stand out: a higher rate dramatically increases total interest (note the $200,000 loan at 7% over 30 years repays more than double the principal), and a shorter term sharply raises the monthly payment but cuts total interest. You can verify any of these figures or test your own numbers with the calculator above.

Key Loan Terms Explained

- EMI (Equated Monthly Installment) — the fixed amount you pay each month, combining both interest and principal, so that the loan is fully repaid by the end of the term.

- Principal (P) — the original loan amount borrowed, before any interest is added. It is the starting balance that the amortization works to reduce to zero.

- Monthly interest rate (i) — the annual nominal rate converted to a monthly decimal. In this formula \( i = \dfrac{\text{Rate(\%)}}{1200} \); for example, a 6% annual rate gives \( i = 0.005 \) per month.

- Number of payments (n) — the total count of monthly installments, equal to the term in years multiplied by 12. A 30-year loan has \( n = 360 \) payments.

- Amortization — the process of paying off a debt over time through scheduled installments, where each payment chips away at both interest and principal according to a set schedule.

- Reducing-balance method — the standard approach in which interest is charged each period only on the remaining outstanding balance, not the original principal. As the balance falls, the interest portion of each EMI shrinks.

- Total interest — the sum of all interest paid over the life of the loan, equal to total repaid minus the original principal (\( \text{EMI} \times n - P \)).

- Escrow — a separate account some lenders use to collect and hold funds for property taxes and insurance, paid alongside the loan EMI. Escrow amounts are not part of the principal-and-interest EMI computed here.

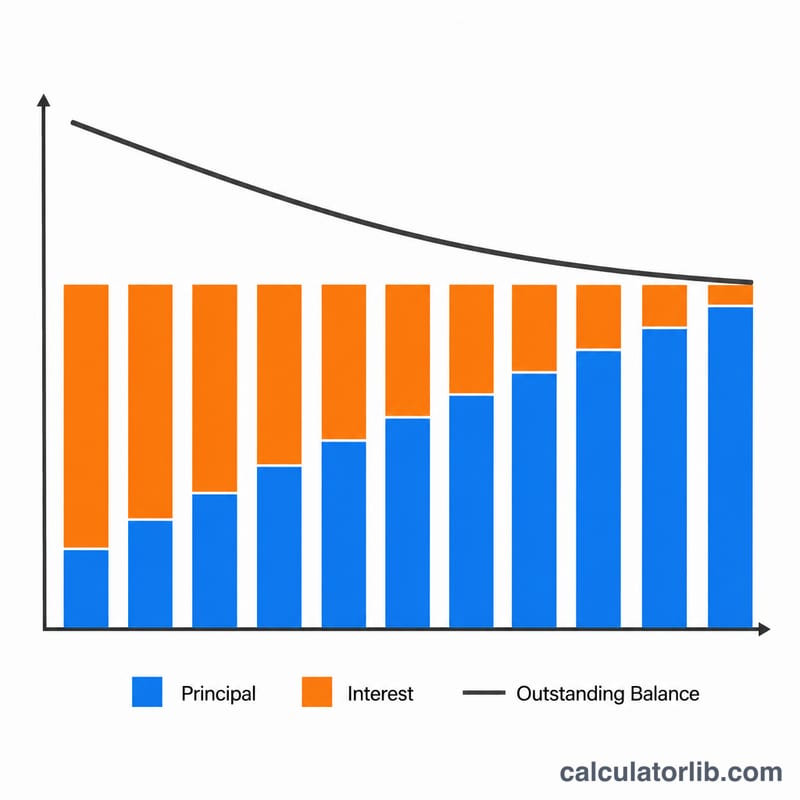

Understanding Your Amortization Results

The EMI is your fixed monthly obligation for principal and interest. It stays constant for the entire term (assuming a fixed rate), which makes budgeting predictable even though the internal split between interest and principal changes every month.

Total repaid is the EMI multiplied by the number of payments, and total interest is that figure minus your original principal. On long-term, higher-rate loans the total interest can rival or exceed the amount you borrowed — a useful reality check before committing.

The first-payment split is revealing. In the earliest payments, interest is charged on the full outstanding balance, so most of your EMI goes to interest and only a small slice reduces principal. For a $200,000 loan at 7% over 30 years, the first payment's interest is roughly \( 200{,}000 \times 0.07/12 \approx \$1{,}167 \) out of the $1,331 EMI, leaving only about $164 toward principal.

As the balance falls, the interest-to-principal ratio steadily flips: later payments apply far more to principal and far less to interest. This is the defining behavior of the reducing-balance method and explains why paying extra early in the term saves disproportionately more interest than paying extra late.

Finally, distinguish these principal-and-interest figures from the full cost of ownership. The EMI here does not include property taxes, homeowners or mortgage insurance, HOA dues, escrow, or closing fees. Your actual monthly outlay and lifetime cost will be higher once those items are added, so treat this result as the financing core rather than the complete bill.

FAQ

Why does so much of my early payment go to interest? Interest is charged on the outstanding balance, which is highest at the start, so early payments are interest-heavy and later payments are principal-heavy.

Does this include taxes, insurance, or fees? No. It calculates pure principal-and-interest repayment. Escrow items like property tax or insurance are not included.

Can I use it for any currency? Yes. The math is currency-neutral, so enter amounts in whatever currency your loan uses.